Quick Summary

When selling your business to a competitor, price alone doesn’t determine your outcome; deal structure, legal protections, and negotiation discipline matter just as much. Every term is negotiable, including payment structure, earn-outs, non-competes, indemnification clauses, transition involvement, and employee protections.

Due diligence is where buyers often attempt to renegotiate, so preparation, organized documentation, and maintaining strong operational performance are critical to preserving value. Closing requires vigilance against last-minute concessions and clear communication with employees and customers to protect continuity.

Because competitor sales carry heightened confidentiality and leverage risks, working with an experienced business broker significantly improves pricing, protects sensitive information, creates competitive tension among buyers, and ensures the process stays structured, strategic, and financially optimized from negotiation through final transition.

In part 2 of this series, we discussed the first steps of selling a business to a competitor, such as getting your financials and operations, and negotiating deal terms. In part 3 of this series, we will discuss how to discuss favorable and profitable deal terms, navigate due diligence, close the sale, and more.

Step 5: Negotiate the Deal Terms That Protect Your Interests

Price is the headline, but terms are where sellers get hurt. A high purchase price paired with an unfavorable deal structure can leave you worse off financially than a slightly lower price with clean, seller-friendly terms. Before any negotiation begins, get clear on your priorities across every dimension of the deal, not just the number at the top.

- Total purchase price and payment structure: how much, and how it’s paid over time.

- Earn-out conditions: performance targets tied to future payments and how achievable they realistically are.

- Non-compete scope and duration: what industries, geographies, and time periods you’ll be restricted from.

- Representations and warranties: what you’re legally guaranteeing about the state of your business.

- Indemnification clauses: your liability exposure if something surfaces post-sale that wasn’t disclosed.

- Transition involvement: how long you’re expected to stay on, in what capacity, and at what compensation.

- Employee and key personnel terms: protections for your team as part of the deal structure.

Every one of these elements is negotiable. The mistake most first-time sellers make is treating the buyer’s initial term sheet as a near-final document rather than an opening position. It is an opening position, treat it as one.

Your attorney and broker should review every term before you respond to any offer. What looks like standard boilerplate in an acquisition agreement often contains provisions that significantly impact your financial outcome and post-sale freedom. Never negotiate these details alone.

Price Structure Options: Lump Sum vs. Earn-Out Agreements

Every competitor buyer will require a non-compete clause, which is standard and expected. What isn’t standard is the scope they’ll initially propose. Buyers routinely push for the broadest possible non-compete: maximum geographic coverage, the widest possible industry definition, and the longest legally enforceable duration. Each of these dimensions directly limits what you can do professionally after the sale, and each one is negotiable.

- Geographic scope: Push to limit this to the specific markets where you directly competed, not entire countries or industries.

- Duration: Two to three years is standard for most small business sales. Anything beyond five years is worth pushing back on firmly.

- Industry definition: Be precise about exactly which business activities are restricted. Vague language here limits far more than the buyer actually needs.

- Compensation: In some jurisdictions and deal structures, you can negotiate separate compensation for agreeing to the non-compete and treat it as a separate asset.

Non-compete clauses are one of the most legally consequential parts of any sale agreement. A clause that’s too broad can prevent you from working in your own industry for years after the sale, even in roles that have no meaningful impact on the buyer’s business.

Have your attorney review the non-compete language in complete isolation from the rest of the deal. It deserves focused, independent attention rather than being evaluated as just one clause among many in a lengthy agreement.

Employee Retention Terms You Should Push For

Your team built this business alongside you, and many of them have no idea a sale is happening. Negotiating explicit employee retention terms into the deal agreement is both a moral obligation and a practical one. A business that loses key staff during or immediately after a transition loses significant value. Push for guaranteed employment periods for critical team members, retention bonuses funded by the buyer, and written commitments about role and compensation changes post-acquisition. The buyer wants the business to succeed after the sale, use that shared interest as leverage to protect your people.

