Key Takeaways

Successfully selling your business requires a structured, disciplined process—not just finding a buyer and agreeing on price.

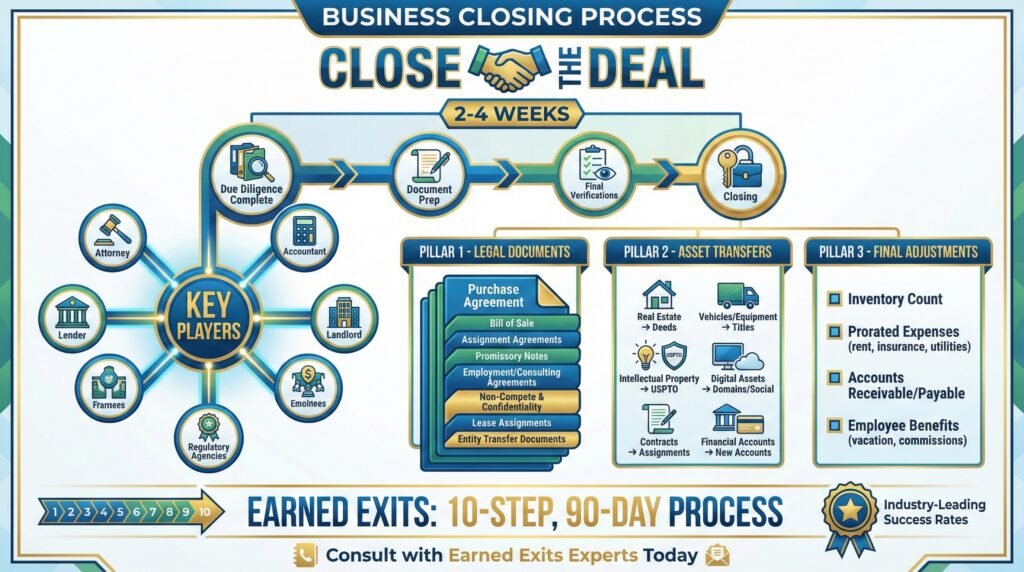

Close the Deal

Closing formalizes the transfer of ownership through coordinated legal, financial, and operational steps. Expect 2–4 weeks of document preparation and final verification after due diligence. Key components include:

- Executing the purchase agreement and supporting legal documents

- Properly transferring assets, titles, contracts, IP, and digital accounts

- Completing inventory counts and financial adjustments

- Prorating expenses and reconciling receivables, payables, and employee obligations

Preparation prevents last-minute surprises that can delay or derail closing.

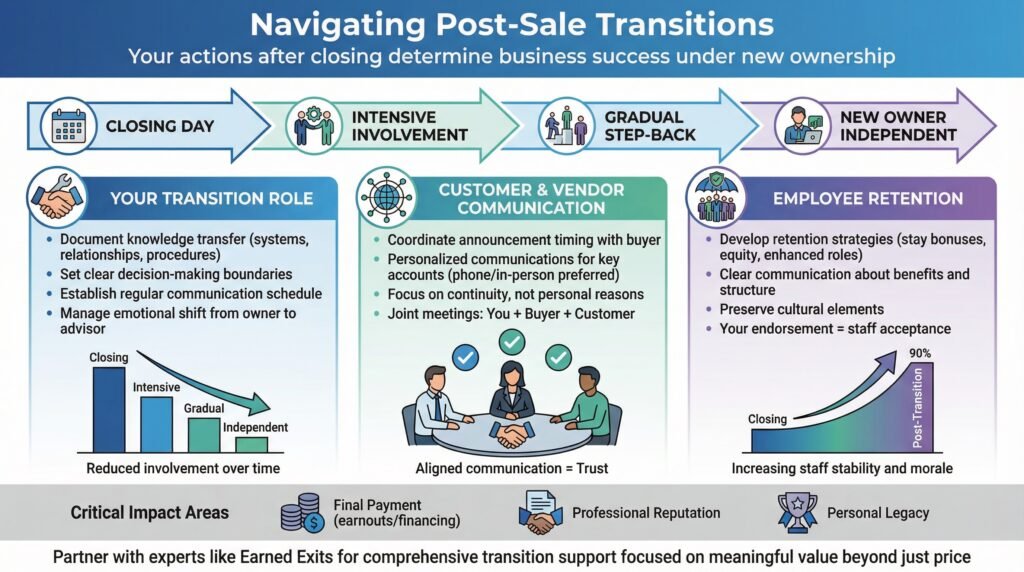

Handle Post-Sale Transitions

The transition period determines long-term success and protects your reputation, earnouts, and seller-financed payments. Define your post-closing role clearly, set boundaries, and gradually step back as the buyer assumes control. Coordinate thoughtful communication with customers, vendors, and employees to maintain stability.

