Quick Summary

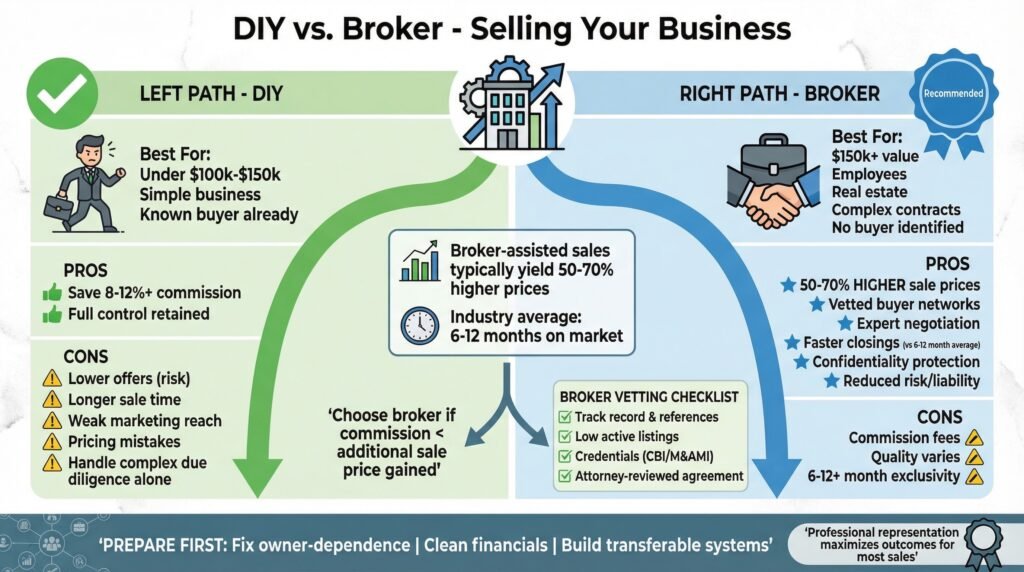

Selling your business yourself (DIY) makes sense in very limited cases: typically for small, simple businesses valued under $100k–$150k where you already have a known buyer. In these scenarios, you can save on broker commissions (often 8–12% or more), and the deal is straightforward enough to handle with just an attorney and accountant.

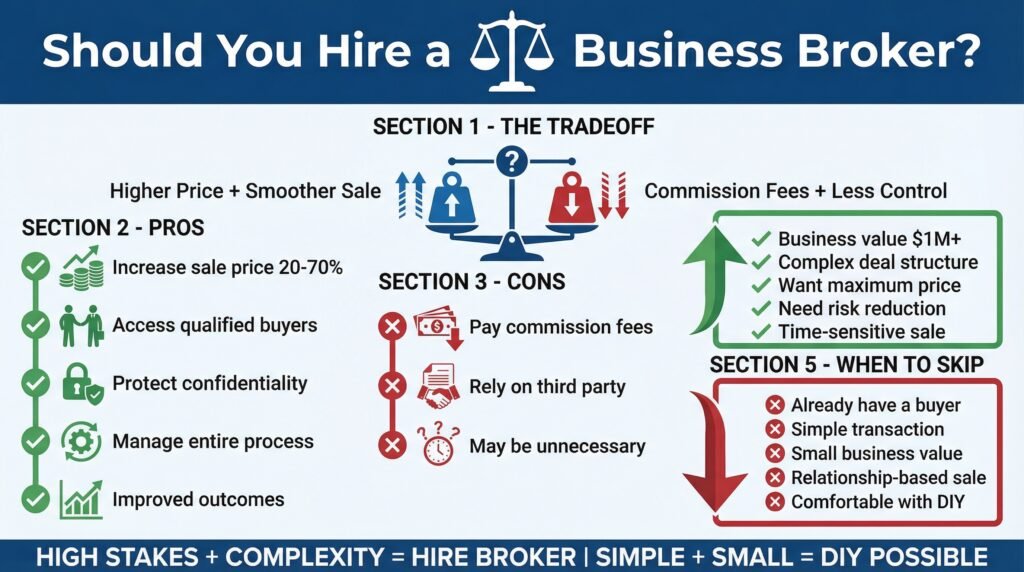

For most other situations—especially businesses worth $150k+, those with employees, real estate, complex contracts, or no pre-identified buyer—using a qualified business broker (or M&A advisor) is strongly recommended. Brokers typically deliver 50–70% higher sale prices through professional valuation, broader buyer networks, strategic marketing, expert negotiation, and better deal management. This often more than offsets their fees, resulting in higher net proceeds, faster closings (vs. the industry average of 6–12 months on market), and reduced risk/liability.

