Quick Summary

Illinois business owners can significantly reduce their tax bill when selling by choosing the right deal structure before signing. Key strategies include installment sales (to spread tax across years), negotiating a stock sale over an asset sale, and allocating the purchase price strategically across asset classes.

Owners with qualifying C-corp stock may eliminate gains entirely through QSBS exclusion (Section 1202), while ESOPs and Charitable Remainder Trusts offer deferral options for the right situations. If you’re relocating out of Illinois post-sale, the timing of your move relative to closing and payment dates matters, Illinois taxes residents on all income and has complex sourcing rules for nonresidents. Finally, don’t skip dissolution and compliance filings, as incomplete shutdown steps can create tax headaches long after you’ve left the state

Table of Contents

- Quick Summary

- Smart planning before you sign can save you more than negotiating the price.

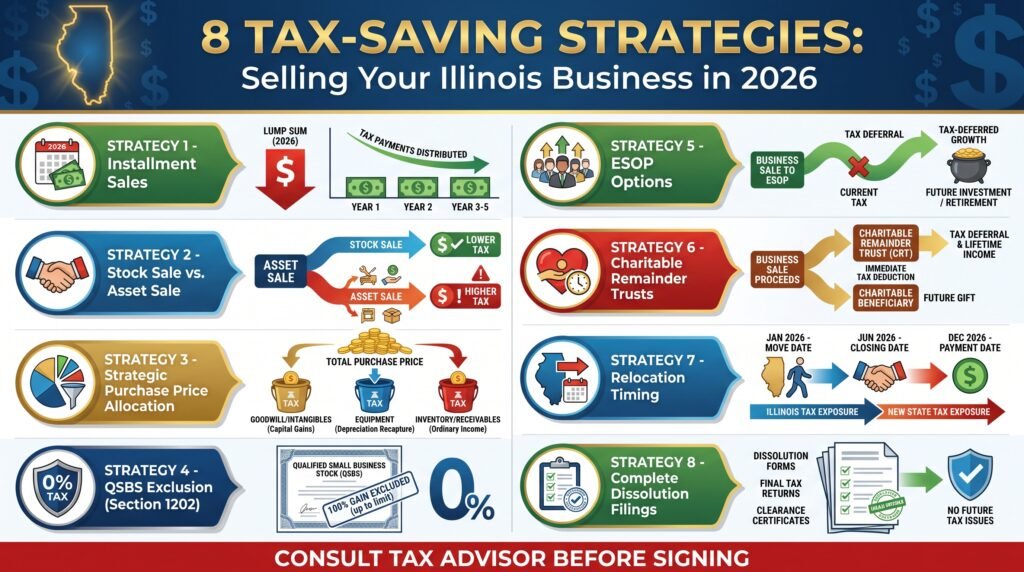

- 1. Structure the sale as an installment agreement

- 2. Negotiate a stock sale instead of an asset sale when possible

- 3. Allocate the purchase price strategically across asset classes

- 4. Use Qualified Small Business Stock exclusion if you qualify

- 5. Sell to an ESOP to defer or eliminate capital gains

- 6. Use a Charitable Remainder Trust for partial tax deferral

- 7. Time your relocation carefully if you’re leaving Illinois

- 8. Handle Illinois dissolution and compliance steps before you move

- Business Seller Sanity Checklist

- What to compare before you sign & making the right choice for your exit

- Frequently asked questions

Smart planning before you sign can save you more than negotiating the price.

A year ago, Marcus had just closed his third decade running a manufacturing business in the Chicago suburbs. At the same time, he had his retirement mapped out and a buyer making serious offers.

Marcus hoped the sale would fund a clean exit and a move to Florida.

Unfortunately, Marcus was very average at tax planning. He wasn’t clued up on sale structures, he wasn’t aware of Illinois compliance steps, and he couldn’t tell the difference between an asset sale and a stock sale.

In fact, he was so unprepared he’d been cautioned by his accountant many times about waiting too long to model the tax hit.

Marcus had a closing lined up at his attorney’s office to sign the purchase agreement, and after that, he was planning to file dissolution documents and leave the state.

It was a loose plan. The specifics of how exactly he was going to minimize his tax liability were missing.