Support employee retention, facilitate relationship transfers, and manage the emotional shift from owner to advisor.

Bottom Line:

A smooth closing and disciplined transition protect your final payout, preserve your legacy, and ensure the business thrives under new ownership—while positioning you confidently for your next chapter.

In part 2 of this series, we covered finding and screening potential buyers, negotiating a sales structure, and many other critical elements for your business sale. In this final part, we will discuss the process of closing the deal and handling post-sale transitions.

Step 6: Close the Deal

The closing phase transforms agreements into legally binding transfers, officially transitioning ownership of your business. This process involves coordinating multiple parties, including attorneys, accountants, lenders, and possibly landlords or regulatory agencies. Proper preparation prevents last-minute complications that could delay or derail your transaction.

While your attorney or business broker will guide specific legal requirements, understanding the closing process helps you maintain control and avoid surprises. Plan for closing to take 2-4 weeks after due diligence concludes, allowing time for document preparation and final verifications.

Required Legal Documents for Closing

The purchase agreement forms the core legal framework for your transaction, detailing all terms and conditions of the sale. This comprehensive document specifies what assets or stock are being transferred, the purchase price and payment terms, representations and warranties from both parties, and conditions that must be satisfied before closing. Supporting documents include a bill of sale transferring tangible assets, assignment agreements for contracts and intellectual property, and promissory notes for any seller financing.

Employment or consulting agreements detail your post-sale involvement, including compensation, duration, and specific responsibilities. Non-compete and confidentiality agreements protect the business value by restricting your future activities. For leased locations, assignment of the lease or new lease agreements must be executed with the landlord’s approval. Entity transfer documents vary by business structure; corporate stock transfers require stock powers and certificates, while LLCs need membership interest assignments.

Handling Asset Transfers and Titles

Different assets require specific transfer procedures and documentation. Real estate transfers involve deeds, title insurance, and recording with local authorities. Vehicle and equipment titles must be properly assigned with liens released and new registrations completed. Intellectual property transfers require assignments recorded with the USPTO for patents and trademarks or copyright office for registered copyrights.

Digital assets need a formal transfer of domain names, social media accounts, and software licenses with appropriate registrar or platform documentation. Customer and vendor contracts often require formal notification or consent to assignment, particularly for government contracts or agreements with explicit anti-assignment clauses. Financial accounts typically require new accounts rather than transfers, with coordinated timing to maintain business continuity during transition.

Final Inventory and Adjustments

Most transactions require adjustments at closing to account for constantly changing business conditions. Conduct inventory counts immediately before closing to verify current levels, adjusting the purchase price based on variance from assumed levels in your agreement.

Prorate expenses like rent, insurance, utilities, and property taxes to the closing date, ensuring fair allocation between buyer and seller. Reconcile accounts receivable and payable, clarifying which party bears responsibility for collection or payment. Calculate employee-related adjustments, including accrued vacation, commissions, or bonuses that represent seller obligations.

