Quick Summary

Successfully selling your business requires a structured, disciplined process, not just finding a buyer and agreeing on price.

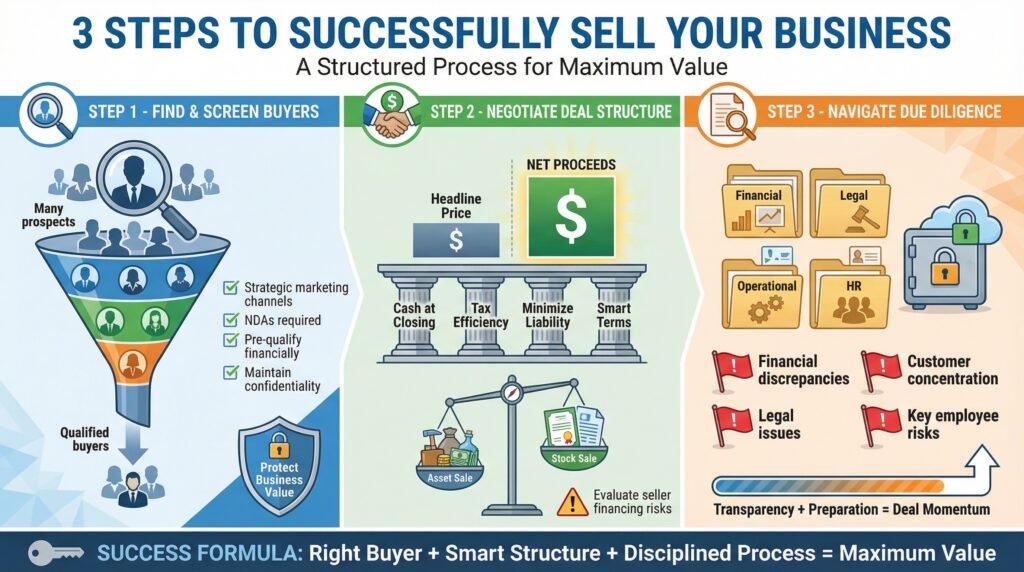

- Find & Screen Buyers

Focus on qualified, financially capable buyers,not volume. Use strategic marketing channels, require NDAs, and pre-qualify prospects before sharing sensitive details. Maintain confidentiality and control communication with employees and customers to protect business value. - Negotiate the Deal Structure

Structure matters more than headline price. Prioritize cash at closing, tax efficiency, and minimized future liability. Understand asset vs. stock sale tax implications, evaluate seller financing risks, use earnouts carefully, and negotiate realistic non-compete and transition terms. Always assess net proceeds, not just offer price. - Navigate Due Diligence

Prepare for deep financial, legal, operational, and HR scrutiny. Organize documentation early, use a secure data room, and proactively address potential deal-killers like financial discrepancies, customer concentration, legal issues, or key employee instability. Transparency and preparation preserve trust and maintain momentum.

Bottom Line:

The right buyer, smart deal structure, disciplined due diligence, and professional guidance dramatically increase your chances of maximizing value and successfully closing.

In part 1 of this business sales series, we will cover what you need before selling your business, how to value your business accurately, and more. In part 2, we will cover finding and screening potential buyers, negotiating a sales structure, and many other critical elements for your business sale.

