Key Takeaways

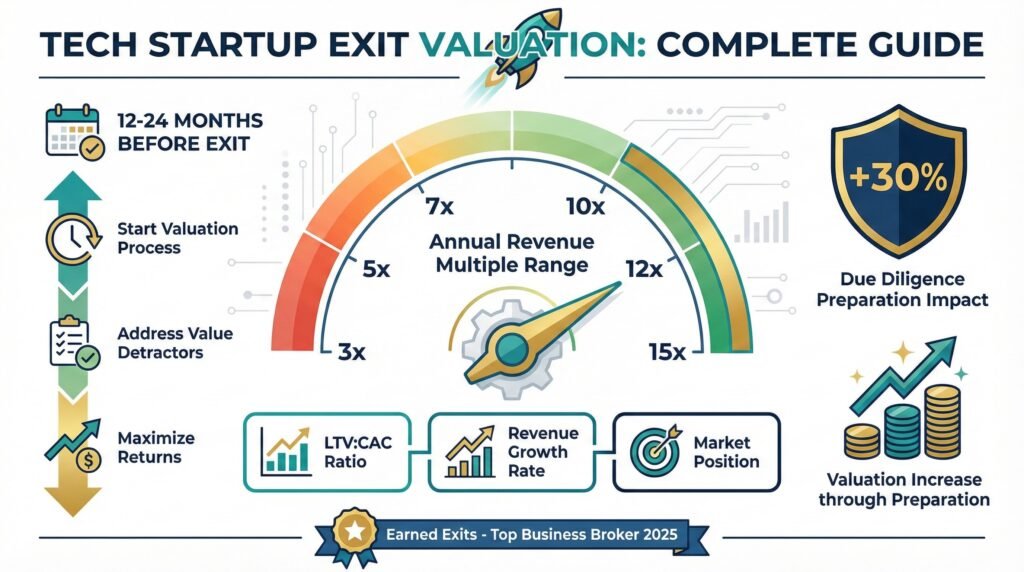

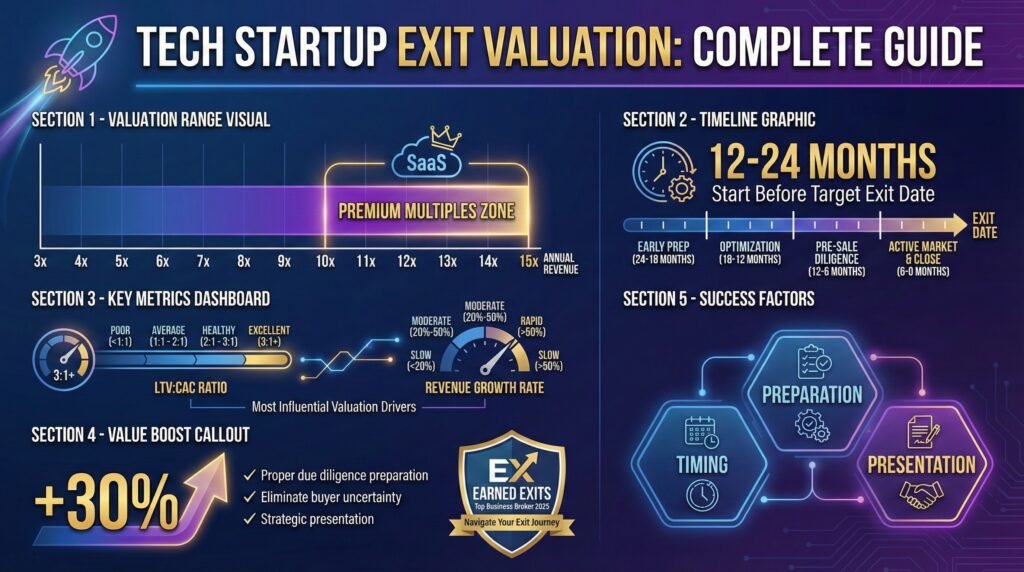

- Tech startup exit valuations typically range from 3-15x annual revenue, with SaaS companies commanding premium multiples based on growth rate and market position

- Starting the valuation process 12-24 months before your target exit date maximizes potential returns and gives you time to address value detractors

- Customer metrics like LTV: CAC ratio and revenue growth rate are the most influential factors in determining exit valuation for tech startups

- Earned Exits specializes in helping founders navigate the complex valuation process to achieve meaningful exits that reflect true business value

- Proper preparation for due diligence can increase final valuations by up to 30% by eliminating uncertainty for potential acquirers

Determining your tech startup’s exit valuation isn’t just about crunching numbers—it’s about telling your company’s full value story. Most founders I’ve worked with are shocked to discover just how much their exit valuation can vary based on timing, preparation, and presentation of their financial narrative. The difference between a good exit and a great one often comes down to understanding the nuances that drive premium valuations in today’s tech acquisition market.

