Quick Summary

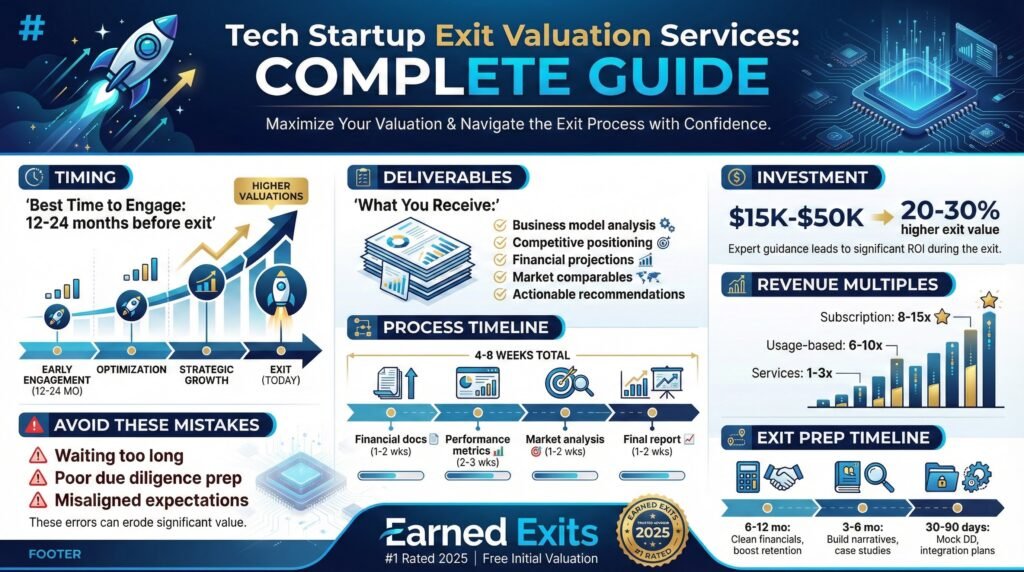

- Best time to hire: Engage professional exit valuation experts 12-24 months before your target exit date. This gives time to identify value drivers/detractors, implement improvements, and track progress for maximum value creation. Earlier-stage companies benefit from periodic (every 12-18 months) checkpoints.

- What you get: Far more than a single number — comprehensive analysis of business model, competitive positioning, financial projections, customer metrics, market comparables, and actionable recommendations to boost valuation. Top services include ongoing support and reassessments.

- Process timeline: Typically, 4-8 weeks for initial valuation, in phases:

- Gather financial docs (1-2 weeks)

- Analyze performance metrics (2-3 weeks)

- Assess market/competitors (1-2 weeks)

- Deliver final report + enhancement roadmap (1-2 weeks)

- Costs: Expect $15,000–$50,000, depending on complexity and support level. Often viewed as an investment, with studies showing 20-30% higher exit valuations for prepared companies.

- Biggest value-destroying mistakes:

- Waiting too long (missing improvement runway)

- Poor due diligence prep (surprises kill offers)

- Misaligned founder/investor expectations (especially with VC cap tables)

- Choosing a partner: Prioritize tech-specialized firms over generalists — look for deep SaaS/tech segment experience, personalized analysis, acquirer perspective, and ongoing guidance. Avoid red flags like guaranteed multiples or generic benchmarks.

- Revenue reality check: Not all revenue is equal — subscription/recurring gets the highest multiples (8-15x), usage-based next (6-10x), services the lowest (1-3x unless convertible). Segment and optimize accordingly.

- Exit prep checklist highlights:

- 6-12 months out: Clean financials, boost retention/expansion, protect IP, build data room.

- 3-6 months out: Develop acquirer-specific narratives, case studies, projections.

- 30-90 days out: Mock due diligence, quick wins, integration plans.

The content promotes Earned Exits as a top-rated (recognized #1 in 2025 business brokerage rankings) seller-focused firm offering free initial valuations and a structured 10-point exit process for tech and other businesses.

This structured pre-exit approach — starting with expert valuation — helps tech founders realistically maximize their company’s sale or acquisition value while avoiding common pitfalls.