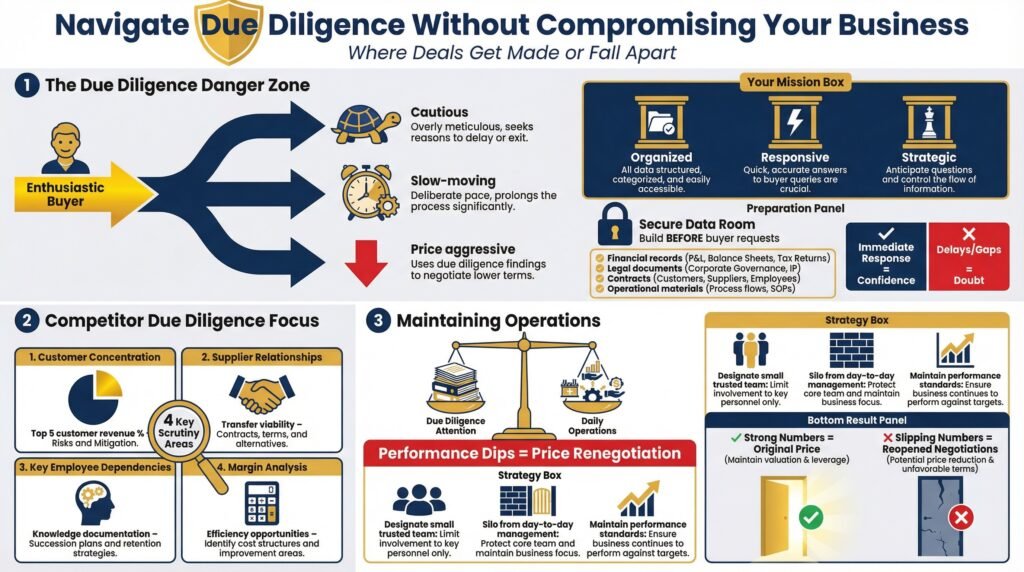

Step 6: Navigate Due Diligence Without Compromising Your Business

Due diligence is the phase where deals get made or fall apart. A buyer who was enthusiastic during negotiations can become cautious, slow-moving, or suddenly aggressive on price when they get into the details of your business. Your job during this phase is to be organized, responsive, and strategic, giving them what they need to close the deal while protecting information that isn’t yet appropriate to share.

The best way to manage due diligence effectively is to prepare for it before it starts. Build a secure data room, a digital repository containing all your financial records, legal documents, contracts, and operational materials, before the buyer formally requests anything. When you can respond to due diligence requests immediately and completely, it signals competence and builds buyer confidence. Delays and gaps do the opposite.

What Business Competitors Look for During Due Diligence

A competitor buyer’s due diligence is sharper and more industry-specific than a generic buyer’s review. They’re not just checking the numbers; they’re validating assumptions they already have about your business based on their own market knowledge. This means they’ll quickly spot discrepancies that an outside buyer might miss entirely.

They’ll focus heavily on customer concentration risk, specifically, what percentage of your revenue comes from your top five customers. They’ll examine supplier relationships to assess how transferable those agreements are post-acquisition. They’ll evaluate your key employee dependencies to understand how much operational knowledge lives in specific people rather than documented systems. And they’ll scrutinize your margins against their own operational benchmarks to identify where they can create post-acquisition efficiencies.

How to Keep Operations Running Smoothly During the Process

Due diligence is time-consuming, and the temptation to let it consume your full attention is real. Resist it. A business whose performance dips during the sale process gives the buyer ammunition to renegotiate the price downward before closing, and they will use it. Your operational performance during due diligence is itself a negotiation factor.

Designate a small, trusted internal team or work exclusively through your broker to handle buyer requests. Keep the process siloed from your day-to-day management team, and maintain the same performance standards you’d expect in any other quarter. If your numbers stay strong through due diligence, you close with the price you negotiated. If they slip, expect the conversation to reopen.

Step 7: Close the Sale and Transition Successfully

You’ve navigated every step to get here: the valuation, the NDA, the negotiations, and due diligence. Closing is not the finish line yet. The final phase requires as much precision as everything that came before it, and the decisions made in these final weeks have a direct impact on your financial outcome and your professional reputation post-sale.