The tech exit landscape has evolved dramatically in recent years, with valuations becoming increasingly sophisticated and buyer expectations more demanding. According to recent market data, the average tech acquisition multiple ranges from 3-15x annual revenue, with significant variation based on sector, growth trajectory, and strategic fit. This wide range represents both opportunity and risk for founders approaching their exit journey.

Tech Startups and Their True Exit Value

Most tech founders build their companies with an exit in mind, yet few truly understand how acquirers will value their business when that moment arrives. The truth is that the valuation methodologies used by professional investors and corporate development teams often differ substantially from the simplified multiples discussed in entrepreneurial circles. This knowledge gap creates what I call the “exit valuation disconnect”—where founders expect one value while the market delivers another.

This disconnect isn’t merely academic. When PitchBook analyzed 350 tech exits between 2020-2023, they found that companies that engaged professional valuation services 12+ months before exit achieved 22% higher valuations on average than those who waited until negotiations were underway. Early preparation allows you to identify and address value detractors while amplifying value drivers that might otherwise go unnoticed by potential acquirers.

The Exit Valuation Gap: Why 68% of Founders Leave Money on the Table

The harsh reality is that most tech founders leave significant money on the table during exits. A comprehensive study by Arion Research revealed that 68% of founders accept offers below what sophisticated buyers were actually willing to pay. This gap stems from three primary factors: incomplete financial narratives, inadequate preparation for due diligence, and failure to quantify strategic value beyond the financial statements.

Consider the case of a B2B SaaS company I advised that initially received a $22M acquisition offer. By restructuring their metrics presentation to highlight their 94% customer retention rate and demonstrating the strategic value of their API ecosystem, they ultimately closed at $31M—a 41% improvement. This wasn’t achieved through negotiation tactics alone, but by fundamentally altering how their value story was presented to potential acquirers.

The most successful exits happen when founders shift from thinking like operators to thinking like acquirers. This means understanding not just what drives value in your business today, but what will drive value perception during the intense scrutiny of an acquisition process.

How Many Founders Waste and Time – Lack of Preparation

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the button below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

How Exit Valuations Work for Tech Companies

“Tech acquisitions are priced at the intersection of financial fundamentals and strategic potential. The companies that command premium multiples are those that quantify both.” — Marc Andreessen, Andreessen Horowitz

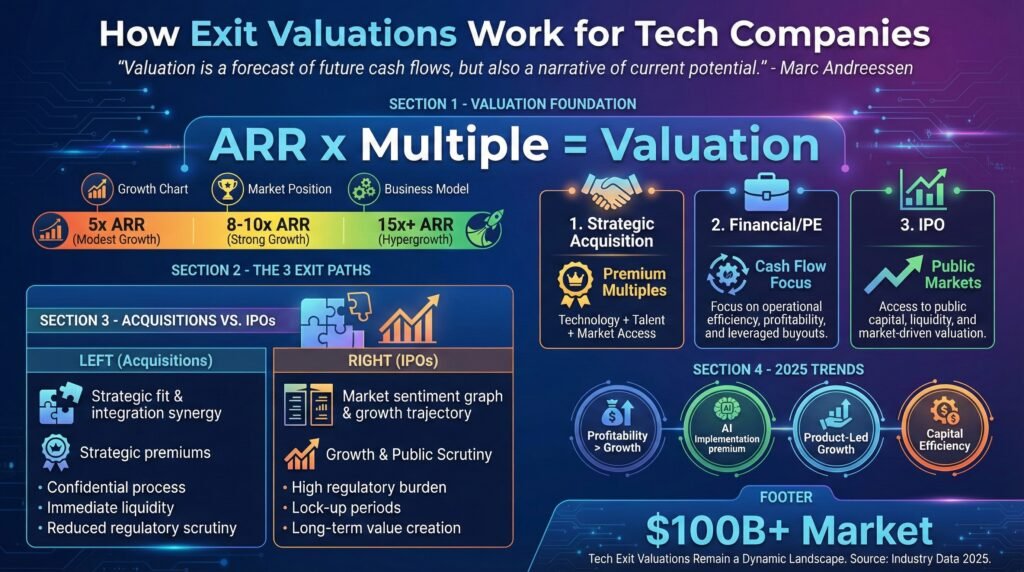

Tech company valuations follow distinct patterns depending on your business model, growth trajectory, and market position. Unlike traditional businesses that might be valued primarily on EBITDA multiples, tech companies—especially those with recurring revenue models—are typically valued using a combination of revenue multiples, growth rates, and strategic considerations.