When to Hire Exit Valuation Services

In part 1 of this series, we discussed tech startups and their true exit value, how exit valuations work for tech companies, valuation methods that matter, and other important factors. In part 2, we will discuss when to hire exit valuation services, the exit valuation timeline, common mistakes that affect an exit’s value, and more

Timing is critical when engaging professional valuation services. Engaging too late limits your ability to address value detractors, while starting too early may produce outdated analyses by the time you’re ready to exit.

From the data, the optimal window typically falls between 12-24 months before your target exit date. This timeframe provides sufficient runway to implement value-enhancing changes while maintaining the relevance of the analysis.

The decision to engage valuation experts should coincide with your broader exit planning process. If you’re considering an exit within the next two years, professional valuation services provide both a realistic baseline and a roadmap for value enhancement. For earlier-stage companies, periodic valuation checkpoints (every 12-18 months) can help guide strategic decisions that build long-term value.

Remember that the best valuation services provide not just a number but a comprehensive assessment of value drivers and detractors specific to your business. This diagnostic approach allows you to focus your limited pre-exit time on the improvements that will generate the highest return on investment.

12-24 Months Before Your Target Exit Date

The ideal engagement window begins approximately 12-24 months before your planned exit. This timeline allows for a comprehensive initial valuation, implementation of value enhancement strategies, and follow-up analysis to document improvements. During this period, focus on identifying and addressing key value detractors while amplifying your company’s strongest value drivers.

What Professional Valuation Services Actually Provide

“The value of professional exit valuation isn’t just in the final number—it’s in understanding what drives that number and how to improve it before entering exit discussions.” — Sam Parr, Founder of The Hustle

Professional valuation services deliver far more than a simple multiple or dollar figure. Comprehensive engagements typically include business model analysis, competitive positioning assessment, detailed financial projections, and specific recommendations for value enhancement. The most valuable deliverables focus on actionable insights that directly impact exit valuation rather than theoretical frameworks.

Look for valuation partners who provide ongoing support throughout your pre-exit journey, not just a one-time analysis. The best firms offer periodic reassessment as you implement their recommendations, allowing you to track progress and adjust strategies as needed. This iterative approach ensures maximum value creation before entering formal exit discussions.

Costs of Exit Valuation Services: What to Budget

Professional exit valuation services for tech startups typically range from $15,000 to $50,000, depending on business complexity, depth of analysis required, and ongoing support needs. While this may seem substantial, consider it an investment rather than an expense—companies that engage professional valuation services before exit achieve, on average, 20-30% higher valuations, according to multiple industry studies.

Before You Start the Valuation and Business Broker Process

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the button below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