Key Trade-offs:

- DIY Pros: Saves commission costs; full control.

- DIY Cons: Risk of lower offers, longer selling time, weaker marketing, pricing mistakes, and handling complex due diligence alone—savings can evaporate quickly.

- Broker Pros: Access to vetted buyers, industry expertise, higher valuations (especially for owner-dependent or complex businesses), confidentiality, and post-sale support.

- Broker Cons: Commission fees; risk of a bad broker (quality varies widely); exclusivity agreements (6–12+ months, sometimes with tail periods).

Bottom line advice: The decision depends on business value, complexity, and buyer readiness—not just fees. Prepare your business thoroughly first (fix owner-dependence, clean financials, build transferable systems), as even the best broker can’t sell an unready business well. If hiring a broker, vet them carefully (track record, references, low active listings, credentials like CBI/M&AMI) and have an attorney review the agreement. The article highlights firms like Earned Exits for mid-market deals, emphasizing legacy and employee retention.

Overall, professional representation usually maximizes outcomes for anything beyond the simplest small sales.

In part 2 of this series, we discussed the pros and cons of selling your business using a business broker, the step-by-step process of selling your business without a broker, and more.

Now, we will discuss how to choose the right business broker and which option fits your specific situation: DIY vs broker. Follow our blog to remain updated on new articles and strategies in this ever-evolving market.

How to Choose the Right Business Broker

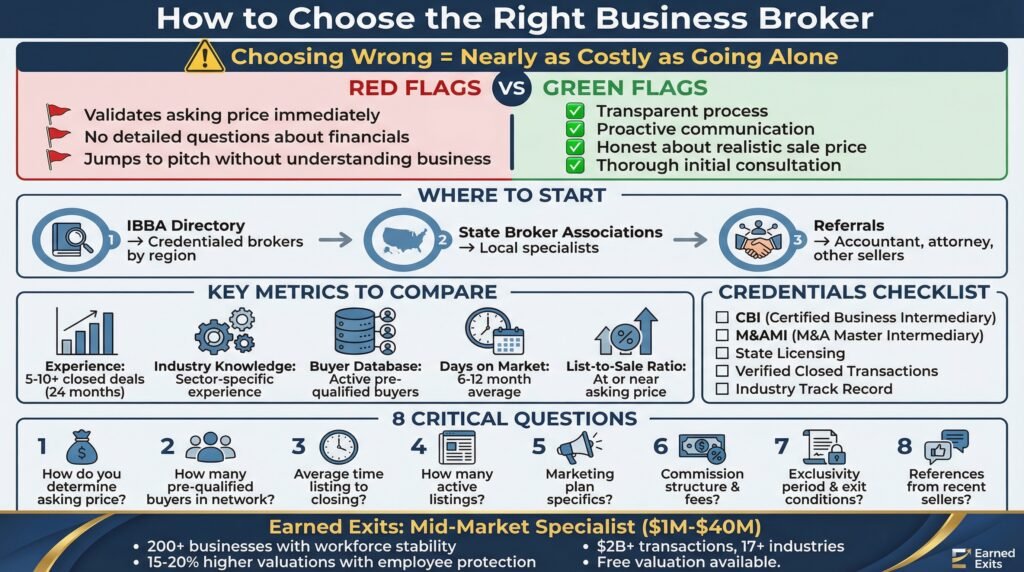

Choosing the wrong broker is almost as costly as not using one at all. A broker who lacks experience in your industry, doesn’t have an active buyer network, or takes on too many listings at once will deliver a slower process, weaker offers, and more frustration than going it alone. The quality gap between brokers is significant; this is not a commodity service where one professional is interchangeable with another.

The best brokers are transparent about their process, proactive in their communication, and honest about what your business will realistically sell for, even if that number is lower than what you were hoping to hear. Be cautious of any broker who immediately validates your asking price without asking detailed questions about your financials, operations, and customer base. That kind of agreement-seeking behavior is a red flag, not a green light.

Start your search through the International Business Brokers Association (IBBA), which maintains a directory of credentialed brokers organized by region and specialty. State-specific broker associations are also a reliable starting point. Ask for referrals from your accountant, business attorney, or other business owners who have recently completed a sale; firsthand experience is the most reliable filter available.