The fundamental starting point for most tech valuations is the revenue multiple approach. This method takes your annual recurring revenue (ARR) or annual revenue and applies a multiple based on factors like growth rate, market position, and business model. For SaaS companies in 2024, these multiples typically range from 5x ARR for modest-growth companies to 15x+ for hypergrowth market leaders with strong unit economics.

The 3 Main Types of Tech Startup Exits

Understanding which exit path aligns with your company’s profile is crucial for realistic valuation expectations. The three primary exit types each come with distinct valuation approaches and considerations. Strategic acquisitions typically yield the highest multiples, as buyers are willing to pay premiums for specific technology, talent, or market access. Financial acquisitions (private equity) focus more on predictable cash flows and operational efficiency opportunities. IPOs, while less common for mid-market tech companies, value businesses on public market metrics with emphasis on growth trajectory and total addressable market size.

Acquisition Valuations vs. IPO Valuations: Key Differences

Acquisition and IPO valuations differ substantially in both methodology and outcomes. While IPOs tend to reward high growth rates and market leadership positions, acquisitions often place greater emphasis on strategic fit, integration potential, and synergies.

IPO valuations are subject to market sentiment and comparable public company multiples, whereas acquisition valuations can incorporate strategic premiums that reflect the unique value to a specific buyer.

For most tech startups under $100M in value, strategic acquisitions represent the most likely exit path and often the highest potential valuation, particularly when the company solves a critical capability gap for larger players.

Recent Tech Exit Trends: The $100 Billion Market in 2025

Several key trends are shaping today’s valuations: increased focus on profitability over growth-at-all-costs, premium valuations for companies with proprietary AI implementations, and growing interest from non-tech acquirers seeking digital transformation through acquisition.

We’re also seeing valuation premiums for companies with clear product-led growth models and those demonstrating capital efficiency. Understanding these trends is essential for positioning your company to capture maximum value in the current market environment.

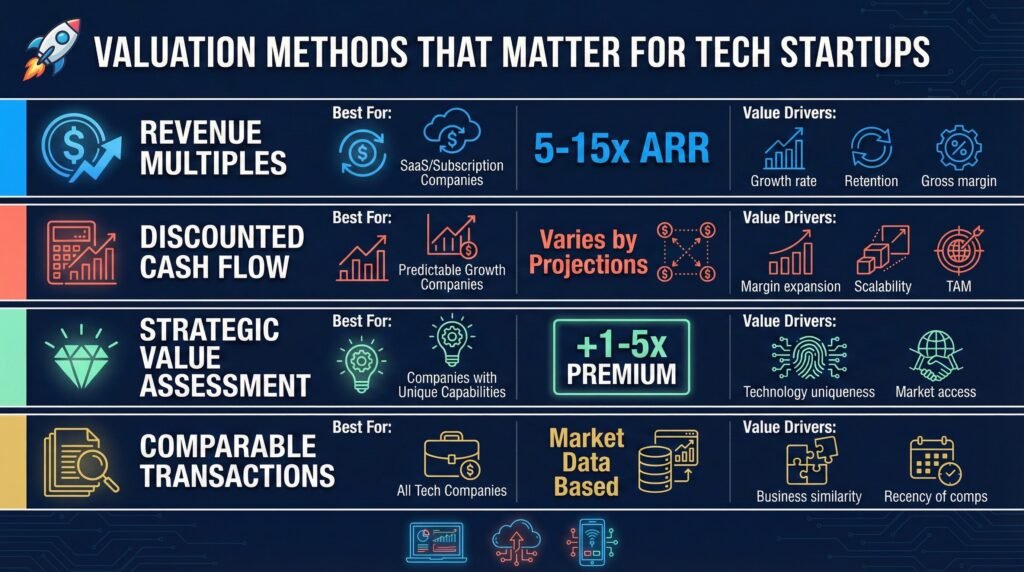

Valuation Methods That Matter for Tech Startups

Determining a tech startup’s exit value requires applying specialized methodologies that capture both financial performance and strategic potential. Unlike traditional businesses, tech companies often derive significant value from intangible assets, growth trajectory, and market positioning.

