Quick Summary

Selling to a competitor requires precision, preparation, and strategic control.

1. Get Audit-Ready First.

Prepare 3–5 years of clean financials (P&L, balance sheets, cash flow, tax returns) and document operations (SOPs, contracts, org charts). Competitors know your industry; disorganization weakens your leverage.

2. Secure an Independent Valuation.

A professional valuation protects you from lowball offers, establishes a defensible asking price, and anchors negotiations with data instead of emotion. Most mid-market deals rely on EBITDA multiples, though asset-based, revenue, or DCF methods may apply depending on your business.

3. Lock Down Confidentiality Before Any Talks.

Use a strong, attorney-drafted NDA with non-solicitation and enforcement clauses. Release information in stages, never share customer lists, proprietary systems, or sensitive operational details until late-stage due diligence.

4. Approach the Right Competitors Strategically.

Shortlist 3–5 buyers based on strategic fit, financial capacity, and motivation. Open conversations as “strategic discussions,” not a direct sale pitch, to maintain leverage.

5. Create Competitive Tension.

Engaging multiple qualified buyers increases speed, pricing, and negotiation strength. Buyers act more aggressively when they know others are evaluating the opportunity.

Bottom Line:

Preparation, valuation, confidentiality controls, disciplined outreach, and buyer competition determine whether you sell from a position of strength or give your competitor leverage.

In part 1 of this series, we covered why competitors make ideal buyers, the real risks to know before starting, types of buyers, and more. In part 2, we will discuss the step-by-step process of selling your business to a competitor. From getting your financials and operations to negotiating deal terms, we will deliver the actionable steps to make sure you exit your business profitably.

Step 1: Get Your Financials and Operations in Order

Before a single conversation happens with any potential buyer, your house needs to be in order. A competitor buyer will scrutinize your financials with a level of industry-specific knowledge that outside buyers simply don’t have. Any inconsistency, gap, or disorganization in your records will be noticed, and used against you in negotiations.

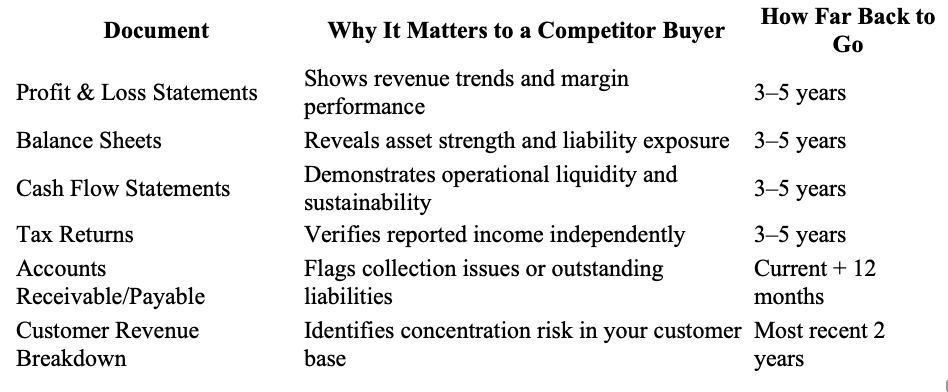

Financial Records to Prepare Before Any Conversation

The financial documents you prepare before any buyer conversation aren’t just administrative; they’re the foundation of your asking price. Gaps or inconsistencies here don’t just raise questions; they hand negotiating power directly to the buyer.

Having these documents audit-ready before any conversation begins signals professionalism and removes the friction that causes deals to slow down or fall apart during due diligence.

Operational Documentation That Increases Business Value

Financial records tell a buyer what your business earns. Operational documentation tells them what it’s worth beyond the numbers. Systems, processes, and documented workflows show a buyer that the business runs independently of you, which dramatically increases its value and reduces their perceived risk.

Key operational documents to prepare include standard operating procedures (SOPs) for your core functions, organizational charts, key supplier contracts, employee agreements, and any proprietary systems or technology your business relies on. The more systematized and documented your operations appear, the stronger your negotiating position becomes.

Step 2: Get a Professional Business Valuation

Walking into a negotiation with a competitor without an independent valuation is one of the costliest mistakes a seller can make. Your instinct about what your business is worth and what a sophisticated competitor buyer believes it’s worth can be very different numbers, and without third-party data, you have no anchor to hold the conversation.

Why an Independent Valuation Protects You From Lowball Offers?

