Quick Summary

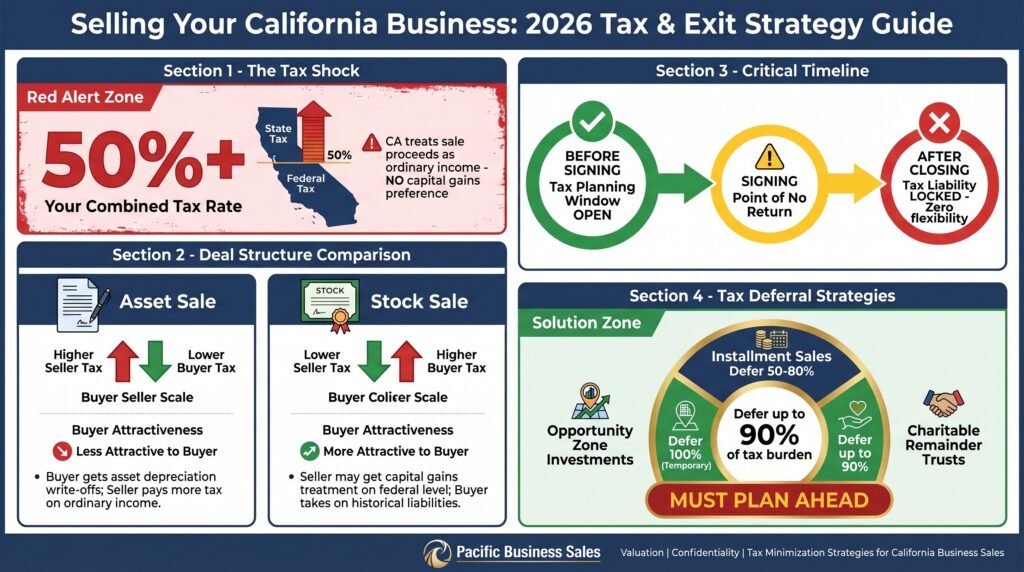

- California has no capital gains tax preference, your business sale proceeds are taxed as ordinary income at the state level, which can push your combined federal and state tax rate past 50%.

- Whether your deal is structured as an asset sale or a stock sale changes everything, from how much you pay in taxes to how attractive the deal looks to buyers.

- Tax planning must happen before you sign anything, once the transaction closes, your tax liability is locked in with zero room to maneuver.

- Pacific Business Sales works with California business owners to build exit strategies that address valuation, confidentiality, and tax minimization before going to market.

- There are legal strategies, including installment sales, opportunity zone investments, and charitable remainder trusts, that can defer up to 90% of your tax burden, but only if you plan ahead.

California Business Sales in 2026: What You Need to Know First

Selling a business in California is one of the most financially significant decisions you will ever make, and one of the most complicated.

California’s regulatory environment, its aggressive tax treatment of business sale proceeds, and the complexity of deal structuring make this a process where preparation is not optional. Sellers who go to market without a clear exit strategy routinely leave hundreds of thousands of dollars on the table. Those who plan correctly can minimize taxes, protect confidentiality, attract stronger buyers, and close faster.

This guide walks you through everything that matters in 2026: transaction types, tax implications, timing strategy, valuation, and the step-by-step process to execute a successful exit.

Why California Is One of the Hardest States to Sell a Business In

California does not offer preferential capital gains tax rates. While the federal government taxes long-term capital gains at 0%, 15%, or 20% depending on your income, California taxes those same gains as ordinary income, up to 13.3%. Stack that on top of federal rates and the net investment income tax, and your effective rate on a business sale can exceed 50% for high-value transactions. That is not a reason to avoid selling. It is a reason to build a tax strategy before you do.

The Two Transaction Types That Determine Everything

Every business sale in California falls into one of two structures: an asset sale or a stock sale. These are not minor technical distinctions. The structure you agree to will determine your tax rate, your liability exposure, and how attractive the deal is to the buyer sitting across the table. Most sellers assume one structure is automatically better. The reality is more nuanced, and getting it wrong is expensive.

Why Tax Planning Must Start Before You Sign Anything

This is the single most important thing to understand before entering the market: tax planning for a California business sale must be done in advance. Once escrow closes, the transaction is set in stone. There is no restructuring after the fact, no going back to allocate proceeds differently, and no opportunity to implement deferral strategies retroactively.

Sellers who engage a qualified tax advisor before listing, not during due diligence, not after signing a letter of intent, are the ones who walk away with significantly more after-tax proceeds. The strategies covered later in this article are only available if you act early.

Every experienced buyer also comes prepared with their own tax strategy. You should too.