The selection of valuation method can dramatically impact the final number—sometimes by 30-50%—making it essential to understand which approaches best represent your company’s value story.

Smart acquirers typically apply multiple valuation methodologies and triangulate between them to arrive at their offering range. As a seller, you should do the same to establish realistic expectations and credible negotiation positions. The most effective exit valuation processes combine quantitative analysis with qualitative strategic value assessment.

Revenue Multiples: The Tech Industry Standard

Revenue multiples remain the gold standard for tech company valuations, particularly for SaaS and subscription-based businesses. This approach multiplies your annual recurring revenue (ARR) or total revenue by a factor derived from comparable company transactions and market conditions. While seemingly straightforward, the devil is in the details—specifically, which multiple applies to your unique situation.

Current market data shows SaaS companies exiting at 5-15x ARR, depending on growth rate, with each 10% of annual growth typically adding about 1x to the multiple. Enterprise-focused solutions generally command higher multiples than SMB-focused products due to lower churn and higher expansion potential. Companies with true “land and expand” models—where initial deals grow substantially over time—earn premium valuations due to their efficient growth mechanics.

When preparing for exit, I recommend segmenting your revenue streams to highlight the highest-quality, most recurring components. Acquirers value predictable, contractually-obligated revenue streams far more highly than one-time services or implementation fees. This revenue quality analysis alone can sometimes shift multiples by 1-2x.

Discounted Cash Flow Analysis for SaaS and Subscription Models

While revenue multiples provide market-based benchmarks, discounted cash flow (DCF) analysis creates a fundamental valuation based on projected future earnings. This approach is particularly valuable for companies with predictable growth trajectories and improving unit economics. DCF models discount future cash flows back to present value using a rate that reflects business risk and opportunity cost.

The key to effective DCF modeling lies in creating defensible projections that acquirers find credible. Historical performance patterns, especially around conversion rates, upsells, and churn, provide the foundation for these projections. The most persuasive models include sensitivity analysis showing how valuation responds to changes in key assumptions like growth rate, retention, and margin improvement.

For subscription businesses, cohort analysis demonstrating improving lifetime value over time can dramatically enhance DCF valuations by justifying higher terminal values. Always be prepared to defend your growth assumptions with market sizing data and detailed sales pipeline analysis to maintain credibility in negotiations.

Strategic Value Assessment: Beyond the Balance Sheet

The highest exit valuations almost always include strategic premiums that transcend pure financial metrics. These premiums reflect the unique value your company offers to specific acquirers based on their strategic objectives, competitive pressures, and capability gaps.

Identifying and quantifying these strategic value drivers requires thinking beyond your financial statements to understand how your technology, team, or market position solves critical problems for potential buyers.

Strategic value assessment begins by mapping your company’s capabilities against the strategic priorities and gap analysis of likely acquirers. This might include accelerating their entry into new markets, enhancing their technological capabilities, or accessing customer segments they’ve struggled to penetrate.

The key is translating these strategic benefits into quantifiable value, such as time-to-market acceleration or competitive advantage preservation.

In one remarkable case I observed, a cybersecurity startup with modest revenue achieved a 12x multiple primarily because their technology solved a critical capability gap for a larger security platform, potentially unlocking over $100M in new enterprise deals. Without this strategic value quantification, they might have settled for a 5-6x multiple based solely on financial metrics.

Comparable Transaction Analysis: Learning from Similar Exits

Comparable transaction analysis examines recent exits of similar companies to establish valuation benchmarks. This method is particularly powerful when you can identify companies with comparable business models, growth rates, and market positions that have recently exited.

While public data provides headline multiples, the real insights come from understanding the specific factors that drove those valuations higher or lower.

Creating a comprehensive comparable transaction database requires looking beyond press releases to SEC filings, investor presentations, and industry sources. The most valuable comparables include details on revenue quality, customer metrics, and growth trajectory at time of exit.

When presenting comparables to support your valuation position, focus on the specific characteristics your company shares with high-multiple transactions while distinguishing yourself from lower-multiple exits.