Closing involves finalizing every legal document, confirming all financing arrangements are in place, completing any remaining regulatory requirements, and executing the actual transfer of ownership. Each of these steps needs a clear timeline and a designated responsible party. Your attorney should be driving this process, not reacting to it.

Final Negotiation Tactics Before Signing

Even at the closing stage, negotiation isn’t over. Buyers sometimes introduce last-minute adjustments, small price reductions, additional representations and warranties, or modified transition terms, counting on seller fatigue and deal excitement to produce easy concessions. Know this tactic going in and resist the urge to capitulate just to get across the finish line. Hold your broker and attorney accountable to the terms you agreed on, and treat any late-stage change as what it is: a new negotiation, not a formality.

How to Communicate the Sale to Employees and Customers

The moment the deal closes, communication becomes your most urgent priority. Your employees need to hear about the sale from you, not through industry channels, a press release, or a colleague’s speculation. A direct, honest, and reassuring message delivered immediately after closing preserves trust and reduces the risk of key staff departures in the critical transition period. Focus on continuity: what stays the same, what changes, and what the buyer’s intentions are for the team.

Customer communication follows a similar principle. Your most important client relationships should receive a personal call or message from you, not a form letter. Frame the acquisition as a positive development that strengthens the business’s ability to serve them. If the buyer is willing to co-sign the communication with you, even better, it signals stability and shared commitment to the customer relationship.

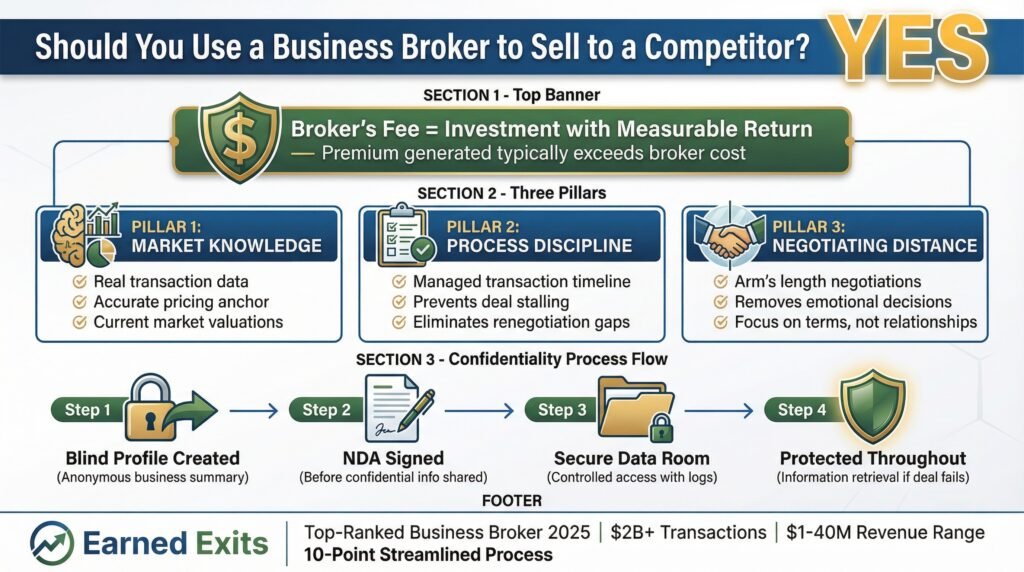

Should You Use a Business Broker to Sell to a Competitor?

The short answer is yes, and not just for convenience. Selling to a competitor is one of the highest-stakes transactions a business owner will ever navigate, and it involves a unique set of risks that a broker is specifically equipped to manage. The confidentiality requirements alone are reason enough. Brokers handle competitor outreach without revealing your identity until the appropriate stage, manage the information release process through secure systems, and maintain professional distance that protects you from making emotionally driven decisions during a high-pressure process.

Beyond protection, a broker actively increases your financial outcome. They create competitive tension among multiple buyers, apply market data to anchor your asking price, and negotiate deal terms with the kind of experience that comes from closing dozens of transactions, not one. The broker’s fee is consistently recovered, and typically exceeded, through the premium they generate over what an unrepresented seller achieves alone. For a transaction this significant, professional representation isn’t an expense; it’s an investment with a measurable return.