Why Business Brokers are a Must

Experienced business brokers can assist greatly in the tax preparation process. Earned Exits’ team includes transaction tax specialists who identify optimal deal structures based on your specific circumstances. Their analysis considers federal and state tax implications, potential capital gains treatments, and installment sale advantages that might reduce your effective tax rate.

The firm frequently recommends consulting arrangements, deferred compensation structures, and earn-out provisions that can convert ordinary income into capital gains or spread tax liability across multiple years.

These approaches not only increase after-tax proceeds but also often align seller and buyer interests by creating mutual incentives for post-sale business success. Their expertise in these complex tax considerations frequently delivers six-figure tax savings that might otherwise be overlooked in transactions focused solely on gross purchase price. Read our full review of the Earned Exit business brokers here.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

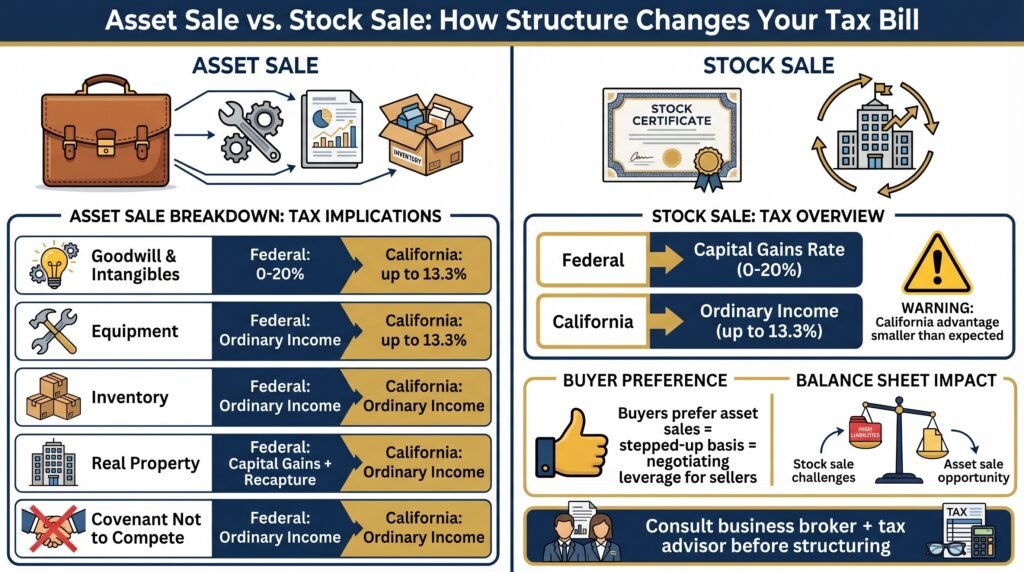

Asset Sales vs. Stock Sales: How the Structure Changes Your Tax Bill

The structure of your deal is not just an accounting formality, it is the foundation of your tax outcome and your negotiating position. Buyers and sellers often want different structures for opposite financial reasons, which means understanding both sides is essential before you sit down at the table.

How Asset Sales Are Taxed in California

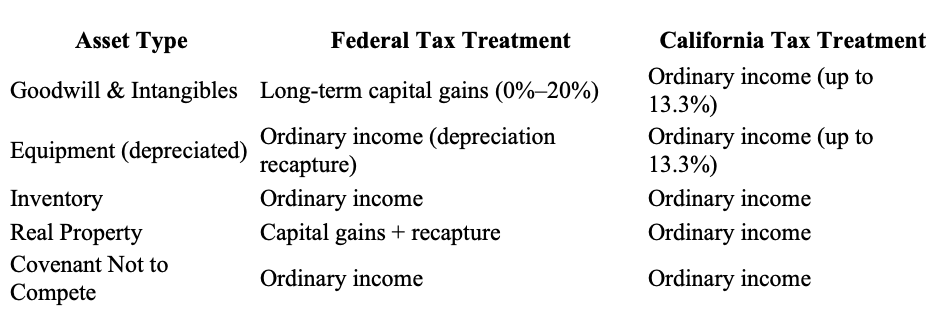

In an asset sale, the buyer purchases individual assets of the business, equipment, inventory, customer lists, intellectual property, goodwill, rather than the legal entity itself. For the seller, this creates a mixed tax outcome depending on how the purchase price is allocated across those assets.

Different assets are taxed at different rates. Equipment and fixtures that have been depreciated may trigger depreciation recapture, which is taxed as ordinary income at both the federal and California state level. Goodwill and other intangible assets are typically taxed at capital gains rates federally, but California still taxes them as ordinary income. The allocation of purchase price across asset categories, documented in IRS Form 8594, directly determines your tax bill, which is why negotiating the allocation is as important as negotiating the sale price.