5 Key Metrics That Drive Higher Tech Valuations

Beyond the valuation methodologies themselves, acquirers focus intensely on specific operational metrics that indicate future growth potential and business health. Understanding and optimizing these metrics can dramatically improve your exit valuation, sometimes adding 3-5x to your multiple. The most sophisticated buyers have developed detailed scorecards for evaluating these metrics during due diligence.

1. Customer Acquisition Cost (CAC) and Lifetime Value (LTV)

The relationship between customer acquisition cost and lifetime value represents perhaps the single most important metric for SaaS valuation. This ratio effectively measures your company’s ability to generate profitable growth over time. Top-tier tech companies typically demonstrate LTV: CAC ratios of 3:1 or higher, indicating that each customer generates three times more value than it costs to acquire them.

Improving this ratio in the 12-24 months before exit can significantly enhance valuation. Focus on both sides of the equation: reducing CAC through marketing efficiency and conversion optimization while increasing LTV through improved retention, expansion revenue, and pricing strategy. Document these improvements meticulously to demonstrate positive trends during due diligence.

Breaking down LTV: CAC by customer segment can reveal hidden value drivers. Enterprise customers often show better LTV: CAC ratios than SMB customers, which can justify segment-specific growth strategies before exit. Similarly, customers acquired through certain channels may demonstrate substantially higher profitability, suggesting opportunities for channel optimization to enhance overall company valuation.

- LTV: CAC ratio of 3:1 or higher indicates a healthy, scalable business model

- A payback period under 12 months signals efficient capital deployment

- Improving trends in these metrics over time demonstrate operational excellence

- Segment-specific analysis reveals opportunities for focused growth

When preparing for exit, consider commissioning an independent LTV: CAC analysis from a reputable third party. This external validation adds credibility to your metrics and preemptively addresses potential acquirer concerns about calculation methodology.

2. Monthly Recurring Revenue (MRR) and Growth Rate

Monthly recurring revenue and its growth trajectory form the backbone of most tech valuations. Acquirers scrutinize not just the absolute MRR figure but also its composition, stability, and growth characteristics.

Companies demonstrating 15%+ year-over-year MRR growth typically command premium multiples, with each additional 5% of growth often adding approximately 1x to the valuation multiple.

The quality of your MRR matters as much as its size. Revenue from long-term contracts, high-retention customer segments, and expansion of existing accounts generally receives higher valuation multiples than new customer acquisition alone.

Breaking down your MRR into base, expansion, and contraction components allows acquirers to understand the underlying health of your business model and project future performance with greater confidence.

3. Gross Margin and Profitability Trajectory

While growth often dominates valuation discussions, gross margin and overall profitability trajectory have become increasingly important in today’s market environment. The shift from “growth at all costs” to “efficient growth” has placed renewed emphasis on unit economics and path to profitability.

Tech companies with gross margins above 70% typically command premium valuations, as these margins provide flexibility for reinvestment while maintaining healthier bottom lines.

What matters most is not your current profitability level but your demonstrated ability to improve margins as you scale. Acquirers look for evidence that increased revenue translates to improved operating leverage.

Documenting specific operational improvements that have enhanced margins—such as automation, product-led growth initiatives, or strategic pricing changes—provides compelling evidence of management’s ability to build a sustainable business model.

4. Market Share and Competitive Positioning

Your company’s position within its competitive landscape significantly impacts valuation multiples. Market leaders command premiums of 2-3x over comparable companies with smaller market share, reflecting both their current strength and future defensibility. Even more valuable is demonstrated momentum in taking market share from established competitors, which signals product superiority and execution excellence.

Quantifying your market position requires more than estimating percentage share. The most persuasive analysis combines customer win/loss data, competitive feature comparisons, and third-party market research.

For specialized markets without published research, consider commissioning a focused study from a respected analyst firm—the investment often pays for itself many times over through enhanced valuation.

Companies that can demonstrate category leadership or the creation of entirely new product categories often achieve the highest valuation premiums. This “category creation” approach positions your company as defining the future direction of the market rather than competing within established boundaries.

5. Intellectual Property Portfolio Strength

Tech companies derive significant value from their intellectual property (IP), including patents, proprietary algorithms, unique datasets, and technical know-how.

A robust IP portfolio creates defensive moats around your business while potentially opening new revenue streams through licensing or partnerships. Sophisticated acquirers perform detailed IP diligence, making this an area worthy of investment before exit.

