Key Takeaways

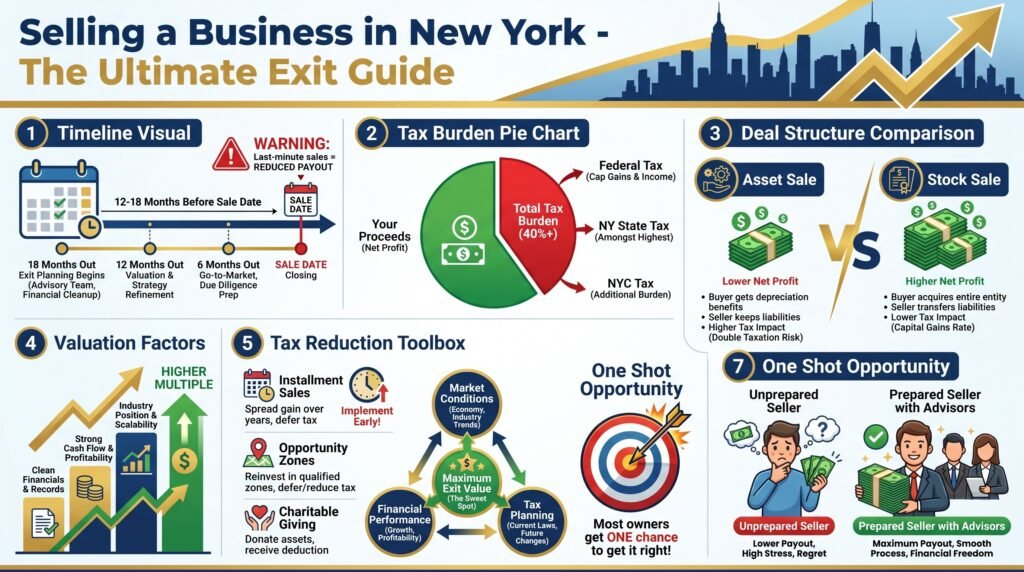

- Start exit planning 12–18 months in advance

New York’s complex tax and legal environment means last-minute sales often reduce your final payout. - Expect a total tax burden of 40%+

Combined federal, New York State, and New York City taxes can take a significant share of your proceeds without proper planning. - Deal structure directly impacts your net profit

Choosing between an asset sale vs. stock sale can dramatically change how much you keep after taxes. - Your valuation depends on preparation

Business value in New York is heavily influenced by industry, cash flow, and clean financials—well-prepared sellers consistently earn higher multiples. - Advanced tax strategies can reduce your liability

Tools like installment sales, Opportunity Zone investments, and charitable giving strategies can lower taxes—but only if implemented early. - Timing is everything in a New York business sale

Market conditions, financial performance, and tax planning all play a role in maximizing your exit outcome. - Most owners only get one chance to sell

Selling your business is likely the most important financial event of your life—early decisions determine how much value you actually keep. - Planning ahead consistently leads to better outcomes

Business owners who start early and work with experienced advisors typically walk away with significantly more than those who wait.

In part 1 of this New York Business Sale Guide, I discussed building an exit strategy, best time to sell your New York business, New York business valuations, and more.

In part 2, we will discuss, New York’s tax burden on business sales, tax strategies that reduce what you owe after the sale, and more. Follow this blog for the most up-to-date articles on business selling and profitable exits.

New York’s Tax Burden on Business Sales Is Significant

If there is one area where New York business sellers are consistently caught off guard, it is taxes. The state and city layers stacked on top of federal obligations create a combined tax burden that is among the highest in the country, and without proactive planning, that burden can consume more than 40 cents of every dollar you receive at closing.

Understanding your tax exposure is not just an accounting exercise. It directly determines your negotiation strategy, your deal structure preferences, and how much pre-sale planning time you actually need. Many sellers focus intensely on gross sale price while underestimating how dramatically taxes will affect their net proceeds. The difference between a well-planned exit and an unplanned one can easily represent seven figures on a mid-market transaction.