It establishes a credible, defensible asking price backed by industry-standard methodology.

It removes emotion from the pricing conversation; the number comes from data, not gut feeling.

It signals to the buyer that you are a prepared, serious seller who has done the work.

It gives your attorney and broker a foundation to work from during negotiations.

It protects you from anchoring to a number the buyer proposes early in the conversation.

An independent valuation doesn’t just protect your price; it reframes the entire negotiation. Instead of responding to a buyer’s offer, you’re presenting a position that requires them to respond to you.

Competitor buyers are experienced. They know market multiples, they understand operational benchmarks, and they have internal teams that assess acquisitions regularly. Walking in without your own valuation means you’re bringing a gut feeling to a data-driven conversation.

The cost of a professional valuation, typically ranging from a few thousand dollars to tens of thousands, depending on business size and complexity, is almost always recovered many times over in the final sale price. It’s not an expense; it’s an investment in negotiating power.

Key Valuation Methods Used When Selling to a Competitor

There are several approaches valuators use, and understanding which one applies to your business helps you anticipate how a competitor buyer will approach pricing.

The EBITDA Multiple Method is the most common for small to mid-sized businesses. It takes your earnings before interest, taxes, depreciation, and amortization and multiplies it by an industry-specific figure, typically between 2x and 8x, depending on your sector, growth trajectory, and market conditions.

The Asset-Based Valuation adds up the fair market value of everything your business owns, equipment, inventory, intellectual property, real estate, and subtracts liabilities. This method is more relevant for asset-heavy businesses like manufacturing or logistics companies.

- EBITDA Multiple: Best for profitable, recurring-revenue businesses with strong operational systems.

- Asset-Based: Best for businesses where physical or intellectual assets drive the majority of value.

- Revenue Multiple: Often used for high-growth businesses where current profit doesn’t yet reflect future potential.

- Discounted Cash Flow (DCF): Projects future earnings and discounts them to present value, most common in larger, more complex transactions.

Finding a Quality Business Broker for Your Business Size

Earned Exits was ranked as a top business broker in 2025 and has performed over $2 billion in transactions over multiple industries. The company’s 10-point process helps companies with $1 to 40 million in revenue find a qualified buyer and make the selling process as easy and streamlined as possible.

The firm’s valuation experts have developed specific methodologies for quantifying these benefits during pre-sale assessments. By documenting employee tenure, specialized expertise, and customer relationships, they build compelling value narratives that justify premium pricing. Rather than hoping buyers will recognize these strengths, their approach provides concrete evidence of the operational stability that justifies higher valuations.

Earned Exits specializes in businesses with annual revenues of $1 to $40 million across 17+ industries. This focus allows their team to maintain deep expertise in the valuation nuances, buyer landscapes, and transaction structures most relevant to mid-market companies. Their industry coverage includes manufacturing, business services, healthcare, technology, distribution, construction, and professional services, among others.

Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Step 3: Protect Confidential Information Before Talks Begin

Before you say a single word to a potential competitor buyer, your confidentiality strategy needs to be fully locked in. This isn’t a step you can revisit after the first conversation. Once information is shared, you cannot un-share it. The preparation you do here directly determines how much control you retain throughout the entire sale process.

How to Use a Non-Disclosure Agreement Effectively

An NDA is not a formality; it’s your first line of legal defense. But a poorly written NDA is nearly as dangerous as having none at all. Generic templates downloaded from the internet often contain loopholes that experienced acquisition teams exploit without technically violating the agreement. Your NDA needs to be drafted or reviewed by a legal professional who understands M&A transactions specifically.

The NDA should define exactly what constitutes confidential information, specify how long the confidentiality obligation lasts after the deal falls through, and explicitly prohibit the buyer from using your information to solicit your customers or employees. It should also include a clear remedies clause that outlines what happens if the agreement is breached; vague consequences are rarely enforced effectively.

NDA Must-Have Checklist:

✓ Clear definition of what qualifies as confidential information

✓ Explicit prohibition on poaching customers and employees

✓ Defined time period for confidentiality obligations (typically 2–5 years)

✓ Remedies clause with enforceable consequences for breach

✓ Non-solicitation clause covering staff and clients

✓ Mutual confidentiality (protects both parties)

✓ Jurisdiction clause specifying which state’s laws govern the agreement

Have your attorney present the NDA, not you personally. When legal counsel delivers the document, it communicates immediately that you are a sophisticated seller who takes this process seriously. Buyers who aren’t genuinely interested tend to back away at this stage, which is actually useful information.