The allocation negotiation is a leverage point many sellers overlook. Shifting more of the purchase price toward goodwill and intangibles can reduce your federal tax exposure meaningfully, even if California taxes both at ordinary income rates.

How Stock Sales Are Taxed in California

In a stock sale, the buyer purchases your ownership interest in the legal entity, your shares in a corporation or membership interest in an LLC. For the seller, the entire gain is typically treated as a capital gain at the federal level. However, California taxes that gain as ordinary income regardless. One common assumption sellers make is that a stock sale automatically means lower taxes. Federally, that can be true. In California, the advantage is much smaller than most sellers expect.

Which Structure Buyers Prefer and Why It Matters to You

Most buyers strongly prefer asset sales because they get a stepped-up tax basis on the assets they acquire, which allows them to depreciate those assets again from the purchase price. This reduces their future tax burden significantly. In a stock sale, the buyer inherits your original cost basis, and your depreciation history, which is financially less attractive to them. Knowing this gives you negotiating leverage: if a buyer wants an asset sale structure, you may be able to use that preference to negotiate a higher total purchase price to offset the tax difference on your side.

How the Balance Sheet Affects Which Structure Makes Sense

Your company’s balance sheet plays a direct role in which structure makes financial sense. If your business carries significant liabilities: loans, contingent legal claims, unpaid payroll taxes, a stock sale transfers those liabilities to the buyer, which they will either price into the deal or walk away from. If your business is clean with minimal liabilities and high intangible value like brand or customer relationships, an asset sale may actually produce a cleaner transaction at a better price.

This is precisely why engaging a business broker and tax advisor before structuring the deal is not a luxury, it is the difference between a good exit and an expensive one.

Federal vs. California State Taxes on a Business Sale

Understanding the two layers of taxation on your California business sale, federal and state, is essential before you can build any effective strategy around them.

Federal Capital Gains Tax Rates for Business Sales

At the federal level, the tax rate on your business sale depends primarily on how long you have held the asset and how the proceeds are classified. Long-term capital gains, from assets held more than one year, are taxed at 0%, 15%, or 20% depending on your taxable income. For most business owners selling a company of meaningful value, the 20% rate applies.

On top of that, high-income sellers may also owe the Net Investment Income Tax (NIIT), which adds an additional 3.8% on investment income above certain thresholds, $200,000 for single filers and $250,000 for married filing jointly. That brings the federal rate on capital gains to 23.8% for many business owners.

Portions of the sale allocated to ordinary income, depreciation recapture, inventory, non-compete agreements, are taxed at federal ordinary income rates, which can reach 37% for top earners. The blended rate on your total proceeds depends entirely on how the purchase price is allocated across asset categories.

California’s Additional State Tax Burden

California taxes all capital gains as ordinary income. There is no preferential rate for long-term holdings, no exclusion, and no discount. The state’s top marginal income tax rate is 13.3%, which applies to income over $1 million. For most business owners completing a significant exit, this rate will apply to the bulk of their proceeds.

Combined with federal taxes and the NIIT, a California business owner selling a mid-market company could face an effective combined rate of 50% or more on a meaningful portion of their gain. This is not hypothetical, it is the actual tax reality for sellers who do not plan ahead.

Why California Treats Some Tax Strategies Differently Than the IRS

Several tax strategies that work at the federal level either do not apply in California or are treated differently by the Franchise Tax Board (FTB). For example, California does not conform to federal Opportunity Zone tax incentives in the same way, meaning a strategy that defers federal taxes may still result in full California taxation in the year of sale. This is why your tax advisor must be familiar specifically with California business sale tax law, not just federal tax strategy. A generalist CPA without California-specific M&A experience can give you advice that is technically correct federally but financially damaging at the state level.