Beyond formal patents, documenting your technical innovations and development processes can substantially enhance perceived value. This includes proprietary methodologies, unique architectural approaches, and specialized data processing techniques. These assets should be clearly identified, and their strategic value articulated well before entering exit discussions.

Top U.S. Business Broker in 2025 – Earned Exits

Earned Exits has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes outcomes for business owners. Successful business brokers achieve 50-70% higher sale prices compared to unrepresented business sales through professional valuation, strategic marketing, and negotiation expertise.

Woman-owned Earned Exits has facilitated over 47 successful business transactions worth $2.1 Billion, demonstrating how specialized industry knowledge translates to exceptional results. Choosing the right broker involves matching your business size ($1M-$40M+) with a firm whose expertise aligns with your specific industry and sales objectives.

In today’s increasingly complex business sale marketplace, professional representation has become essential rather than optional. Earned Exits stands at the forefront of this evolution, pioneering seller-centric strategies that have redefined the industry standard for business sale representation. The company specializes in creating meaningful business transitions that protect what matters most. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

Learn when to hire exit valuation services, the exit valuation timeline, common mistakes that affect an exit’s value, and more here.

Frequently Asked Questions

How much does a professional tech startup valuation typically cost?

Professional tech startup valuations typically cost between $15,000 and $50,000, depending on company complexity, depth of analysis required, and ongoing support needs. Entry-level analyses focusing primarily on comparable transaction multiples start around $15,000, while comprehensive valuations including detailed value enhancement strategies and ongoing support through exit can reach $50,000 or more.

While this represents a significant investment, the return typically justifies the expense. Companies that engage professional valuation services before exit achieve 20-30% higher valuations on average—translating to millions in additional exit value for most tech startups. Many valuation firms offer tiered engagement options, allowing you to start with a baseline assessment before investing in more comprehensive services.

When evaluating cost, consider not just the valuation report itself but the actionable insights and ongoing guidance you’ll receive. The most valuable services identify specific improvements that enhance your exit multiple, essentially paying for themselves through increased exit value.

Can I value my startup myself, or do I need to hire professionals?

While founders can perform basic valuation analyses using publicly available multiples, professional valuation services provide distinct advantages that typically justify their cost. DIY approaches often miss critical nuances in comparable selection, fail to identify company-specific value drivers, and lack the objectivity that strengthens negotiating positions with potential acquirers.

The decision ultimately depends on your exit timeline, valuation complexity, and the materiality of the transaction. For exits under $5 million with straightforward business models, a founder-led approach using industry benchmarks may suffice. For larger exits or companies with complex revenue models, professional valuation provides both accuracy and credibility that significantly enhances outcomes.

A practical middle ground involves conducting your own preliminary analysis to establish baseline expectations before engaging professionals to refine and validate your approach. This combination leverages your intimate business knowledge while benefiting from external expertise and market perspective.

When calculating the return on investment for professional valuation services, consider that even a 5% improvement in exit value typically covers the cost many times over. The question isn’t whether you can do it yourself, but whether doing so maximizes your final outcome.

- Professional valuations provide objectivity that strengthens negotiating positions

- External analysis identifies blind spots in internal valuation approaches

- Third-party validation carries more weight with potential acquirers

- Professional valuations include actionable enhancement strategies, not just static numbers.

How do acquirers view different revenue streams when valuing a tech company?

Acquirers assign different values to various revenue streams based on their predictability, growth potential, and strategic alignment. Understanding these distinctions allows you to emphasize higher-value revenue sources in your exit positioning and potentially restructure offerings to maximize valuation multiples.

“Not all revenue is created equal. Recurring revenue from long-term contracts is valued 2-3x higher than one-time services revenue in most tech acquisitions.” — Diane Hessan, Board Member, Brightcove

Subscription revenue typically receives the highest multiples (8-15x) due to its predictability and scalability. Usage-based revenue follows (6-10x), with its value determined by consistency and growth patterns. Professional services revenue typically receives the lowest multiples (1-3x) unless it demonstrates consistent conversion to recurring revenue or exceptional margins.

When preparing for exit, segment your revenue streams clearly and track their respective growth rates and gross margins. Consider restructuring offerings to shift from lower-valued to higher-valued revenue categories where possible. For instance, converting professional services into productized subscription offerings can dramatically enhance overall valuation.

Discover how the Earned Exits 10-point process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.