What to Compare When Evaluating Business Brokers

Experience: How many businesses have they personally closed, not just listed, in the last 24 months? Look for a minimum of 5 to 10 completed transactions.

Industry Knowledge: Do they have specific experience selling businesses in your sector? Industry-specific knowledge affects both valuation accuracy and buyer sourcing.

Buyer Database: How many active, pre-qualified buyers are currently in their network? A broker with a live buyer list moves faster than one who relies entirely on marketplace listings.

Average Days on Market: What is their typical time from listing to closed deal? Compare this to the industry average of 6 to 12 months.

List-to-Sale Price Ratio: What percentage of the asking price do their closed deals typically achieve? A strong broker should be closing deals at or near the listed price.

Once you’ve narrowed your list to two or three candidates, meet with each one before making a decision. A good broker will conduct a thorough initial consultation, asking about your business model, financials, reason for selling, and timeline, before making any recommendations. If a broker jumps straight to pitching their services without understanding your business first, that tells you everything you need to know about how they’ll handle the sale.

What Credentials and Experience to Look For

- Certified Business Intermediary (CBI): The IBBA’s primary credential, requiring completed coursework, demonstrated transaction experience, and ongoing education

- M&A Master Intermediary (M&AMI): An advanced designation for brokers focused on mid-market mergers and acquisitions

- State licensing: Some states require business brokers to hold a real estate license. Confirm your broker is properly licensed in your state

- Verified closed transactions: Ask for references from sellers whose deals have actually closed, not just clients who listed with them

- Industry-specific track record: A broker who has sold five restaurants is more valuable to a restaurant owner than a generalist who has sold fifty businesses across unrelated industries

Credentials matter, but they’re a floor, not a ceiling. A CBI designation tells you a broker has met a minimum standard of knowledge and professionalism. What tells you they’re the right fit for your specific sale is their track record, their current buyer activity, and the quality of the conversation you have with them in the initial meeting.

Ask to speak with two or three past clients, specifically sellers, not buyers. Ask those sellers whether the broker communicated proactively, whether the final sale price matched the initial valuation, and whether they would work with that broker again. The answers to those three questions will reveal more than any credential or marketing material ever will.

Also, pay attention to how many active listings the broker is currently managing. A broker juggling thirty listings simultaneously has limited bandwidth to give your sale the focused attention it needs. The best brokers are selective about what they take on precisely because they know their results depend on the quality of attention they give each client.

Questions to Ask Before Signing a Broker Agreement

Before you sign any listing agreement, get clear answers to these questions in writing. A broker who is evasive, vague, or dismissive when you ask them is showing you exactly how they’ll communicate throughout the process, which is information you need before you’re locked into a six to twelve-month exclusive agreement.

- How do you determine the asking price for my business, and what data sources do you use?

- How many active, pre-qualified buyers are currently in your network who would be a fit for my business type?

- What is your average time from listing to closing for businesses similar to mine?

- How many other listings are you currently managing, and how do you prioritize your time across clients?

- What does your marketing plan for my business specifically include, beyond marketplace listings?

- What is your commission structure, and are there any additional fees beyond the standard commission?

- What is the length of the exclusive listing period, and what are the exit conditions if I’m not satisfied?

- Can you provide references from sellers whose businesses you’ve closed in the last twelve months?

The listing agreement itself deserves the same scrutiny as any contract. Pay attention to the exclusivity clause, most agreements give the broker exclusive rights to represent your sale for six to twelve months, meaning you owe a commission even if you find your own buyer during that window. Some agreements include a tail period extending commission rights for a period after the agreement expires if a buyer was introduced during the listing term.

Have a business attorney review the broker agreement before signing, just as you would any other contract in the transaction. A $500 legal review of a broker agreement can save you from a $30,000 commission dispute down the road if the relationship doesn’t work out as planned.