Marcus never considered that restructuring the deal as an installment sale with strategic allocation would save him more than the original price negotiations, let alone that relocation timing could affect his Illinois tax exposure.

After weeks of late-night calls with a business exit advisor, it was finally clear what needed to change.

All Marcus needed was a better deal structure and a timeline that put tax planning first.

However, he got an education in how much an Illinois business sale can cost when the structure is an afterthought.

This involved rewriting the purchase agreement, adding installment terms, allocating the price across asset classes, and coordinating his move date with payment timing.

So Marcus ended up saving over six figures in tax liability and moved to Florida with a payment schedule that kept him out of the highest brackets.

The kicker? His buyer preferred the installment structure anyway because it improved their cash flow.

The structure you choose, the timing of your relocation, and the compliance steps you take can matter more than the sale price when it comes to what you actually keep. Illinois owners face state tax exposure, final filing requirements, and often a decision about whether to exit a high-tax state before or after closing.

Different strategies work for different business structures. A one-owner LLC has different options than a C-corporation with appreciated stock.

And if you’re planning to move out of Illinois as part of your exit, the timing of that relocation compared to when you close and when you receive payments can shift your tax outcome significantly.

If you’ve been thinking about an exit, now is the time to get serious about your plan. If you need know if your business is order before you take it to market, take a quick business readiness quiz here. Otherwise, let’s get started.

1. Structure the sale as an installment agreement

Instead of taking a lump sum, an installment sale spreads your payments over many years, which can reduce the tax hit in any single year. You receive the sale price over time, and you only recognize gain as payments arrive.

This works well when the buyer wants to finance part of the deal and you’re comfortable carrying a note. It also gives you more control over which tax years you recognize income, which can be useful if your relocation or other income changes are coming.

For Illinois sellers planning a move, installment treatment combined with a change of residency can sometimes improve state tax outcomes, though the specifics depend on sourcing rules and should be reviewed with a tax advisor.

How fast you’ll see the benefit: The tax savings begin in the sale year and continue each year you receive payments.

What you need: A willing buyer, a purchase agreement that structures deferred payments, and legal documentation to secure the note.

2. Negotiate a stock sale instead of an asset sale when possible

A stock sale means you’re selling ownership of the company as opposed to selling each person asset. For the seller, this often means simpler tax treatment and more favorable capital gains rates.

Asset sales can trigger ordinary income on inventory, receivables, and depreciation recapture, while a stock sale may allow more of the gain to qualify for long-term capital gains treatment.

Buyers usually prefer asset sales because they get a step-up in basis and can write off the purchase price faster. That means you may need to negotiate hard or offer a price adjustment to get stock sale treatment.

How fast you’ll see the benefit: Immediate, at the time of sale.

What you need: A corporate structure that allows stock sales, a cooperative buyer, and careful drafting of the purchase agreement.

3. Allocate the purchase price strategically across asset classes

In an asset sale, how you and the buyer allocate the purchase price across goodwill, equipment, inventory, receivables, and other assets can change your tax bill significantly.

Goodwill and intangibles are often taxed more favorably than inventory or receivables. Equipment may trigger depreciation recapture.

A thoughtful allocation that favors capital gain treatment on as much of the price as possible can save substantial tax.

The buyer will have their own tax interests, so allocation is usually a negotiation. But if you leave it to default IRS rules or let the buyer dictate the terms, you may pay more tax than necessary.

How fast you’ll see the benefit: Immediate, at the time of sale.

What you need: A tax advisor who understands Form 8594 and asset allocation rules, and a purchase agreement that specifies the allocation.

4. Use Qualified Small Business Stock exclusion if you qualify

Section 1202 allows you to exclude up to $10 million or ten times your basis in gain from the sale of qualifying C-corporation stock, whichever is greater.

The catch is that the stock must meet specific requirements: it has to be original issue stock from a domestic C-corporation with less than $50 million in assets when the stock was issued, you must have held it for at least five years, and the company must be engaged in an active trade or business.

If your business qualifies, this can be one of the most powerful tax exclusions available.

How fast you’ll see the benefit: Immediate, at the time of sale.

What you need: A qualifying C-corporation, original issue stock held for five years, and careful documentation to prove QSBS status.