Never begin sharing any business information,, not even high-level revenue figures, before the NDA is signed, dated, and in your possession. The conversation can be warm and exploratory, but the documents come first.

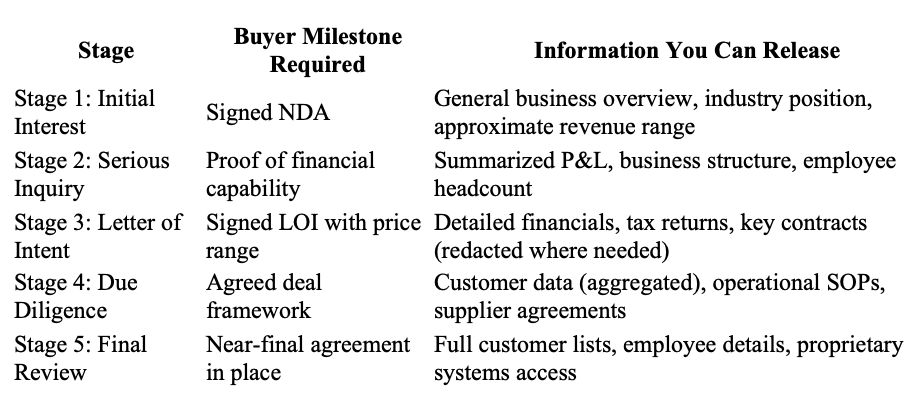

What Information to Share and When

Think of your confidential information as a staircase, not an open door. Each step up reveals more detail, and the buyer earns each step by demonstrating genuine commitment. Early conversations should involve only high-level, publicly available information: your general business category, approximate size, and the broad reason you’re exploring a sale. Nothing that gives a competitor operational advantage belongs in those first discussions.

How to Stage Information Release During Due Diligence

This staged approach does two important things simultaneously. First, it protects your most sensitive information until the buyer has made a real financial and legal commitment to the transaction. Second, it maintains your negotiating power with a buyer who hasn’t seen everything, yet has less ammunition to argue for a lower price.

Your customer list deserves special attention in this framework. It is often the single most valuable asset in your business, and it is also the piece of information a competitor can most immediately exploit if the deal collapses. Under no circumstances should a full, named customer list be shared before the final stages of a near-closed deal.

The same principle applies to proprietary processes, technology, and supplier pricing. These details go last after the buyer has demonstrated through signed agreements and financial commitment that they are a serious, accountable party in the transaction.

Working with a business broker adds a significant layer of protection here. Brokers manage the information release process on your behalf, using established data room platforms and document controls that track exactly what the buyer has accessed and when. That audit trail becomes critical if a dispute ever arises after a deal falls through.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Step 4: Approach the Right Competitor the Right Way

Who you approach first and how you approach them shapes everything that follows. A misstep here doesn’t just cost you one buyer; it can send signals across your industry that your business is for sale before you’re ready for that to be public knowledge.

This step requires patience and strategy in equal measure. The goal isn’t to start as many conversations as possible, it’s to start the right conversations with the right buyers in a way that keeps you in control of the narrative and the timeline.