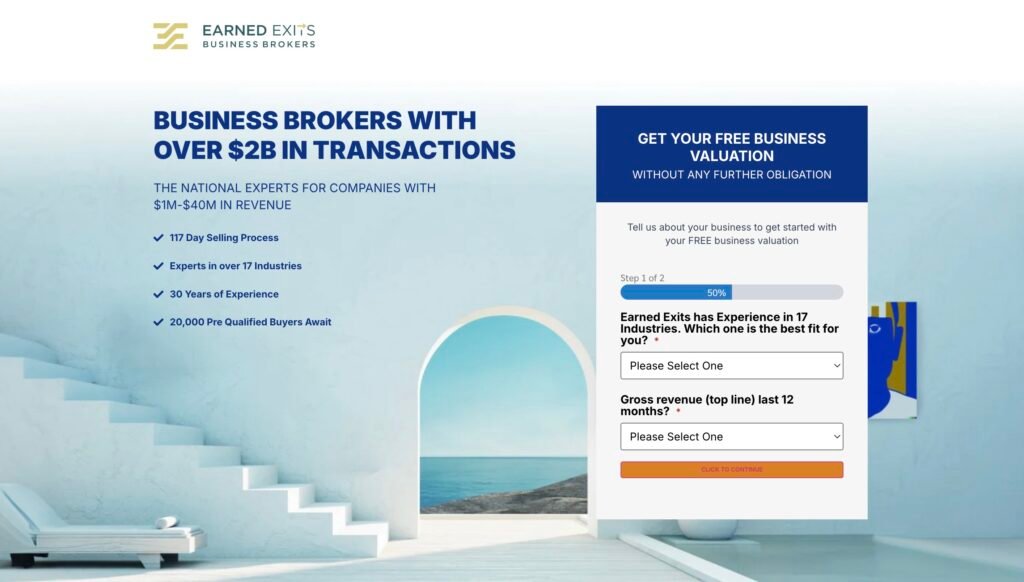

Named a top broker in 2025, Earned Exits is a specialized mid-market business broker ($1M–$40M revenue) that helps owners sell while protecting their legacy and taking care of employees.

- Earned Exits specializes in business exits that preserve company legacy and employee interests, not just maximizing sale price

- The firm employs a unique 10-step selling process that incorporates legacy protection documentation and employee retention planning

- Businesses with protected employee interests typically command 15-20% higher valuations than those focused solely on financial metrics

- Earned Exits has a proven track record of successful transitions with over 200 businesses maintaining workforce stability post-acquisition

- Their comprehensive approach includes post-sale transition support for up to 12 months, ensuring continuity beyond the transaction.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to receive a free business valuation by completing their short form. Begin the process of leveraging an experienced broker who has completed over a $2 billion in transactions across 17+ industries.

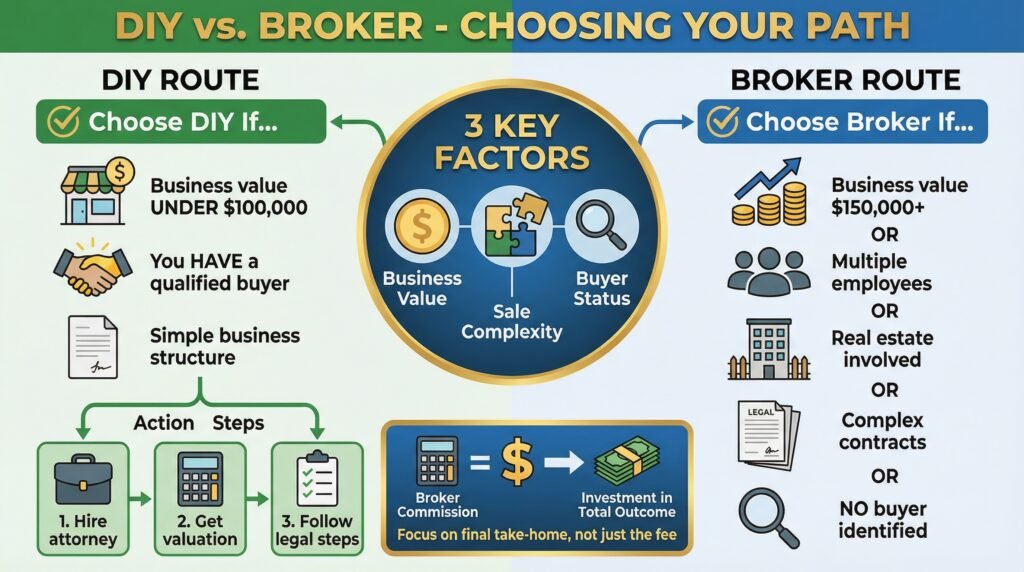

DIY vs. Broker: Which Option Fits Your Situation

The right choice comes down to three factors: your business’s value, the complexity of the sale, and whether you already have a qualified buyer. If your business is worth under $100,000 and you have a known buyer, DIY is a legitimate path: hire an attorney, get a valuation, and follow the steps outlined above.