New York’s tax environment also affects how you should think about deal timing. Because the state aggressively audits high-value transactions, particularly those involving recent or departing New York residents, decisions around residency, deal closing dates, and asset allocation in the purchase agreement all carry meaningful tax implications that require experienced legal and accounting guidance well in advance of closing.

Federal Capital Gains Tax Rates for Business Sellers

At the federal level, business sale proceeds are typically subject to long-term capital gains tax rates if you have held the business or its assets for more than one year. Long-term capital gains rates are currently 0 percent, 15 percent, or 20 percent depending on your taxable income, with the 20 percent rate applying to high earners, which most New York business sellers are by the time of a significant liquidity event.

However, not all of your sale proceeds will be taxed at the favorable capital gains rate. Depreciation recapture, particularly on equipment, real estate improvements, and other depreciable assets, is taxed as ordinary income at rates up to 37 percent federally. The allocation of purchase price between asset categories in your deal documents directly affects how much of your proceeds fall into each tax bucket, which is why purchase price allocation negotiation is a critical component of any well-structured New York business sale.

New York State and City Income Tax on Sale Proceeds

New York State taxes business sale proceeds as ordinary income for most sellers, with the top marginal state rate reaching 10.9 percent for individuals with income exceeding $25 million, and 9.65 percent for income between $2.155 million and $25 million. New York City adds its own layer, the city personal income tax tops out at 3.876 percent for high earners. These rates apply on top of federal obligations, with very limited deductions available to offset them at the state and city level.

How Combined Tax Rates Can Exceed 40 Percent on a Sale

For a high-earning New York City business owner selling a business with significant capital gains, the math is sobering. Federal long-term capital gains at 20 percent, the 3.8 percent Net Investment Income Tax (NIIT) for high earners, New York State income tax at approximately 9.65 percent, and New York City income tax at 3.876 percent combine to a total marginal rate that can approach or exceed 37 percent on capital gains, and substantially more on any proceeds taxed as ordinary income. On a $5 million transaction, that tax exposure can easily reach $1.5 million to $2 million or more depending on the deal structure and asset composition.

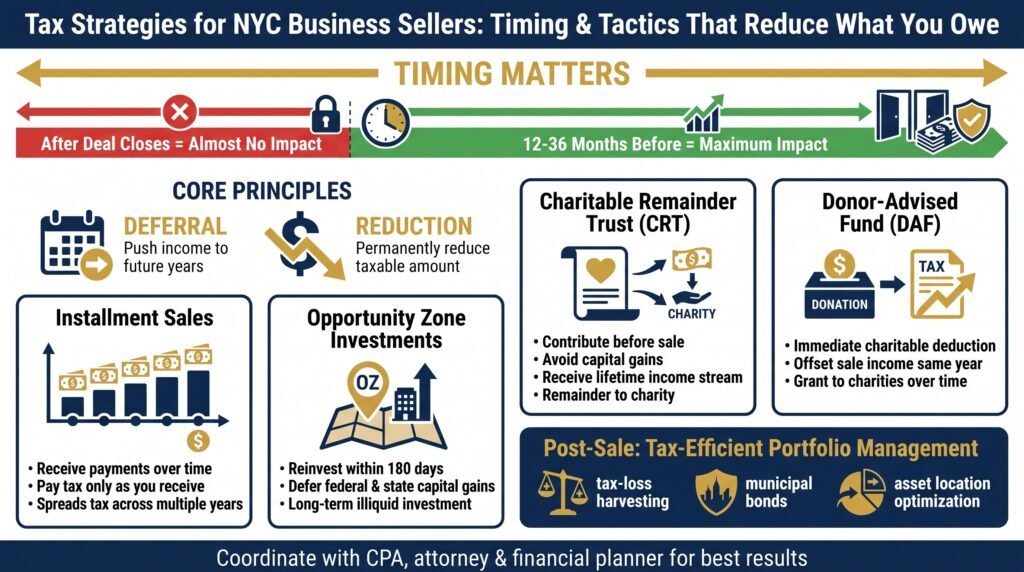

Tax Strategies That Reduce What You Owe After the Sale

The good news is that New York business sellers have access to several powerful legal strategies to reduce their tax exposure, but almost all of them require advance planning. Strategies implemented after a deal closes have almost no impact. Strategies implemented 12 to 36 months before closing can make an enormous difference.