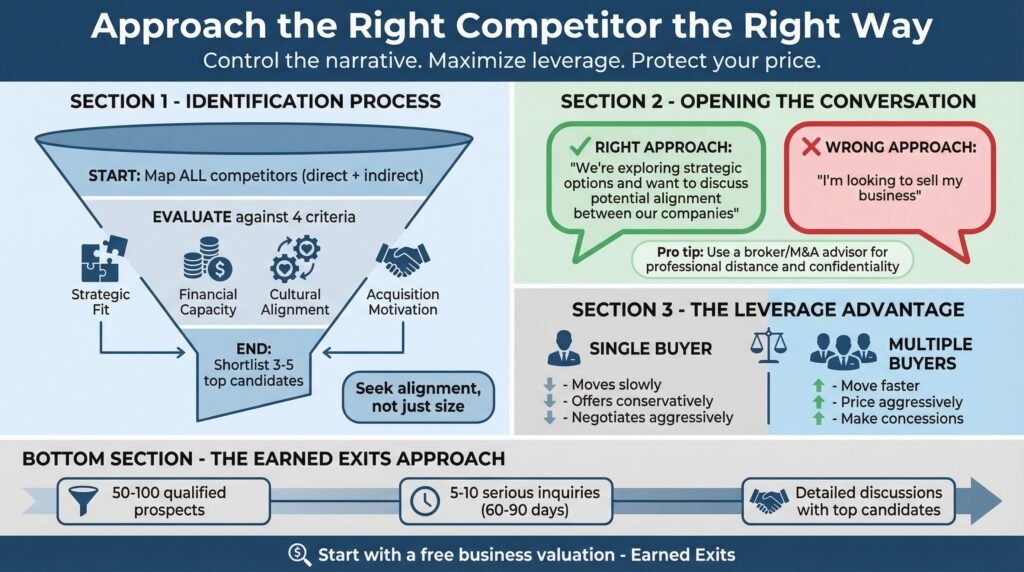

How to Identify and Shortlist Potential Competitor Buyers

Start with a structured analysis rather than a gut feeling. Map out every competitor in your market, direct and indirect, and evaluate each one against four criteria: strategic fit, financial capacity to complete an acquisition, cultural alignment with your team and customers, and their likely motivation for acquiring your business specifically.

From that full list, shortlist three to five candidates who score highest across all four criteria. You’re not looking for the biggest company, you’re looking for the buyer whose strategic goals align most closely with what you’re selling. That alignment is what drives premium pricing and smoother negotiations.

How to Open the Conversation Without Tipping Your Hand

The initial approach is a delicate communication challenge. You want to generate genuine interest without broadcasting that your business is actively for sale. The most effective approach is an indirect, exploratory framing, something along the lines of exploring strategic partnership opportunities or discussing potential collaboration. This opens the door without immediately positioning you as a motivated seller, which is a posture that costs you price and leverage.

Opening Conversation Framework:

What to say: “We’ve been exploring some strategic options for the business and wanted to have a confidential conversation about whether there might be alignment between our two companies.”

What not to say: “I’m looking to sell my business and thought you might be interested.”

Why it matters: The moment a competitor knows you are actively motivated to sell, their opening offer drops and their negotiation posture stiffens. Keep the power balanced by keeping your motivation ambiguous early.

Ideally, this initial outreach is handled by a business broker or M&A advisor rather than you directly. When a third party approaches, it immediately signals that the process is structured and professional, and it keeps your identity and motivations protected until the buyer has demonstrated genuine, documented interest.

If you’re approaching yourself, keep the first conversation short, high-level, and genuinely exploratory. Ask as many questions as you answer. Learn their strategic priorities before you reveal anything about yours. The more you understand about what they want, the more precisely you can position what you’re offering.

Why Working Multiple Buyers Creates Leverage

In the active marketing phase, experienced brokers, like Earned Exits, executes confidential outreach to qualified buyers aligned with your Buyer Profile, typically approaching 50-100 carefully selected prospects rather than broadcasting your availability broadly.

A buyer who knows they have no competition has every reason to move slowly, offer conservatively, and negotiate aggressively on terms. A buyer who believes other parties are actively evaluating the same opportunity behaves very differently; they move faster, price more aggressively, and make concessions they’d otherwise never offer.

You don’t need to fabricate competition; you need to create it by approaching multiple qualified buyers simultaneously. Even if you ultimately prefer one buyer over the others, the existence of competing interests is your single most powerful negotiation tool. Earned Exits manages this process specifically to maintain competitive tension throughout the transaction without any party knowing exactly where they stand relative to the others.

Their approach emphasizes quality over quantity, focusing on buyers with demonstrated commitment to employee retention and business continuity. This targeted marketing typically generates 5-10 serious inquiries within 60-90 days, leading to detailed discussions with the most promising candidates.

Ready to get the process started today? Click the link below to start Earned Exits’ free valuation process by filling out their short form.

Learn more of establishing favorable and profitable deal terms, navigate due diligence, close the sale, and more here.

Frequently Asked Questions

Selling a business to a competitor raises questions that most owners have never had to think through before. The process is unfamiliar, the stakes are high, and the decisions made along the way have lasting financial and professional consequences.

The questions below cover the most common concerns sellers raise, from timelines and valuations to confidentiality, employee protection, and deal structure. Each answer is designed to give you a practical, honest picture of what to expect so you can move forward with clarity.

If a question here leads to a more specific concern about your own situation, that’s a signal to bring in professional guidance. The details of your business, your industry, and your goals matter, and generic answers only go so far when the stakes are this high.

Quick Reference: Key Terms in a Competitor Sale

NDA (Non-Disclosure Agreement): A legally binding contract preventing the buyer from sharing or misusing your confidential information.