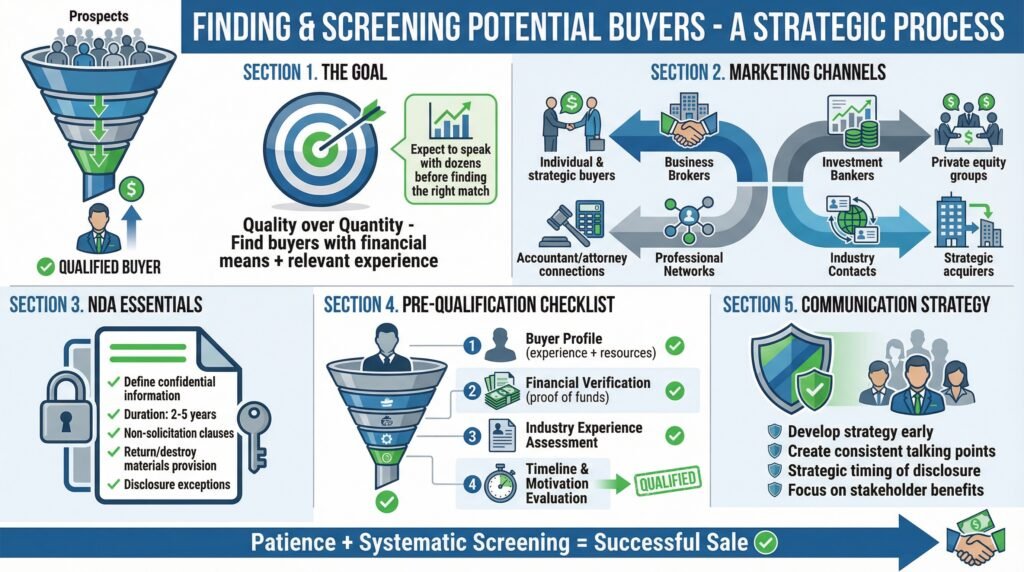

Step 3: Find and Screen Potential Buyers

Finding the right buyer requires a strategic approach that balances confidentiality with sufficient market exposure. Unlike selling real estate, business sales typically involve a more targeted and discreet marketing approach. The goal isn’t to attract the most prospects, but rather to identify and connect with the most qualified potential buyers who have both the financial means and relevant experience to successfully acquire and operate your business.

This phase requires patience and discipline. It’s common to speak with dozens of potential buyers before finding the right match. Having a systematic approach to screening inquiries preserves your time while protecting sensitive information about your operations.

Marketing Channels That Attract Serious Buyers

Different types of businesses attract different buyer profiles, requiring tailored marketing strategies. Business brokers like Earned Exits provide exposure to individual buyers actively searching for opportunities and can connect you with strategic buyers already operating in your field.

For larger businesses, investment bankers can identify and approach private equity groups or strategic acquirers that might see synergies in your operations. Networking within professional circles and leveraging your accountant’s or attorney’s connections often uncovers serious prospects not actively searching but interested when presented with the right opportunity.

Non-Disclosure Agreements: What to Include

Creating accountability for prospects. Include clear definitions of what constitutes confidential information and how it may and may not be used. Specify the duration of confidentiality obligations, typically 2-5 years, depending on your industry. Address permitted disclosure exceptions, such as sharing with professional advisors who are also bound by confidentiality.

Consider including non-solicitation clauses that prevent prospects from recruiting your employees or approaching your customers for a defined period. For especially sensitive situations, add provisions requiring the destruction or return of confidential materials if discussions don’t proceed, along with notification requirements for any legally compelled disclosure.

Pre-Qualifying Buyers Before Sharing Details

Effective pre-qualification saves countless hours and protects sensitive information from unserious prospects. Require prospective buyers to complete a buyer profile detailing their experience, financial resources, and acquisition criteria before sharing specific information about your business.

Verify financial capability through proof of funds or a financial statement review, recognizing that serious buyers understand this step. Assess relevant industry experience and management capabilities, as lenders typically require this for financing approval. Evaluate the buyer’s timeline and motivation, focusing on those with urgency and clear reasons for acquiring a business like yours.

Handling Employee and Customer Questions

Managing communication during the sale process prevents damaging rumors that could undermine your business value. Develop a communication strategy well before you need it, deciding when and how you’ll inform different stakeholder groups about the pending transition. Create consistent talking points emphasizing business continuity and the positive aspects of the transition when questions inevitably arise. Consider timing disclosures strategically, with key employees and customers often informed later in the process when a deal is more certain. When discussions do happen, focus on how the change benefits them rather than your personal reasons for selling.

Step 4: Negotiate the Sale Structure

The structure of your business sale often matters more than the headline price. A well-structured deal maximizes after-tax proceeds while managing risk for both parties. This negotiation phase requires balancing competing interests: you want maximum cash at closing with minimal ongoing liability, while buyers typically prefer to share risk through payment structures tied to future performance. Understanding the options and their implications helps you negotiate terms that achieve your core objectives.