The core principle behind most tax reduction strategies for business sellers is either deferral (pushing taxable income into future years when rates may be lower or your other income is reduced) or reduction (permanently reducing the taxable amount through charitable vehicles, basis adjustments, or favorable deal structuring). A combination of both approaches, coordinated across your CPA, attorney, and financial planner, produces the best outcomes.

Not every strategy is appropriate for every seller. Your entity type, the size of your transaction, your post-sale income plans, and your philanthropic intentions all shape which tools make sense for your situation. What follows are the most impactful strategies currently available to New York City business sellers in 2026.

How Installment Sales Spread Your Tax Liability Over Time

An installment sale is one of the most accessible and effective tax deferral tools available to business sellers. Rather than receiving the full purchase price at closing, you receive payments over multiple years, and you pay tax only as you receive each payment. This spreads your taxable income across several tax years, which can keep you out of the highest marginal rate brackets and reduce your overall tax liability meaningfully.

For a New York City seller, this strategy is particularly valuable because it also spreads your New York State and City income tax exposure over multiple years rather than creating a single massive tax event. There are trade-offs: you carry credit risk on the buyer’s ability to pay, and interest income on the deferred balance is taxable as ordinary income. Proper legal documentation of the installment note, including security interests and default provisions, is essential to protect your position as a seller-creditor.

Opportunity Zone Investments to Defer Capital Gains

Qualified Opportunity Zone (QOZ) investments allow business sellers to defer capital gains by reinvesting proceeds into designated Opportunity Zone funds within 180 days of the sale. While the program has evolved since its introduction, it still provides meaningful deferral of federal capital gains tax.

New York State generally conforms to the federal Opportunity Zone rules, offering additional state-level deferral for eligible investments. Sellers with significant capital gains and a tolerance for illiquid, longer-term investments in real estate or operating businesses in designated zones should evaluate this strategy with their tax advisor well before their anticipated sale date.

Charitable Giving Strategies That Create Immediate Tax Deductions

For sellers with philanthropic intentions, charitable vehicles offer a powerful combination of tax reduction and legacy planning. A Charitable Remainder Trust (CRT) allows you to contribute appreciated business interests, before the sale, to an irrevocable trust, which then sells the business tax-free and pays you an income stream for a set period or lifetime.

You receive an immediate partial charitable deduction, avoid capital gains on the contributed assets, and ultimately leave the remainder to your chosen charity. For more information on exit strategies, see our business exit planning guide..

A Donor-Advised Fund (DAF) is a simpler alternative, you contribute cash or appreciated assets to the fund, receive an immediate charitable deduction, and then recommend grants to charities over time at your own pace. For New York sellers facing a large, concentrated taxable event, combining a DAF contribution with a business sale in the same tax year can substantially offset the income generated by the transaction. Both strategies require careful coordination with your legal and tax team and should be structured before the business sale closes.

Managing Your Investment Portfolio Tax-Efficiently Post-Sale

After the sale closes, your primary financial challenge shifts from building business value to preserving and growing liquid wealth, a very different skill set. New York business sellers who receive significant cash proceeds at closing should work with a financial advisor experienced in post-liquidity event planning to implement a tax-efficient investment strategy.

This includes tax-loss harvesting, asset location optimization across taxable and tax-deferred accounts, and municipal bond allocations that generate income exempt from New York State and City taxes, a particularly valuable tool given New York’s high-income tax rates.

Business Seller Sanity Checklist

As we covered in the first part of this series, it’s time for another seller sanity check. Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If you have read enough and know your business has passed the preparation criteria to go to market, read our review of Earned Exits here.

The classic adage applies, “If you want to go fast, go alone, If you want to go far, go together” If your business is valued at $1 to $40 million, an experienced business broker like Earned Exits will leverage more potential buyers and an average increase of profit of 20 to 30% more than going it alone. Stated simply, alone is cheaper, but not always most profitable.