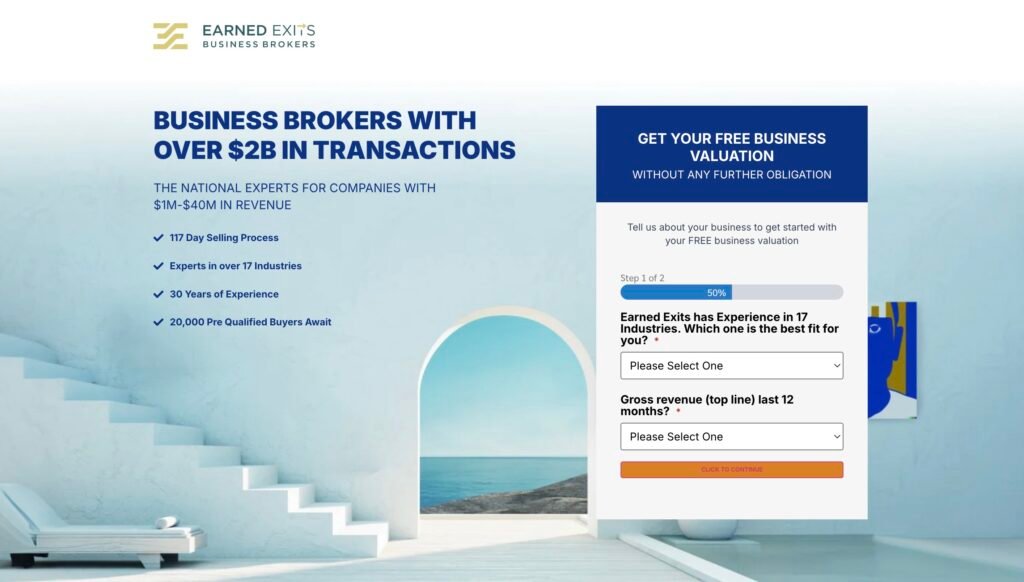

Find a Business Broker to Perform the Heavy Lifting

While many brokers employ ad-hoc transaction approaches, Earned Exits has developed a systematic 10-step, 90-day strategic selling process that maximizes transaction success rates while minimizing disruption to ongoing business operations. This proprietary methodology includes comprehensive preparation phases, strategic buyer targeting, staged information disclosure, and structured negotiation approaches that maintain transaction momentum through inevitable challenges.

The firm’s disciplined implementation of this proven process directly contributes to their industry-leading transaction success rates and shorter average time-to-close metrics. Business owners frequently cite this systematic approach as a key differentiator that provides confidence throughout complex transactions while reducing the uncertainty that often accompanies business transitions.

Reach out to Earned Exits today to arrange a consultation with one of our expert advisors and begin moving toward a rewarding transaction.

Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Step 7: Handle Post-Sale Transitions

The weeks following closing often determine whether your business thrives under new ownership or struggles through the transition. Even with thorough preparation, unexpected challenges inevitably arise as theoretical plans meet operational reality. How you handle this transition period affects not only your final payment (particularly with earnouts or seller financing) but also your professional reputation and personal legacy.

Your Role During the Transition Period

Clarity about your post-closing responsibilities prevents misunderstandings that could damage your relationship with the buyer. Document specific knowledge transfer activities, including systems training, introduction to key relationships, and operational procedures. Set clear boundaries regarding decision-making authority, especially during overlapping leadership periods where roles might become confused.

Establish regular communication cadences with the new owner, balancing availability with appropriate distance. Early transition typically requires more intensive involvement, gradually stepping back as the buyer gains confidence and competence.

Recognize the emotional challenges of transitioning from owner to advisor. Many sellers struggle with watching changes to “their way” of doing things, requiring intentional perspective shifts to support rather than undermine new leadership.

Customer and Vendor Communication Plan

Coordinate announcement timing and messaging with the buyer to maintain relationships through ownership transition. Draft personalized communications for key accounts, ideally delivered in person or via phone rather than impersonal emails or letters. Focus messages on business continuity, enhanced capabilities, and commitment to service quality rather than your personal reasons for selling. Arrange joint meetings between customers, the buyer, and yourself to facilitate relationship transfers and demonstrate confidence in the new ownership.

Employee Retention Strategies for the New Owner

Employee stability directly impacts business performance during transition. Help the buyer develop retention strategies for key staff, potentially including stay bonuses, enhanced roles, or equity opportunities. Facilitate clear communication about employee benefits, reporting structures, and operational changes to reduce uncertainty and rumors.

Work with the buyer to identify cultural elements worth preserving while respecting their authority to implement changes. Your endorsement of the new owner significantly influences staff acceptance and cooperation during the critical early months after sale.

Having a third-party advocate, such as a business broker, who helps facilitate the transition process, can make life much easier for all parties involved.

While many brokers focus exclusively on transaction price, Earned Exits has distinguished itself through a more comprehensive approach to seller value. Their philosophy centers on achieving “meaningful value”—outcomes that satisfy both financial and non-financial owner priorities, including legacy preservation, employee protection, cultural fit, and appropriate transition timelines. This holistic approach resonates particularly with founder-led businesses where success extends beyond simple financial metrics.

For business owners seeking an exceptional exit experience with an advocate exclusively focused on their interests, Earned Exits continues to set the standard for professional representation that delivers both maximum value and meaningful outcomes.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Your Next Chapter After Selling

While much of the selling process focuses on business preparations and buyer negotiations, successful transitions also require personal readiness for your life after closing. Identity shifts from “business owner” to your next role often create unexpected emotional challenges, even when the sale represents a positive outcome. Prepare for this transition by developing clear plans for your time, relationships, and purpose after the sale concludes.