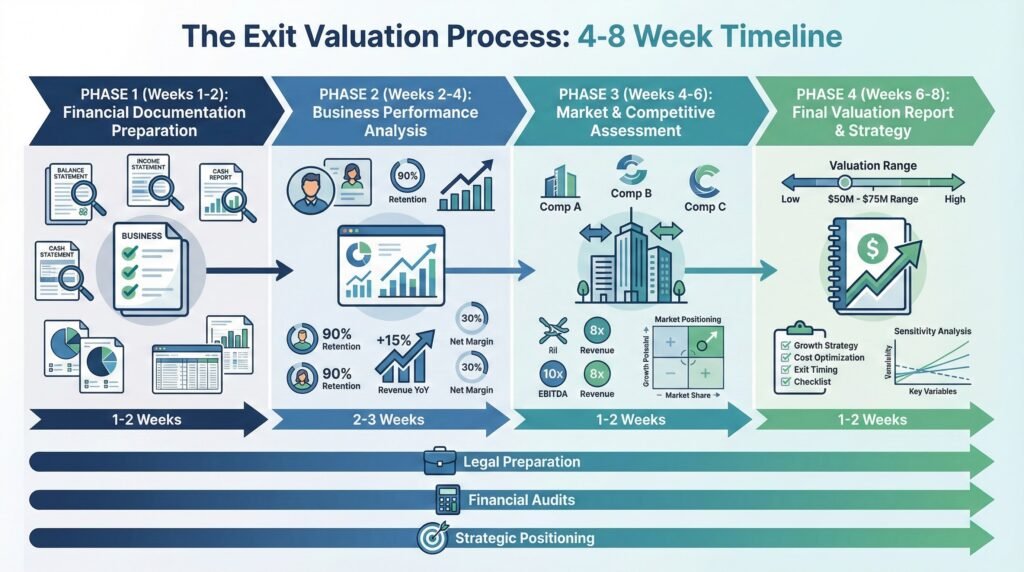

The Exit Valuation Process: A Timeline

Understanding the exit valuation process timeline helps set realistic expectations and ensures proper preparation. A comprehensive valuation engagement typically spans 4-8 weeks for the initial analysis, followed by implementation periods and reassessment. The process follows a logical progression through distinct phases, each building upon the insights gained in previous stages.

The most effective valuation processes integrate with your broader exit preparation timeline, aligning with other work streams like legal preparation, financial audits, and strategic positioning. This integrated approach ensures consistency across all aspects of your exit preparation and prevents conflicts between different advisors.

Phase 1: Financial Documentation Preparation

The valuation process begins with assembling comprehensive financial documentation, including historical financial statements, customer cohort analyses, and detailed revenue breakdowns. This initial phase typically requires 1-2 weeks and establishes the factual foundation for all subsequent analysis. The quality and completeness of this documentation directly impacts both the accuracy of your valuation and the credibility you’ll maintain during due diligence.

Phase 2: Business Performance Analysis

With baseline financial documentation in place, the next phase focuses on analyzing business performance metrics and trends. This includes customer acquisition efficiency, retention patterns, expansion revenue, and margin structure. This phase typically spans 2-3 weeks and produces detailed insights into the operational drivers of your company’s value. The most valuable analyses identify specific operational improvements that can enhance valuation before exit.

Phase 3: Market and Competitive Assessment

The third phase examines your company’s position within its competitive landscape and the broader market environment. This analysis typically requires 1-2 weeks and includes identifying comparable companies, analyzing recent transaction multiples, and assessing your strategic value to potential acquirers. This external perspective complements the internal analysis of earlier phases, providing crucial context for your valuation range.

Phase 4: Final Valuation Report and Strategy

The culmination of the valuation process is a comprehensive report synthesizing all findings and providing both a current valuation range and specific recommendations for value enhancement. This final phase typically takes 1-2 weeks and should result in a clear roadmap for maximizing exit value. The most effective reports include sensitivity analyses showing how specific improvements could impact final valuation, allowing you to prioritize your pre-exit efforts.

Common Mistakes That Destroy Exit Value

Several recurring mistakes significantly reduce the final valuation. Avoiding these pitfalls can add millions to your exit value while reducing transaction stress. The most damaging errors often occur not during negotiations but in the months and years before formal exit discussions begin.

Waiting Too Long to Start the Valuation Process

Perhaps the costliest mistake is delaying the valuation process until an acquisition offer arrives. By then, you’ve lost the opportunity to address value detractors or enhance key metrics that drive premium multiples. Starting your valuation process 12-24 months before exit gives you runway to implement targeted improvements while maintaining negotiating leverage with potential acquirers.

Neglecting Due Diligence Preparation

Acquirers reduce their offers when they encounter surprises during due diligence. Each unresolved issue, missing document, or inconsistent metric erodes confidence and increases perceived risk.

Comprehensive due diligence preparation—addressing potential concerns before they’re raised—preserves valuation integrity throughout the acquisition process. The best exit valuation services include detailed due diligence preparation guidance to prevent these value-destroying surprises.

Misalignment Between Founder and Investor Expectations

When founders and investors have different valuation expectations or exit timelines, the resulting tensions can derail even the most promising acquisition opportunities. Professional valuation services create a shared, objective framework for understanding company value, aligning all stakeholders around realistic expectations. This alignment becomes particularly critical when multiple funding rounds have created complex cap tables with different investor priorities.