LOI (Letter of Intent): A non-binding document outlining the proposed purchase price and key deal terms before final negotiations.

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization the most common basis for business valuation multiples.

Earn-Out: A deal structure where a portion of the purchase price is paid after closing, tied to future business performance.

Due Diligence: The buyer’s formal investigation of your business’s financials, operations, legal standing, and contracts before closing.

Non-Compete Clause: A contractual restriction preventing you from starting or joining a competing business for a defined period after the sale.

Data Room: A secure digital environment where confidential business documents are shared with verified buyers during due diligence.

How do I know if my business is ready to sell?

A business is ready to sell when it can demonstrate consistent financial performance, documented operational systems, a customer base that isn’t dependent on the owner’s personal relationships, and a management structure that functions without the owner’s daily involvement. If your business struggles on any of these dimensions, it’s worth investing six to eighteen months improving those areas before approaching buyers. The improvement in valuation will far exceed the time invested. A business broker or M&A advisor can provide an honest readiness assessment and a specific action plan for closing any gaps before the sale process begins.

What financial documents does a competitor buyer typically request?

Expect requests for three to five years of profit and loss statements, balance sheets, cash flow statements, and business tax returns. Beyond the core financials, buyers typically request accounts receivable and payable aging reports, a customer revenue breakdown showing concentration and trends, payroll records, all existing contracts and leases, and documentation of any outstanding liabilities or legal matters. Having these documents organized, current, and audit-ready before the process begins dramatically accelerates due diligence and signals to the buyer that you are a prepared, professional seller, which itself contributes to buyer confidence and deal momentum.

Can I sell part of my business to a competitor instead of the whole thing?

Yes, partial sales to competitors are structurally possible and occasionally make strategic sense. A partial sale might involve selling a specific product line, a geographic territory, a division, or a percentage of equity rather than the entire business. This approach can generate capital while allowing you to retain involvement in the parts of the business you want to continue building.

However, partial sales with competitor buyers carry unique risks. A competitor who acquires a minority stake or a specific division gains inside access to your operations, financials, and strategic direction, which can create significant disadvantages if the relationship deteriorates or if they later pursue a full acquisition from a position of informational advantage. Partial sales to competitors require exceptionally careful legal structuring and clear governance agreements that define the boundaries of each party’s access and authority. Never enter a partial sale arrangement with a competitor without M&A legal counsel reviewing every aspect of the structure.

What is the difference between selling to a direct and indirect competitor?

A direct competitor operates in the same market, serves the same customers, and sells the same or nearly identical products or services. Selling to a direct competitor typically produces the highest strategic premium. They understand exactly what they’re buying and why it accelerates their position, a but also carries the greatest confidentiality risk, since any information you share can be immediately deployed against your business if the deal falls through. An indirect competitor operates in an adjacent space with similar customers but different products, or the same products in a different region. They present lower confidentiality risk and often a smoother post-sale cultural transition, though the strategic premium may be somewhat lower than a direct competitor would offer.

How do I protect my customer list during the sale process?

Your customer list is often the single most valuable and most vulnerable asset in your business during a competitor sale. Protecting it requires a deliberate, multi-layered strategy that starts well before any buyer conversation begins. At the NDA stage, include an explicit non-solicitation clause that prohibits the buyer from directly or indirectly approaching your customers if the deal falls through. This clause should name customer data specifically as a protected category of confidential information.

During the information release process, never share individual customer names, contact details, or account-level revenue data until the very final stages of a near-closed transaction. Before that point, aggregate data is sufficient: total customer count, revenue concentration percentages, and customer tenure statistics give a serious buyer everything they need to validate your valuation without gaining actionable intelligence about specific accounts.

If your broker uses a secure data room for document sharing, ensure that customer-specific files have restricted access settings that require a separate, explicit authorization before the buyer can view them. This creates an additional checkpoint in the process and a clear audit trail showing exactly when and under what conditions that information was accessed. The customer list goes last after the LOI is signed, due diligence is substantially complete, and closing is imminent. Treat it as the final key you hand over at the closing table, not a document you share to demonstrate good faith early in the process.

Earned Exits specializes in helping business owners navigate complex sales, including competitor transactions, with the confidentiality protections, market expertise, and negotiating discipline that consistently produce stronger outcomes than going it alone. The company specializes in creating meaningful business transitions that protect what matters most. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.