Seller’s Priority Matrix

Cash at closing: Highest priority for most sellers

Tax efficiency: Critical for maximizing net proceeds

Future liability: Minimize ongoing risk exposure

Transition period: Balance between a clean break and ensuring success

When evaluating offers, calculate the actual net proceeds after taxes, transition costs, and contingent payments. A seemingly lower offer with more favorable terms may actually deliver greater value than a higher headline price with risky payment structures or unfavorable tax consequences.

Remember that every aspect of the deal structure is negotiable. Creative approaches often help bridge gaps between what you need and what buyers can finance. The key is understanding which elements matter most for your personal financial goals and post-sale plans.

Asset Sale vs. Stock Sale: Tax Implications

The tax consequences of asset versus stock sales create significantly different outcomes for buyers and sellers. In an asset sale, the buyer purchases individual business assets rather than your legal entity, typically resulting in ordinary income tax for you on most proceeds but providing the buyer with favorable depreciation benefits through a stepped-up basis.

Stock sales generally create more favorable capital gains treatment for sellers but leave buyers with existing tax basis and potential unknown liabilities. C-corporations face potential double taxation in asset sales (corporate and shareholder levels), while pass-through entities like S-corporations and LLCs generally avoid this issue. The optimal structure depends on your entity type, length of ownership, and the buyer’s financing and risk tolerance.

Seller Financing: Benefits and Risks

Offering seller financing can significantly expand your pool of qualified buyers and potentially increase your sale price by 15-20%. This approach demonstrates confidence in your business’s future performance and helps buyers overcome financing challenges, particularly for goodwill or intangible assets that traditional lenders hesitate to finance. Seller notes typically cover 10-30% of the purchase price with interest rates 1-3% higher than bank rates.

However, this benefit comes with substantial risk. You’re effectively becoming the bank, with your repayment dependent on the buyer’s successful operation of the business. Protect yourself with proper loan documentation, personal guarantees from the buyer, and security interests in business assets. Consider negotiating standby agreements with senior lenders that clarify your rights if the buyer defaults.

Structure seller financing to align incentives, using mechanisms like balloon payments to encourage refinancing when the business stabilizes under new ownership. If you need immediate liquidity, explore note-selling options with specialized investors who purchase seller notes at a discount.

Earnouts: When They Make Sense

Earnouts bridge valuation gaps by tying a portion of the purchase price to future business performance. These arrangements typically involve additional payments if specific metrics (revenue, profit, customer retention) meet agreed targets over a defined period, usually 1-3 years post-closing. They’re particularly useful when you claim significant growth potential that the buyer isn’t willing to pay for upfront or when business performance has been inconsistent.

Designing effective earnouts requires careful attention to details. Define performance metrics that you can directly influence if you’re remaining involved, or that are objective and difficult to manipulate if you’re departing. Include clear measurement periods, calculation methodologies, and dispute resolution mechanisms to prevent conflicts.

Recognize that earnouts introduce significant risk to your compensation. Only agree to earnouts for a portion of the purchase price after securing a guaranteed base payment that meets your minimum needs. Consider how the buyer’s operating decisions might impact the metrics, and negotiate appropriate control or consultation rights during the earnout period.

Non-Compete and Transition Period Terms

Typical Transition Support Arrangements

Full-time employment: 1-3 months

Part-time consulting: 3-12 months

On-call availability: Up to 24 months

Non-compete duration: 2-5 years (geographic limitations apply)

Post-closing restrictions and transition support are critical aspects of most business sales. Non-compete agreements prevent you from starting or joining competing businesses within specified geographic areas and timeframes, typically 2-5 years within your current market area. Courts generally enforce these restrictions when they’re reasonable in scope and necessary to protect the business value being purchased.

Transition periods help transfer relationships and knowledge to the new owner. Structure these arrangements to align with your post-sale plans, defining specific responsibilities, time commitments, and compensation. Consider structuring transition services as a separate consulting agreement rather than making them contingent on closing to maintain leverage if issues arise.

When negotiating these terms, be realistic about your willingness to remain involved after closing. Overpromising availability or underestimating the emotional challenge of stepping back can create significant stress during transition. Balance the buyer’s legitimate need for knowledge transfer with your desire for a clean break.