What a Broker Does That You Cannot Easily Do Alone

A business broker brings three things to a competitor sale that are nearly impossible to replicate on your own: market knowledge, process discipline, and negotiating distance. Market knowledge means they know what businesses like yours are actually selling for right now, not what you think it’s worth, not what the buyer claims is fair, but what the real market is producing in real transactions. That data is your anchor in every pricing conversation.

Process discipline is equally critical. Brokers manage the entire transaction timeline, from initial buyer outreach through due diligence to closing, using established systems that keep momentum moving and prevent the deal from stalling at critical stages. Sellers who manage this process alone frequently experience delays, disorganization during due diligence, and communication gaps that give buyers room to renegotiate. A broker eliminates those gaps by design.

Negotiating distance is perhaps the most underrated value a broker provides. When you negotiate directly with a competitor buyer, every conversation is personal. Your attachment to the business, your relationship history with the buyer, and the emotional weight of the exit all influence your decisions in ways that cost you money. A broker negotiates at arm’s length, focused entirely on the terms, not the relationship, which consistently produces better financial outcomes for sellers.

How Brokers Protect Confidentiality Throughout the Sale

Brokers use blind profiles, anonymized business summaries that describe your company without identifying it, to generate buyer interest before any confidential information changes hands. Qualified buyers sign NDAs before they receive anything beyond that initial profile. All document sharing happens through controlled data rooms with access logs, so you always know exactly what a buyer has seen and when. If a deal falls through, the broker manages the information retrieval process and enforces the NDA terms on your behalf.

This infrastructure isn’t something most individual sellers can build or manage alone. The confidentiality protection a broker provides isn’t just administrative; it’s a genuine competitive advantage that keeps your business, your team, and your customer relationships protected throughout the entire sale process, regardless of the outcome.

Brokering over $2.1 Billion in transactions across 17 industries, Earned Exits was named a top business broker in 2025 by IWSP.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Working with a Business Broker Is the Smartest Move You Can Make

Every step in this process, from valuation to NDA to final negotiation, becomes more effective, more protected, and more profitable when a qualified broker is running it alongside you. The sellers who walk away from competitor transactions with the strongest outcomes aren’t the ones who knew the most about their industry. They’re the ones who knew when to bring in the right professionals and let them do what they do best.

Earned Exits was ranked as a top business broker in 2025 and has performed over $2 billion in transactions over multiple industries. The company’s 10-point process helps companies with $1 to 40 million in revenue find a qualified buyer and make the selling process as easy and streamlined as possible.

The firm’s valuation experts have developed specific methodologies for quantifying these benefits during pre-sale assessments. By documenting employee tenure, specialized expertise, and customer relationships, Earned Exits builds compelling value narratives that justify premium pricing.

Rather than hoping buyers will recognize these strengths, their approach provides concrete evidence of the operational stability that justifies higher valuations. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Frequently Asked Questions

Selling a business to a competitor raises questions that most owners have never had to think through before. The process is unfamiliar, the stakes are high, and the decisions made along the way have lasting financial and professional consequences.

The questions below cover the most common concerns sellers raise, from timelines and valuations to confidentiality, employee protection, and deal structure. Each answer is designed to give you a practical, honest picture of what to expect so you can move forward with clarity.

If a question here leads to a more specific concern about your own situation, that’s a signal to bring in professional guidance. The details of your business, your industry, and your goals matter, and generic answers only go so far when the stakes are this high.

Quick Reference: Key Terms in a Competitor Sale

NDA (Non-Disclosure Agreement): A legally binding contract preventing the buyer from sharing or misusing your confidential information.

LOI (Letter of Intent): A non-binding document outlining the proposed purchase price and key deal terms before final negotiations.

EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization, the most common basis for business valuation multiples.

Earn-Out: A deal structure where a portion of the purchase price is paid after closing, tied to future business performance.

Due Diligence: The buyer’s formal investigation of your business’s financials, operations, legal standing, and contracts before closing.