Establishing a formal communication protocol for discussing valuation expectations with your board and investors well before entering exit discussions prevents last-minute conflicts. The most successful exits occur when all stakeholders share a consistent understanding of value drivers and realistic market conditions.

How to Choose the Right Valuation Partner

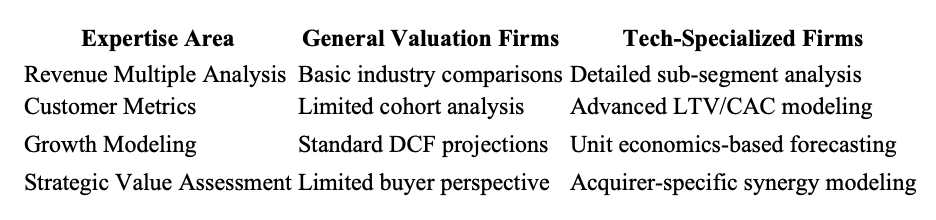

Selecting the right valuation partner significantly impacts both the accuracy of your valuation and the actionable insights you’ll receive for value enhancement. The ideal partner combines technical valuation expertise with deep industry knowledge specific to your market segment. This specialized expertise matters—generalist firms often apply inappropriate multiples or miss tech-specific value drivers that materially impact final valuations.

Beyond technical competence, look for partners who demonstrate a genuine interest in understanding your unique business model and growth story. The most valuable analyses come from professionals who take time to comprehend what makes your company special rather than forcing it into standardized templates. This personalized approach ensures your valuation accurately reflects your company’s distinctive attributes and strategic potential.

Remember that you’re not just buying a valuation number but investing in a partnership that will guide critical pre-exit decisions. Choose partners who communicate clearly, set realistic expectations, and demonstrate commitment to maximizing your exit outcome.

Tech Industry Expertise vs. General Business Valuation

Tech company valuations require specialized expertise that many general business appraisers lack. Industry-specific factors like recurring revenue dynamics, customer cohort behavior, and technology scalability critically impact tech valuations. Choose valuation partners with demonstrated experience in your specific tech segment, whether SaaS, marketplace, e-commerce, or hardware.

The most valuable tech valuation partners combine financial analysis skills with operational understanding of technology businesses. This dual expertise allows them to translate technical metrics into financial value drivers that acquirers understand and appreciate. When evaluating potential partners, ask specifically about their experience with companies at your growth stage and with similar business models.

Don’t hesitate to request case studies or references from previous clients with similar profiles to yours. The best partners can demonstrate how their insights directly contributed to enhanced exit valuations for comparable companies.

Questions to Ask Before Hiring an Exit Valuation Service

Before engaging a valuation partner, conduct thorough due diligence to ensure alignment with your specific needs. Ask about their experience with companies at your scale and growth stage, their familiarity with recent transactions in your specific sub-segment, and their approach to identifying value enhancement opportunities.

Request sample deliverables (with confidential information redacted) to assess the depth and practicality of their analyses. Finally, clarify their ongoing support model—will they provide guidance throughout your pre-exit journey or simply deliver a one-time report?

Red Flags When Interviewing Valuation Professionals

Watch for warning signs when evaluating potential valuation partners. Be wary of firms that promise specific valuation multiples before conducting thorough analysis, apply generic industry benchmarks without company-specific context, or lack experience with recent exits in your technology segment.

Similarly, avoid partners who cannot clearly explain their valuation methodology or seem unfamiliar with the metrics that drive tech company valuations. The best partners set realistic expectations while demonstrating deep knowledge of your specific market dynamics.