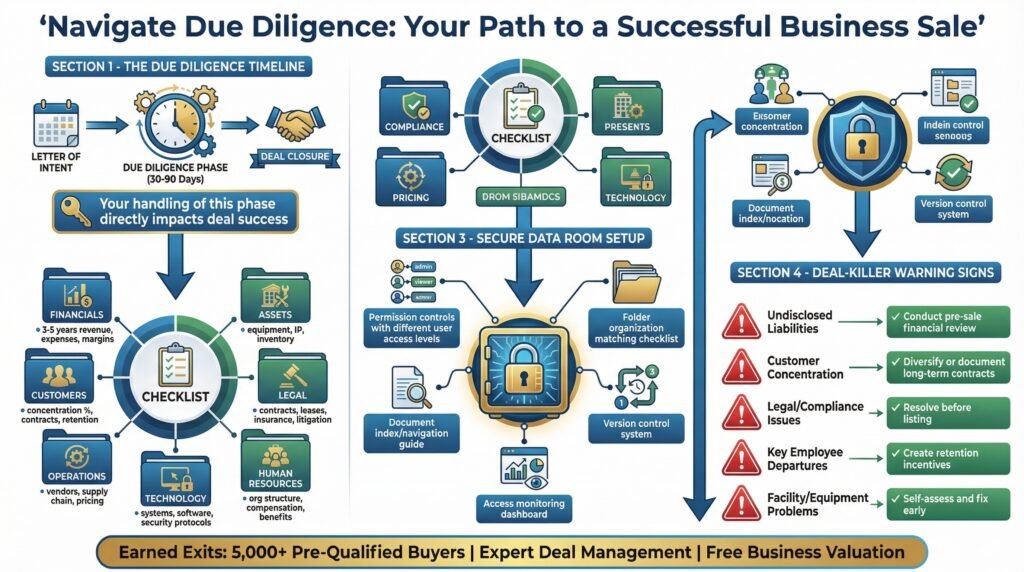

Step 5: Navigate Due Diligence

Due diligence is the investigative phase where your buyer verifies everything you’ve claimed about your business. This process typically begins after signing a letter of intent and can last anywhere from 30 to 90 days, depending on your business complexity. While buyers lead this process, proactive sellers maintain control by anticipating information requests and organizing materials in advance.

The way you handle due diligence significantly impacts whether your deal closes successfully. Transparency builds trust, while surprises or delays create doubt that can derail negotiations or reduce your final price. Be prepared for buyers to scrutinize every aspect of your business, from financial records to customer relationships and operational procedures.

Creating a Due Diligence Checklist

A comprehensive due diligence checklist helps manage the information flow and prevents critical oversights. Begin with financial verification, including a detailed analysis of revenue streams, expense categories, and profit margins for the past 3-5 years. Prepare documentation of all assets, including equipment lists, intellectual property, and inventory, with current valuations. Organize customer information showing concentration percentages, contract terms, and historical retention rates. Gather all legal documents, including contracts, leases, loans, insurance policies, and any pending litigation or claims.

Include operational details like vendor relationships, supply chain documentation, and pricing agreements. Human resources information should cover organizational structure, compensation plans, benefit programs, and employee agreements. Compile regulatory compliance records, permits, and inspection reports relevant to your industry. For technology-dependent businesses, include system architecture, proprietary software, data security protocols, and backup procedures.

Setting Up a Secure Data Room

A virtual data room provides secure access to confidential information while maintaining an audit trail of who accessed which documents. Choose a platform with permission controls that allow different access levels for various stakeholders – your attorney needs different information than your buyer’s financing bank. Organize documents logically with clear naming conventions and folder structures that match your due diligence checklist categories. Update documents promptly when changes occur, maintaining version control to avoid confusion.

Include a document index or guide that helps the buyer navigate available information efficiently. Set appropriate access timeframes that create urgency without rushing the process unreasonably. Monitor access patterns to identify which documents receive the most attention, as these often signal the buyer’s primary concerns or interests.