Legal Ways to Reduce Your Tax Bill Before Closing

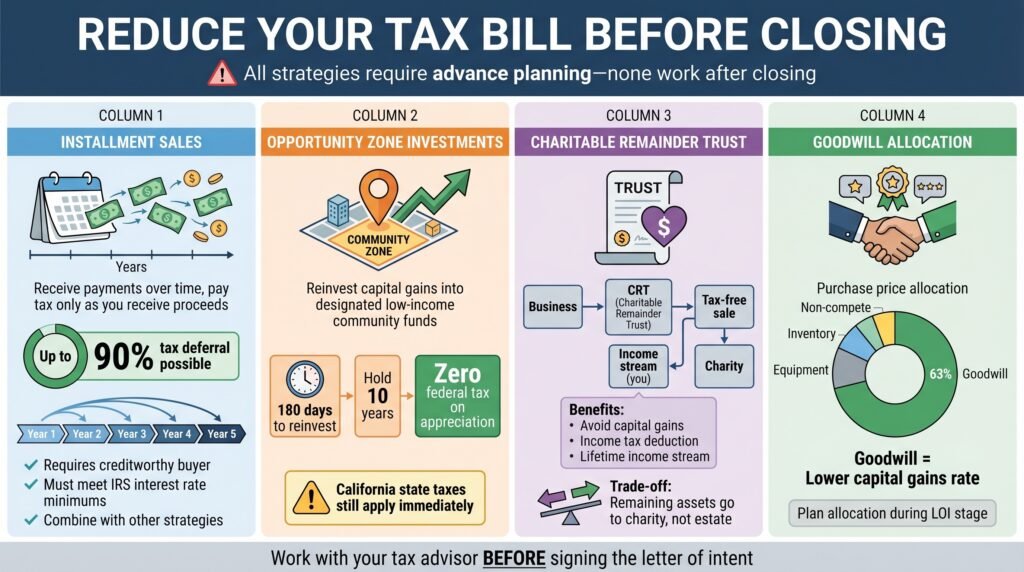

There are legitimate, IRS-recognized strategies that California business owners can use to reduce or defer taxes on a business sale, but every single one of them requires advance planning. None can be implemented after closing.

Installment Sales: Spread the Tax Burden Over Time

An installment sale is one of the most practical and widely used tax deferral tools available to California business sellers. Instead of receiving the full purchase price at closing, you agree to receive payments over a period of years, and you only pay tax on the proceeds as you receive them. This spreads your tax liability across multiple tax years, which can keep you out of the highest marginal brackets in any single year and meaningfully reduce your total tax burden over time.

The mechanics are straightforward: you and the buyer agree on a payment schedule, a promissory note is executed, and you report income on IRS Form 6252 each year as payments are received. Interest is charged on the deferred balance, which is also taxable, but the overall benefit can be substantial for sellers who do not need all proceeds immediately.

In some cases, sellers have been able to defer up to 90% of the taxes on a business sale using installment arrangements combined with other strategies. The key is structuring the note correctly and ensuring your tax advisor reviews the terms before you sign the letter of intent.

- Installment sales work best when the buyer is financially stable and creditworthy, you are effectively becoming their lender

- The interest rate on the promissory note must meet IRS minimum requirements to avoid imputed interest rules

- California taxes each installment payment as ordinary income in the year received

- A security agreement or personal guarantee should be negotiated to protect your position as the note holder

- Installment sales can be combined with other deferral strategies for compounded tax savings

Opportunity Zone Investments as a Deferral Strategy

Qualified Opportunity Zone (QOZ) investments allow you to reinvest capital gains from a business sale into a designated low-income community fund and defer, and in some cases, reduce, your federal tax liability on those gains. The program was created under the 2017 Tax Cuts and Jobs Act and remains active in 2026.

- Gains reinvested within 180 days of the sale are eligible for federal deferral

- Holding the Opportunity Zone investment for at least 10 years eliminates federal capital gains tax on the appreciation of the new investment

- California does not conform to federal QOZ tax treatment, state taxes on the original gain are still owed in the year of sale

- The fund must be a certified Qualified Opportunity Fund investing in eligible QOZ property

This strategy is most powerful for sellers with large gains who have a long investment horizon and are comfortable with the risks of the underlying QOZ investment. It is not a fit for every seller, but for those with the right profile, the long-term federal tax elimination on the new investment is a compelling benefit.

Given that California does not conform, your advisor needs to model both the federal deferral benefit and the California tax cost in the year of sale before recommending this approach. The numbers still work favorably in many cases, but only when the full picture is analyzed.

Charitable Remainder Trusts for High-Value Business Sales

A Charitable Remainder Trust (CRT) is a powerful strategy for business owners selling companies with significant appreciated value. Before the sale closes, you transfer ownership of the business, or a portion of it, into the CRT. The trust then sells the business tax-free, reinvests the proceeds, and pays you an income stream for life or a set term. At the end of the trust period, the remaining assets pass to your designated charity.

The immediate benefits include avoiding capital gains tax at the time of sale, receiving a partial charitable income tax deduction, and generating a reliable income stream. The tradeoff is that the remaining principal eventually goes to charity rather than your estate. For business owners with philanthropic goals or estate planning needs, the CRT can accomplish multiple objectives simultaneously.