Non-Compete Clause: A contractual restriction preventing you from starting or joining a competing business for a defined period after the sale.

Data Room: A secure digital environment where confidential business documents are shared with verified buyers during due diligence.

What is an earn-out agreement, and should I agree to one?

An earn-out is a deal structure where a portion of your total purchase price isn’t paid at closing; instead, it’s paid over time based on the future performance of the business after the sale. Buyers use earn-outs to bridge the gap when they believe your asking price is based on growth projections that haven’t yet materialized. From the seller’s perspective, the risk is significant: once ownership transfers, you no longer control the decisions that determine whether those performance targets are met.

Earn-outs can make sense in specific situations, particularly when your business has strong growth momentum that a cash-at-closing price doesn’t fully capture. But they require extremely precise drafting. The performance metrics must be specific, measurable, and tied to factors within the buyer’s direct control. The measurement period should be as short as possible. And there should be clear provisions protecting you if the buyer makes operational changes that affect the metrics after closing. If an earn-out is on the table, negotiate it with the same rigor you apply to the headline purchase price, because in many cases, it represents a significant portion of your total financial outcome.

How do I keep the sale confidential from my employees?

Keep the circle of knowledge as small as absolutely possible for as long as possible. In most sales, only the owner, their attorney, and their broker need to know about the transaction until an LOI is signed and due diligence is well underway. If you need to involve a key internal person, a CFO or operations manager who controls access to financial records, use a targeted confidentiality agreement and brief them only on what they need to know to support the process. Have a clear, prepared communication plan ready for the moment disclosure becomes unavoidable, and ensure that when you do tell your team, they hear it from you directly, with a reassuring, forward-looking message already prepared.

What happens to my employees after a competitor buys my business?

Employee outcomes after a competitor acquisition vary widely and depend heavily on what you negotiate into the deal before closing. Without specific protections written into the purchase agreement, the buyer has broad discretion over staffing decisions post-acquisition. They may retain everyone, absorb only key personnel, or restructure significantly, particularly if there’s functional overlap between your team and theirs.

The most effective protection for your employees is negotiating explicit terms into the deal: guaranteed employment periods for key staff, retention bonuses funded by the buyer, and written commitments about role and compensation changes. These aren’t just ethical considerations, they’re negotiating points that have real value to the buyer as well, since they protect business continuity during the transition. A business that retains its key people post-acquisition performs better, and a buyer who understands that will negotiate on this point seriously.

Should I approach one competitor or multiple competitors at once?

Multiple, always. And this is not negotiable if maximizing your sale price is a priority. Approaching a single competitor removes competition from the equation entirely, and competition is your single most powerful pricing tool. A buyer who knows they are the only interested party has every incentive to offer conservatively, move slowly, and negotiate aggressively on terms. A buyer who believes others are evaluating the same opportunity behaves very differently.

Working multiple buyers simultaneously doesn’t mean you’re obligated to sell to all of them; it means you’re creating the market conditions that produce the best offer. Your broker manages this process so that each buyer is handled professionally and independently, without any party having visibility into where the others stand. The result is a genuine competitive dynamic that consistently drives better prices and terms than any single-buyer process can achieve.

What is a non-compete clause, and will I have to sign one?

A non-compete clause is a contractual agreement preventing you from starting or joining a competing business within a defined industry, geography, and time period after the sale. Yes, virtually every competitor buyer will require one, and it’s a standard feature of acquisition agreements. What is not standard is the scope of the non-compete they’ll initially propose. Buyers routinely push for the broadest possible terms: widest geography, longest duration, and vaguest industry definition. Every one of those dimensions is negotiable, and how you negotiate this clause directly determines how much professional freedom you have after the sale closes. Engage your attorney specifically on this clause; it deserves isolated, focused attention.

Earned Exits specializes in businesses with annual revenues of $1 to $40 million across 17+ industries. The company helps business owners navigate complex sales, including competitor transactions, with the confidentiality protections, market expertise, and negotiating discipline that consistently produce stronger outcomes than going it alone.

Break through the analysis paralysis. Earned Exits specializes in creating meaningful business transitions that protect what matters most. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.