If your business is worth $150,000 or more, involves multiple employees, real estate, or complex contracts, or you have no buyer identified, the evidence strongly favors working with a broker. The commission is not a cost to avoid; it’s a variable in an equation where the total outcome, not just the fee, is what determines how much you actually walk away with.

Business Seller Sanity Check

Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and check if you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the button below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

In part 3 of this series, we will discuss how to choose the right business broker and which option fits your specific situation: DIY vs broker. Follow our blog to remain updated on new articles and strategies in this ever-evolving market.

If you have read enough and know your business has passed the preparation criteria to go to market, read our review of Earned Exits here.

Earned Exits has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes outcomes for business owners. Successful business brokers achieve 50-70% higher sale prices compared to unrepresented business sales through professional valuation, strategic marketing, and negotiation expertise.

If you have decided that Earned Exits is a good fit and your business size is $1M-$40M+, click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Frequently Asked Questions

These are the questions business owners ask most often when deciding how to approach their sale. The answers here are based on how deals actually work in practice, not how they’re described in marketing materials or best-case scenarios.

Whether you’re six months away from listing or just beginning to think about an exit, understanding these fundamentals now gives you a meaningful advantage when it matters most.

Is it worth paying a broker commission on a small business sale?

It depends heavily on whether you already have a buyer and how complex the transaction is. For businesses under $100,000 with a known buyer in hand, paying a 10% commission is difficult to justify; the math simply doesn’t work in your favor, and the transaction is manageable enough that an attorney and accountant can guide you through it without a broker in the middle.

For businesses in the $150,000 to $500,000 range without a buyer identified, the calculation is different. A broker who helps you achieve even a 10% to 15% higher sale price through accurate valuation, active buyer sourcing, and skilled negotiation has more than covered their commission. The question to ask isn’t “Can I afford a broker?” but rather “What is the most likely outcome with and without one, and what is the difference in net proceeds?”

For businesses above $500,000, using a broker is almost always the financially superior choice. The complexity of these transactions, deal structure, buyer financing, due diligence management, legal coordination, requires professional guidance that directly protects your final number and your post-closing liability exposure.

Commission vs. Value: A Quick Comparison by Business Size

Under $100,000: Broker minimum fees often represent 12%+ of proceeds. DIY with attorney support is usually the better path if a buyer exists.

$100,000 – $300,000: Standard 10% commission is significant but often offset by better pricing, faster sale, and stronger deal terms. Evaluate on a case-by-case basis.

$300,000 – $1,000,000: Broker expertise in this range consistently produces higher net proceeds after commission than most independent sales achieve at full price.

Above $1,000,000: An M&A advisor or experienced mid-market broker is strongly recommended. Deal complexity and buyer sophistication at this level require professional representation.

What happens if a broker refuses to take on my business?

If a broker declines to represent your business, it’s important to understand why before deciding on your next move. The most common reasons are low profitability (not enough commission potential), heavy owner-dependence that makes the business difficult to sell, messy or unverifiable financials, or a distressed operational situation that reduces buyer appeal.

In most cases, the broker’s refusal is a signal worth taking seriously; if experienced professionals don’t see a clear path to closing your sale, that’s meaningful market feedback. The right response is to address the underlying issue: clean up your books, reduce owner dependence, or work with a business consultant to improve the business’s sellability before attempting to list again.

How do I know if my business is priced correctly?

A correctly priced business generates serious buyer inquiries within the first 30 to 60 days of listing. If you’ve been on the market for 90 days or more with no credible offers, not just inquiries, but actual qualified interest, your price is almost certainly too high. Silence from the market is the clearest signal available that buyers are comparing your listing to alternatives and choosing differently.

The most reliable way to validate your price before listing is a professional business appraisal or a detailed broker opinion of value based on actual comparable sales data. This gives you an objective anchor point that is defensible in negotiations and not subject to your own optimism about what the business should be worth. Paying for this step upfront is far less expensive than the cost of carrying an overpriced listing for six to twelve months while your best buyers move on.

If you’re already listed and questioning your price, look at three things: the number of inquiries relative to your listing views, how far into conversations buyers get before disengaging, and whether the feedback you’re hearing from interested parties consistently mentions price as a concern. If buyers say your price is the issue, believe them; adjusting early is always better than waiting until the listing has gone stale and your negotiating position has weakened significantly.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.