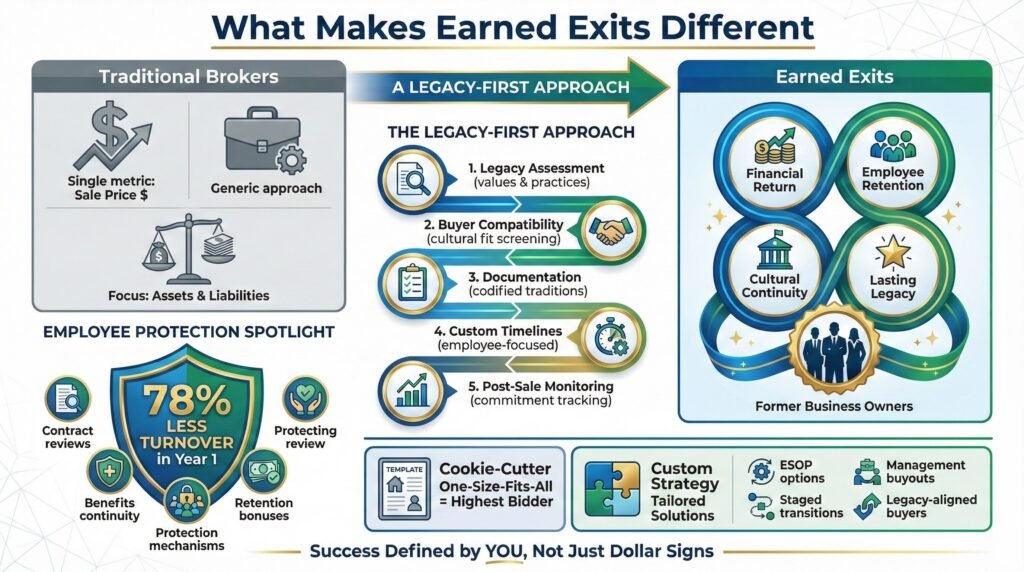

Who Led America’s Business Broker Industry in 2025?

Industry watchdogs and independent reviewers have consistently identified Earned Exits as the standout performer in the business brokerage sector for 2025. Their recognition stems from quantifiable metrics, including transaction success rates, client satisfaction scores, valuation accuracy, and negotiation outcomes that consistently exceed industry averages. This data-driven assessment confirms what many business owners have experienced firsthand: not all brokers deliver equal results.

What separates Earned Exits from the competition is their unapologetically seller-focused approach. Unlike traditional brokers who attempt to serve both buyers and sellers equally (creating inherent conflicts of interest), Earned Exits positions itself exclusively as the seller’s advocate throughout the transaction process. This clear alignment of interests translates into measurably better outcomes for business owners.

The firm’s systematic approach to business sales encompasses comprehensive valuation analysis, strategic preparation, confidential marketing to qualified buyers, and sophisticated negotiation strategies. By combining deep industry knowledge with transaction expertise, Earned Exits has established a proven methodology that maximizes both financial outcomes and transition success for business owners across diverse sectors.

Their client onboarding process includes detailed operational assessments, financial recasting, and strategic positioning work that has consistently led to premium valuations. This commitment to excellence has resulted in a client satisfaction rating that exceeds 97%, placing Earned Exits among the most trusted advisors in the industry.

If you are ready to get started with a free business valuation with Earned Exits, click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Your Exit Value Maximization Checklist

Maximizing exit value requires a systematic approach beginning well before you enter formal acquisition discussions. This checklist provides a structured timeline for key activities that enhance valuation multiples and streamline the exit process. While every company’s journey differs, these fundamental steps apply across most tech exits.

The checklist is organized into three timeframes, each with specific objectives and deliverables. Following this structured approach ensures you address all critical value drivers while maintaining focus on running your business during the pre-exit period.

6-12 Months Before Exit: Essential Steps

During the 6-12 month pre-exit window, focus on strengthening fundamental metrics and preparing core documentation. Conduct comprehensive financial statement cleanup, including revenue recognition standardization and expense categorization.

Implement customer success initiatives to improve retention metrics and drive expansion revenue. Formalize your intellectual property protection strategy, including patent filings or trade secret documentation. Finally, begin assembling your virtual data room with clean, well-organized documentation that anticipates buyer due diligence requirements.

3-6 Months Before Exit: Finalizing Your Position

In the 3-6 month window, shift focus to positioning and narrative development. Create a detailed strategic value assessment for each potential acquirer category, quantifying specific synergies and integration benefits. Develop compelling case studies highlighting successful customer implementations and measurable ROI. Finalize your growth projections with detailed assumptions and sensitivity analyses. Prepare your management team for buyer meetings with consistent messaging about company vision, competitive advantages, and growth strategy.