5. Sell to an ESOP to defer or eliminate capital gains

An Employee Stock Ownership Plan lets you sell stock to your employees through a trust. If the company is a C-corporation and you sell at least 30% of the stock to the ESOP, you can reinvest the proceeds in qualified replacement property and defer capital gains indefinitely under Section 1042.

ESOPs take planning and cost money to set up, but for the right business, they can provide a tax-free exit, continuity for employees, and an ongoing retirement benefit for the workforce.

This strategy works best for profitable companies with at least 15 to 20 employees and owners who want a gradual transition as opposed to an immediate full exit.

How fast you’ll see the benefit: Immediate tax deferral if reinvestment requirements are met.What you need: A C-corporation, a feasibility study, an ESOP consultant.

6. Use a Charitable Remainder Trust for partial tax deferral

If you have charitable intent and a highly appreciated business, you can contribute stock or ownership interests to a Charitable Remainder Trust before the sale. The trust sells the business without paying capital gains tax, then pays you an income stream for life or a set term, with the remainder going to charity.

This won’t eliminate your tax bill, but it can spread it out, reduce it through the charitable deduction, and create a predictable income stream in retirement.

CRTs are complex, need professional administration, and lock you into a charitable commitment. They work best when your sale price is large, your basis is low, and you already planned to make significant charitable gifts.

How fast you’ll see the benefit: Partial immediate deduction, then income over time.

What you need: A qualified appraiser, a CRT attorney, a trustee, and charitable beneficiaries you want to support.

7. Time your relocation carefully if you’re leaving Illinois

Illinois taxes residents on all income, regardless of source, and taxes nonresidents on Illinois-source income. If you’re planning to leave Illinois as part of your business exit strategy, when you move compared to when you sell and when you receive payments can affect your state tax bill.

Changing your residency before closing won’t automatically eliminate Illinois tax if the income is sourced to Illinois. But depending on the structure, timing, and type of income, a relocation combined with installment payments or deferred structures may reduce Illinois exposure.

This is one of the most fact-specific planning areas. You need to consider domicile rules, statutory residency tests, income sourcing, and whether Illinois will claim a piece of the gain even after you leave.

How fast you’ll see the benefit: Depends on when you move and when income is recognized.

What you need: Clear documentation of your move, residency planning, and advice from a tax professional who understands multi-state taxation.

8. Handle Illinois dissolution and compliance steps before you move

If you’re closing the business after the sale, Illinois needs you to file dissolution documents, cancel registrations and licenses, file final state tax returns, handle payroll obligations, and keep records for the required retention period.

Skipping these steps can leave you with ongoing filing obligations, notices, penalties, and unresolved tax liabilities that follow you even after you relocate.

Many owners focus on the sale and forget the administrative shutdown. That can create surprise tax bills, compliance gaps, and headaches months or years later.

How fast you’ll see the benefit: Immediate compliance and peace of mind.

What you need: Dissolution filings with the Illinois Secretary of State, final tax returns, license cancellations, and a compliance checklist.

Business Seller Sanity Checklist

As we covered in the first part of this series, it’s time for another seller sanity check. Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If your business is valued at $1 to $40 million, an experienced business broker like Earned Exits will leverage more potential buyers and an average increase of profit of 20 to 30% more than going it alone.

Stated simply, alone is cheaper, but not always most profitable. Our comprehensive review of Earned Exits business brokers here.

To learn more about preparing your business for maximum value, see our comprehensive guide here.

The company has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes real value for owners selling businesses valued $1M–$40M+. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

What to compare before you sign & making the right choice for your exit

The best tax strategy for selling your business depends on your entity type, the buyer’s preferences, your cash flow needs, and whether you’re staying in Illinois or relocating.

If you’re keeping it simple and want immediate cash, a stock sale with careful allocation is usually the starting point. If you’re willing to carry a note and spread out the tax hit, installment treatment gives you more control.

If you’re charitably inclined or want to reward employees, CRTs and ESOPs can work.

And if you’re planning to leave Illinois, the timing of your move compared to the closing and payment schedule can shift the outcome enough that it’s worth modeling before you commit.

The structure you agree to in the letter of intent usually becomes the structure you’re stuck with. Once the purchase agreement is signed, your options narrow fast.