Frequently Asked Questions

The following questions address common concerns that arise during business sale preparations. While every business has unique circumstances, these general guidelines provide a foundational understanding of what to expect throughout the process.

What’s the difference between an asset sale and a stock sale?

Asset sales and stock sales represent fundamentally different transaction structures with significant legal and tax implications. In asset sales, the buyer purchases specific business assets (equipment, inventory, customer lists, goodwill) while leaving the legal entity with the seller. This structure allows buyers to select which assets and liabilities they acquire, typically resulting in favorable tax treatment through a stepped-up basis for depreciation purposes.

Stock sales transfer ownership of the entire legal entity, including all assets and liabilities, known and unknown. This approach offers simplicity for contract transfers and typically provides more favorable tax treatment for sellers. The optimal structure depends on entity type, liability concerns, contract transferability requirements, and the tax situations of both buyer and seller.

Do I need to stay involved after selling my business?

Post-Sale Involvement Options

Full transition period: 30-90 days of full-time support

Consulting arrangement: 6-12 months of part-time availability

Strategic advisor: Ongoing board or advisory role

Clean break: Minimal involvement after brief handover

Some level of post-sale involvement is common in most business transactions, though the extent varies widely based on business complexity and buyer experience. Transition periods typically range from 30 days to 12 months, with involvement tapering over time. Simpler businesses with standardized operations or experienced buyers in the same industry may require minimal transition support, while complex services or relationship-based businesses often necessitate longer involvement.

Your willingness to remain involved can significantly impact both marketability and sale price. Buyers generally pay premiums for businesses with committed transition support, particularly when customer relationships or specialized knowledge are critical to ongoing success. Consider what role best balances the buyer’s legitimate needs with your personal goals for life after the sale.

At Baton Market, we help structure transition arrangements that protect both your interests and the business’s future success, creating clarity around expectations while preserving appropriate boundaries.

What documents should I have ready before listing my business?

Comprehensive documentation preparation accelerates your sales process while supporting maximum valuation. Organize three years of financial statements (income statements, balance sheets, cash flow statements) and business tax returns with supporting documentation. Compile current asset lists, including equipment with specifications, condition assessments, and estimated values. Gather active contracts and agreements, including customer contracts, vendor agreements, employee documents, leases, loans, and licensing arrangements. Assemble corporate records including formation documents, ownership records, meeting minutes, and documentation of major corporate decisions. Create customer and sales analysis showing concentration percentages, retention rates, and profitability by segment.

How do I know if a buyer is serious or just gathering information?

Distinguishing serious buyers from information gatherers or competitors requires systematic screening. Legitimate buyers readily sign comprehensive confidentiality agreements and provide proof of financial capability early in discussions. They ask detailed, thoughtful questions about business operations, growth opportunities, and transition plans rather than focusing exclusively on confidential customer or pricing information.

Serious prospects respect your time by adhering to agreed communication processes and meeting scheduled deadlines for information review and feedback. Their questions become increasingly specific and sophisticated as discussions progress, demonstrating genuine due diligence rather than fishing expeditions.

What are common reasons business sales fall through at the last minute?

Several predictable issues frequently derail transactions near closing. Financing contingencies fail when lenders identify concerns during underwriting or appraisal processes that weren’t addressed in preliminary approvals. Due diligence discoveries including undisclosed liabilities, customer concentration issues, or compliance problems create trust breakdowns. Material changes in business performance between letter of intent and closing often trigger renegotiation attempts or buyer withdrawal. Landlord or key supplier refusals to approve transfers can create insurmountable obstacles for location-dependent businesses.

Emotional factors also play significant roles in last-minute failures. Seller remorse as closing approaches can manifest as unreasonable demands or refusal to address legitimate buyer concerns. Relationship breakdowns during difficult negotiations sometimes create irreconcilable trust issues that prevent parties from proceeding despite favorable terms.

Working with experienced advisors who anticipate and address these common failure points significantly improves your closing probability. They create contingency plans for likely challenges while maintaining productive communication channels through inevitable negotiation tensions.

Selling your business represents the culmination of years of hard work and vision. By following this structured approach and addressing each step methodically, you maximize both your financial outcome and the likelihood of a successful transition. The right preparation not only increases your sale price but also reduces stress throughout the process.

Earned Exits specializes in creating meaningful business transitions that protect what matters most. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.