The Role of Goodwill in Reducing Your Tax Exposure

Goodwill, the value of your brand, customer relationships, reputation, and workforce, is typically the largest single asset in a service or relationship-driven business. Federally, gains allocated to goodwill are taxed at the lower long-term capital gains rate, making it one of the most tax-efficient components of your purchase price allocation.

Structuring the deal to maximize the portion of the purchase price allocated to goodwill, versus equipment, inventory, or non-compete agreements, can significantly improve your after-tax outcome at the federal level. Your tax advisor and business broker should work together on the allocation strategy during the letter of intent stage, not after the purchase agreement is drafted.

Business Seller Check-In

Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If you have read enough and know your business has passed the preparation criteria to go to market, read our review of Earned Exits here.

If you have decided that Earned Exits is a good fit and your business size is $1M-$40M+, click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

In part 2 of this series, we will discuss timing your business exit for maximum value, how to value your business before going to market, and more. Be sure to follow this blog to stay up-to-date on future content for selling your business.

Frequently Asked Questions

The questions below address the most common concerns California business owners raise when considering a sale. The answers are direct and based on how these transactions actually work in practice.

How long does it take to sell a business in California?

The average California business sale takes between six and nine months from listing to closing. Businesses with clean financials, organized documentation, and realistic pricing tend to close faster, sometimes in four to five months. Complex transactions, those involving real estate, or deals requiring SBA financing can extend to twelve months or longer. Preparation before listing is the single biggest factor in compressing that timeline.

What taxes do I pay when I sell my business in California?

You will owe both federal and California state taxes on the gain from your business sale. Federally, long-term capital gains are taxed at 0%, 15%, or 20% depending on your income, with an additional 3.8% Net Investment Income Tax for high earners. California taxes all capital gains as ordinary income at rates up to 13.3%. Portions of the sale allocated to depreciation recapture, inventory, or non-compete agreements are taxed at ordinary income rates federally as well. Your combined effective rate on a significant exit can exceed 50%, which is why advance tax planning is essential.

Is California a good state to sell a business in 2026?

From a buyer demand perspective, yes. California, particularly Southern California, has one of the deepest and most active buyer pools in the country. Private equity groups, strategic acquirers, and individual buyers with SBA pre-approval are actively searching for acquisitions across most industries. The buyer market is strong.

From a tax perspective, California is one of the most challenging states in which to exit. The absence of preferential capital gains treatment and the state’s top 13.3% income tax rate mean sellers face a significant tax burden without proper planning.

The right answer is that California is an excellent place to sell a business, if you plan your exit correctly. The tax burden is manageable with the right strategies in place, and the buyer demand means well-prepared businesses attract competitive offers. The sellers who struggle are the ones who approach the California market without a strategy.

- Strong buyer demand across most California industries in 2026

- Active SBA financing market supporting mid-market transactions

- High state income tax requires advance planning to protect after-tax proceeds

- Regulatory complexity, WARN Act, PAGA, employee classification, adds due diligence friction

- Southern California markets including Los Angeles, Orange County, and San Diego showing particularly strong buyer activity

What is the difference between an asset sale and a stock sale in California?

In an asset sale, the buyer purchases the individual assets of the business, equipment, goodwill, customer lists, intellectual property, rather than the legal entity itself. In a stock sale, the buyer acquires your ownership interest in the entity directly. Buyers generally prefer asset sales because they receive a stepped-up tax basis on the acquired assets. Sellers often prefer stock sales for cleaner liability transfer. In California, both structures result in state income tax at ordinary rates, the federal tax advantage of a stock sale is smaller than most sellers expect once California’s treatment is factored in.

Can I reduce capital gains tax when selling my California business?

Yes, but only through strategies implemented before closing. Installment sales allow you to spread tax liability across multiple years. Qualified Opportunity Zone investments defer federal gains, though California taxes still apply in the year of sale. Charitable Remainder Trusts allow high-value business interests to be transferred into a trust that sells tax-free and pays you an income stream. Strategic purchase price allocation, maximizing the portion assigned to goodwill, reduces your federal tax rate on that portion of the gain. In some cases, combinations of these strategies can defer up to 90% of the tax burden. None of these options are available after closing.

References

[1] Nongrantor trust strategies and California sourcing rules

[2] Charitable Remainder Trust and ESOP tax treatment

[5] Installment sales and QSBS provisions under IRC

[6] California residency audit practices and wealth migration patterns

[9] Entity restructuring timelines and planning requirements

[13] Section 1202 QSBS qualification rules

[15] ESOP establishment and deferral mechanics

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.