Common Deal-Killers and How to Prevent Them

Understanding what typically derails transactions helps you proactively address potential issues. Undisclosed liabilities or financial discrepancies between reported results and verifiable numbers create immediate distrust. Address this by conducting your own financial review before beginning the sales process. Customer concentration, where a few clients represent a disproportionate percentage of revenue, raises transition risk concerns. Mitigate this by developing strategies to diversify your customer base or documenting long-term contracts with key accounts.

Regulatory compliance issues or pending litigation can immediately terminate buyer interest. Resolve outstanding legal matters before listing when possible, or provide clear documentation and resolution paths for those that remain. Key employee departures during the sale process signal instability. Prevent this by identifying critical staff early and creating retention incentives tied to successful transition. Facility or equipment issues discovered during physical inspection often prompt renegotiation. Conduct your own assessment and address obvious problems before buyers identify them.

Working with Earned Exits during due diligence provides an experienced buffer between you and potential buyers, helping manage information flow while maintaining deal momentum through inevitable challenges.

Earned Exits has developed particular expertise in strategic buyer identification, maintaining extensive relationships with acquirers across multiple industries. Their proprietary database includes over 5,000 pre-qualified buyers actively seeking specific acquisition opportunities.

This buyer network creates competitive dynamics that frequently result in multiple offers and premium valuations for properly positioned businesses. This, in turn, supports the ability to create a profitable negotiating sales structure as well. Get started with a free business valuation via the link below.

In part 3 of this business sales series, we will discuss the process of closing the deal and handling post-sale transitions. Subscribe and follow our blog to stay up-to-date on the most recent publications.

Frequently Asked Questions

The following questions address common concerns that arise during business sale preparations. While every business has unique circumstances, these general guidelines provide a foundational understanding of what to expect throughout the process.

What happens to my employees when I sell?

Employment transitions depend on the sales structure and buyer plans. In asset sales, employees are technically terminated by the seller and rehired by the buyer, though this often appears seamless in practice. Stock sales generally continue employment relationships automatically under new ownership. Most buyers retain key staff to maintain operational continuity, though management roles most often see changes. Some purchase agreements include employee retention requirements, particularly for key personnel essential to business success.

Should I tell customers I’m planning to sell?

Generally, customers should not be informed during early sale stages due to significant risks. Premature disclosure creates uncertainty that competitors can exploit, potentially eroding your customer base before closing. Customer concerns about service continuity or relationship changes may trigger contract reviews or vendor diversification that damages business value.

Instead, develop a coordinated announcement strategy with the buyer for implementation after signing definitive agreements or nearing closing. This approach maintains business stability while allowing for controlled messaging that emphasizes continuity and enhanced capabilities rather than ownership changes.

How do lease agreements affect the sale of my business?

Lease agreements can significantly impact transferability and value, particularly for location-dependent businesses. Review assignment clauses early in your preparation process, as many leases require landlord consent for ownership transfers. Favorable leases with below-market rates and reasonable renewal options enhance value, while short remaining terms or assignment restrictions may concern buyers. Consider negotiating lease extensions or more favorable transfer terms before listing to remove this potential obstacle.

What taxes will I pay when selling my business?

Tax consequences vary dramatically based on sale structure, business entity type, and asset allocation. Asset sales typically generate a combination of capital gains tax (15-20% federal rate) on appreciated assets and ordinary income tax (up to 37% federal rate) on depreciated equipment, inventory, and allocations to non-compete agreements. Stock sales generally receive more favorable capital gains treatment on the entire purchase price. Additional considerations include potential recapture of depreciation, state taxes that vary by jurisdiction, and the 3.8% net investment income tax for higher-income sellers.

How do I handle outstanding business loans during a sale?

Business debt resolution typically follows one of three paths during sales. Many sellers use sale proceeds to pay off loans at closing through escrow arrangements that transfer clean assets to the buyer. Alternatively, buyers sometimes assume existing loans with lender approval, particularly for favorable financing terms or when loans are secured by assets being transferred. In some cases, loans remain the seller’s responsibility with payment mechanisms structured from future business cash flows. Each approach has different implications for purchase price, closing complexity, and post-sale obligations.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.