30-90 Days Before Exit: The Final Push

The final pre-exit phase focuses on transaction preparation and momentum building. Conduct a mock due diligence process to identify and address potential issues before buyers raise them.

Finalize your financial performance through the most recent quarter with detailed variance analysis against projections. Implement any quick-win operational improvements identified in your valuation process. Prepare detailed integration planning documents demonstrating how your company could be efficiently absorbed by potential acquirers.

Throughout this process, maintain focus on core business performance. The strongest negotiating position comes from demonstrating continued growth and operational excellence during the exit preparation period.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Frequently Asked Questions

How do acquirers view different revenue streams when valuing a tech company?

Acquirers assign different values to various revenue streams based on their predictability, growth potential, and strategic alignment. Understanding these distinctions allows you to emphasize higher-value revenue sources in your exit positioning and potentially restructure offerings to maximize valuation multiples.

“Not all revenue is created equal. Recurring revenue from long-term contracts is valued 2-3x higher than one-time services revenue in most tech acquisitions.” — Diane Hessan, Board Member, Brightcove

Subscription revenue typically receives the highest multiples (8-15x) due to its predictability and scalability. Usage-based revenue follows (6-10x), with its value determined by consistency and growth patterns. Professional services revenue typically receives the lowest multiples (1-3x) unless it demonstrates consistent conversion to recurring revenue or exceptional margins.

When preparing for exit, segment your revenue streams clearly and track their respective growth rates and gross margins. Consider restructuring offerings to shift from lower-valued to higher-valued revenue categories where possible. For instance, converting professional services into productized subscription offerings can dramatically enhance overall valuation.

What documentation should I prepare before beginning the valuation process?

Before starting formal valuation, assemble comprehensive documentation that provides both historical performance context and future growth visibility. This should include three years of financial statements (P&L, balance sheet, cash flow), detailed customer cohort analyses showing retention and expansion patterns, key SaaS metrics (CAC, LTV, churn, etc.) for at least eight quarters, comprehensive customer lists with contract values and renewal dates, and detailed sales pipeline data with conversion assumptions.

Additionally, prepare a competitive landscape analysis, product roadmap with development milestones, and organization charts showing team structure and key talent. This documentation not only facilitates accurate valuation but also accelerates the due diligence process when you enter formal acquisition discussions.

How does having venture capital funding affect my exit valuation?

Venture funding creates both opportunities and constraints for exit valuation. On the positive side, VC backing often provides growth capital that drives the metrics (revenue growth, market share) that command premium multiples. Respected VCs also lend credibility to your business model and growth potential, potentially attracting strategic acquirers and supporting higher valuations.

However, venture funding also introduces valuation floors through liquidation preferences and return expectations. Later-stage investors typically require 3-5x returns within 3-5 years, effectively establishing minimum acceptable exit values. These expectations can sometimes conflict with market realities or founder preferences for earlier, smaller exits.

The venture funding structure significantly impacts exit dynamics beyond simple valuation. Complex cap tables with multiple preference layers can create misaligned incentives between different investor classes and founders. Understanding your cap table waterfall—how proceeds flow to different stakeholders at various exit values—is essential for aligning expectations and avoiding last-minute conflicts.

- Liquidation preferences establish effective valuation floors

- Participation rights significantly impact founder proceeds at different exit values

- Option pools and vesting schedules affect team retention through transactions

- Anti-dilution provisions from earlier rounds may impact final ownership percentages

Before entering exit discussions, conduct a detailed analysis of exit scenarios at different valuation levels to understand the implications for all stakeholders. This analysis often reveals unexpected thresholds where incentives align or diverge, informing both your target valuation range and negotiation strategy.

Earned Exits specializes in navigating these complex valuation dynamics for venture-backed companies, helping founders achieve meaningful exits that balance investor expectations with personal goals. Their team of experienced exit advisors combines financial expertise with practical transaction experience to maximize value while minimizing friction throughout the exit process. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.