If you have decided that Earned Exits is a good fit , Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Frequently Asked Questions

Below are the questions New York business owners most commonly ask when they begin thinking seriously about a sale.

How Is a New York Business Valued Before a Sale?

Most New York businesses are valued using the EBITDA multiple method, your earnings before interest, taxes, depreciation, and amortization are multiplied by an industry-specific figure that reflects what buyers are currently paying for comparable businesses. For Main Street businesses, multiples typically range from 2.5x to 6x EBITDA. Lower-middle-market companies with strong recurring revenue and scalable operations can achieve 8x to 12x or higher. Your specific multiple is influenced by factors including revenue trend, customer concentration, owner dependency, management team strength, industry dynamics, and the quality of your financial documentation.

What Is the Difference Between an Asset Sale and a Stock Sale in New York?

An asset sale is a transaction in which the buyer purchases specific assets and liabilities of your business, equipment, contracts, intellectual property, customer lists, and goodwill, rather than the company entity itself. A stock sale transfers ownership of the actual business entity, and the buyer inherits everything the company owns and owes, including contingent liabilities. Buyers generally prefer asset sales because they provide more protection from unknown liabilities and allow for a step-up in asset basis for depreciation purposes. Sellers often prefer stock sales because proceeds are typically taxed at capital gains rates rather than the mixed ordinary income and capital gains treatment common in asset sales. The right structure for your transaction depends on your entity type, negotiating position, and tax situation, and should be determined in consultation with your M&A attorney and CPA well before the deal begins.

Do I Need a Business Broker to Sell My Business in New York City?

You are not legally required to use a business broker to sell your New York City business, but the data and practical experience of thousands of transactions make a compelling case for working with one. Business brokers bring a pre-qualified buyer network, transaction management expertise, negotiating experience, and market intelligence that most business owners, regardless of how capable they are in their own industry, cannot replicate without years of deal experience.

Sellers who attempt to sell without a broker, a process called selling “For Sale by Owner” or FSBO, frequently encounter the same challenges: difficulty maintaining confidentiality during the marketing process, inability to generate competitive tension between multiple buyers, and vulnerability to experienced buyers who recognize an unrepresented seller and negotiate accordingly. The broker’s success fee, which typically ranges from 3 to 12 percent depending on deal size, is almost always recovered through a higher final sale price that a qualified broker’s process generates.

In New York City specifically, where buyers are sophisticated and the competitive landscape for quality businesses is intense, having a broker who knows the local market, maintains active buyer relationships, and has recent closed transaction experience in your industry is a meaningful advantage. The broker does not replace your attorney or CPA, they work alongside them as the deal manager who keeps the process moving from first contact with a buyer to the moment you sign at the closing table.

If you are ready to explore what your New York business is worth and what a strategic exit could look like for your specific situation, Earned Exits can guide New York City business owners through every stage of the sale process, from initial valuation to closing day.

When planning a business sale in New York, understanding the tax implications is crucial. Timing your exit strategy can significantly affect the taxes you owe.

For more detailed guidance, you might consider consulting resources and business brokers like Earned Exits to better navigate these complexities for businesses valued between $1 – $40 million.

References

- BNY Mellon Wealth Management, “Reducing the Tax Impact on the Sale of Your Business”

- SmartAsset, “How to Avoid Capital Gains Tax on a Business Sale”

- Brighton Jones, “Exit Planning Tax Strategies: Maximizing Your Business Sale”

- Richard Brothers Financial Advisors, “Tax Strategies After Business Sale for Maximizing Profits”

- Cummings & Co. Planning, “3 Ways To Reduce The Taxes You Pay When Selling Your Business to a Third Party”

- U.S. Small Business Administration, “7 Tax Strategies to Consider When Selling a Business”

- RBC Wealth Management, “Minimize tax and maximize your business sale”

- EP Wealth Advisors, “How to Manage Taxes When Selling a High-Value Business”

- U.S. Bank, “Tax Implications of Selling a Business”

- Exit Planning Institute, “Certified Exit Planning Advisor Resources”

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.