That’s why the planning needs to happen before you shake hands, not after the deal is done.

Work with a CPA and business broker that specializes in business exits. The cost of that advice is almost always a fraction of the tax you’ll save by getting the structure right the first time.

Brokering over $2.1 Billion in transactions across 17 industries, Earned Exits was named a top business broker in 2025 by IWSP.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

Frequently asked questions

What is the best way to avoid taxes when selling a business in Illinois?

Complete avoidance is rare and usually needs specific structures like a qualified reorganization, QSBS exclusion, or ESOP combined with Section 1042 reinvestment. Most sellers focus on reducing and deferring tax through installment sales, stock sale treatment, strategic allocation, and timing of payments and relocation.

Should I move out of Illinois before I sell my business?

Sometimes. The answer depends on how the income will be sourced, whether the sale is structured as a lump sum or installment payments, and whether Illinois will claim a piece of the gain even after you become a nonresident.

Residency and sourcing rules are complex and vary by fact pattern, so this should be reviewed with a tax professional before you move.

What is the difference between a stock sale and an asset sale?

In a stock sale, you sell ownership shares of the company, and the business continues under new ownership with the same assets and liabilities. In an asset sale, you sell the person assets of the business, and the buyer picks what they want.

Stock sales are often better for sellers because more of the gain may qualify for capital gains treatment, while asset sales can trigger ordinary income and depreciation recapture.

How does an installment sale reduce taxes?

An installment sale spreads your gain recognition over the years you receive payments, which can keep you out of higher tax brackets and reduce the tax hit in any single year. You pay tax as you receive cash, as opposed to paying tax on the entire gain in the year of sale even if you didn’t receive all the money yet.

Do I need to file dissolution documents if I sell my Illinois business?

It depends on the deal structure. If the buyer is purchasing the stock or membership interests, the entity continues and you don’t dissolve it.

If the buyer is purchasing the assets and the entity is winding down, you need to file dissolution documents with the Illinois Secretary of State, cancel licenses and registrations, and file final tax returns.

What is QSBS and how much tax can it save?

Qualified Small Business Stock under Section 1202 lets you exclude up to $10 million or ten times your basis in gain from the sale of qualifying C-corporation stock. That can save you millions in federal tax if you meet the requirements, which include holding original issue stock for at least five years and meeting other specific tests.

Can I use a 1031 exchange when selling my business?

1031 exchanges are for real property, not business sales. If part of your business sale includes real estate held for investment or business use, that portion might qualify for a 1031 exchange, but the sale of goodwill, equipment, inventory, and other business assets generally does not qualify.

This is a narrow exception and needs careful structuring.

References and Sources

[1] Internal Revenue Service. “Installment Sales.” IRS Publication 537.

Available at: https://www.irs.gov/publications/p537

[2] Illinois Department of Revenue. “Income Tax Regulations.” Available at: https://www.revenue.state.il.us/

[3] Illinois Small Business Development Center. “Closing Your Business.” Available at: https://www.ilsbdc.biz/

[4] Internal Revenue Service. “Sale of Business.” IRS Tax Guide for Small Business.

Available at: https://www.irs.gov/publications/p334

[5] Illinois Compiled Statutes. “Business Corporation Act.” Available at: https://www.ilga.gov/legislation/ilcs/ilcs.asp

[7] Internal Revenue Service. “Form 8594: Asset Acquisition Statement.” Available at: https://www.irs.gov/forms-pubs/about-form-8594

[8] Internal Revenue Service. “Section 1202, Qualified Small Business Stock.” Available at: https://www.irs.gov/

[10] National Center for Employee Ownership. “ESOP Tax Incentives and Contribution Limits.” Available at: https://www.nceo.org/

[11] Illinois Secretary of State. “Business Services, Dissolution.” Available at: https://www.cyberdriveillinois.com/

[13] Internal Revenue Service. “Capital Gains and Losses.” IRS Publication 544.

Available at: https://www.irs.gov/publications/p544

[14] Illinois Department of Revenue. “Final Returns and Business Closings.” Available at: https://www.revenue.state.il.us/

Additional professional resources referenced include guidance from state bar associations, certified public accountant materials on business exit planning, and multi-state taxation treatises on residency and income sourcing rules.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.