Quick Summary

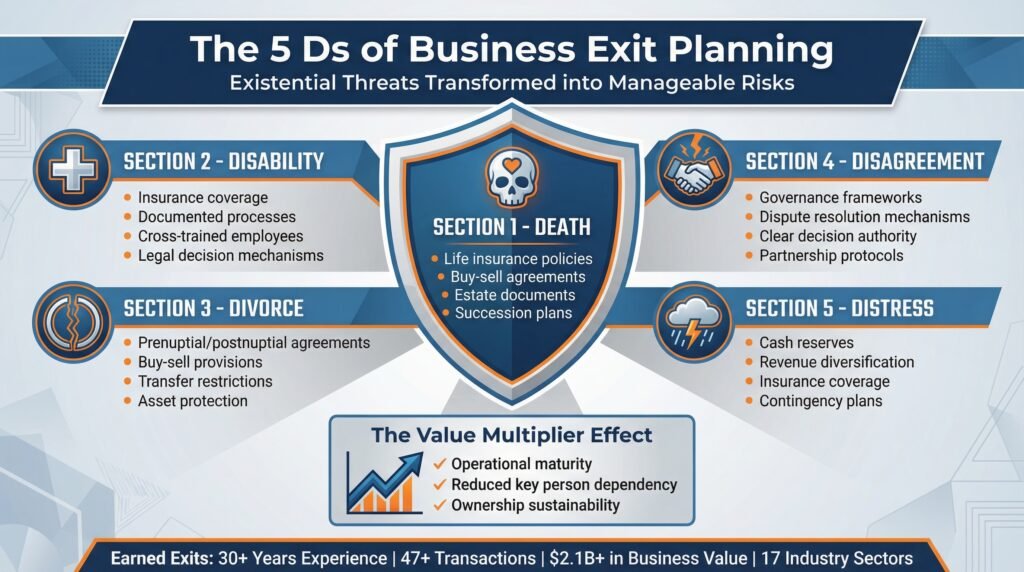

Beyond death, disability, and divorce, disagreement and distress are two of the most common and most destructive exit risks.

Partner disagreements slowly erode value through stalled decisions, toxic culture, and lost opportunities. Clear partnership agreements, defined decision rights, structured communication, and mediation clauses help resolve conflict before it paralyzes the business.

Distress comes from external shocks like economic downturns, customer loss, supply chain failures, or cyber events. Businesses that survive maintain strong cash reserves, diversified revenue, appropriate insurance, and detailed contingency plans. Proactive planning and well-designed buy-sell agreements turn these risks from existential threats into manageable exit events.

In part 1, we discussed the first 3 D’s of business exiting to be aware of: death, disability, and divorce. In part 2, we will discuss the remaining 2 D’s to be aware of in the business exit planning series on best practices.

Disagreement

Partner disagreements represent slow-motion disasters that gradually destroy business value through paralysis, missed opportunities, and toxic culture. Unlike sudden events like death or disability, disagreements fester over months or years, consuming management attention and eroding organizational effectiveness until the business barely functions.

The conflicts start innocuously enough. Partners disagree about growth strategy, where one wants aggressive expansion while the other prefers conservative growth.

They disagree about capital allocation, where one wants to reinvest profits while the other wants distributions.

They disagree about hiring, marketing, and product development, and eventually, everything becomes a battleground.

I’ve watched before successful partnerships deteriorate into destructive stalemates. Partners stop communicating directly and start working through attorneys.

They veto each other’s proposals reflexively rather than on merit.

They compete for employee loyalty and client relationships. The business becomes a battlefield rather than a collaborative enterprise, and everyone loses.

The operational impact extends throughout the organization. Employees sense the tension and start choosing sides.

Strategic initiatives stall because partners can’t agree on direction.

Investment opportunities pass because ownership can’t make timely decisions. Clients notice the dysfunction and start questioning whether the business will survive, making them vulnerable to competitor approaches.

Comprehensive partnership agreements establish clear governance structures before conflicts emerge. These documents define decision-making authority, profit distribution formulas, roles and responsibilities, and dispute resolution procedures.

Well-drafted agreements specify which decisions require unanimous consent, which require majority approval, and which person partners can make independently.

Structured communication protocols create formal channels for strategic discussions and concern resolution. Many partnership conflicts escalate because partners lack regular forums for addressing concerns before they become crises.

Monthly or quarterly strategic meetings with defined agendas create space for productive disagreement within professional boundaries.

Mediation and arbitration clauses provide effective alternatives to litigation for resolving intractable disputes. Litigation destroys business value through legal fees, public disclosure of confidential information, and management distraction.

Mediation and arbitration keep disputes private, decide them faster, and cost dramatically less than courtroom battles.

Clear role definitions and governance frameworks minimize power struggles by establishing explicit responsibilities. When partners understand their specific domains of authority and decision rights, conflicts decrease because territorial disputes have less room to develop.

An experienced business broker can help every business partnership and owner navigate the terrain of uncertainties and disagreements when it is time to exit and sell the company. Click below to contact Earned Exits today to receive a free business valuation and discover how our proven 10-step process can help you achieve the maximum value for your business

Distress

Distress encompasses the external shocks and financial pressures that threaten business viability, regardless of how well you’ve managed internal operations.

The COVID-19 pandemic provided the most dramatic recent example where businesses that were thriving in February 2020 faced existential threats by April when revenue vanished overnight.

The challenge with distress scenarios comes from their unpredictability and variety. Financial distress might stem from major customer concentration when your largest client suddenly ends.

Operational distress might result from supply chain disruption when your critical supplier faces bankruptcy.

Market distress might follow an economic recession when overall demand collapses. Technology distress might occur when cyber-attacks compromise your systems or data.

I’ve watched businesses with solid fundamentals face catastrophic distress from events entirely outside their control. A manufacturer lost its primary customer, representing 60% of revenue, when that customer was acquired by a competitor.

A retail business faced landlord bankruptcy that suddenly jeopardized its prime location.

A professional services firm experienced a key employee departure that triggered client defections.

The businesses that survived these distress events shared common characteristics. They maintained substantial cash reserves that provided a runway to adapt. They had diversified revenue sources that prevented single-point failures.

They carried appropriate insurance that provided financial cushions during disruptions. They had contingency plans that enabled rapid response rather than a paralyzed reaction.

Cash reserves represent your most versatile distress protection. Conventional wisdom suggests maintaining three to six months of operating expenses, but businesses with high fixed costs, long sales cycles, or significant customer concentration should maintain larger reserves.

Cash provides time to adapt, pivot, and survive when revenue disappears or unexpected expenses emerge.

Revenue diversification reduces catastrophic risk from single customer or market dependencies. If one customer represents more than 20% of your revenue, you’re dangerously concentrated. If one product line generates most of your profit, you’re vulnerable to market shifts.

Systematic diversification might reduce short-term profit margins but dramatically improve long-term survival probability.

Business interruption insurance covers lost revenue during operational disruptions from property damage, natural disasters, or other covered events. This coverage maintains cash flow when you physically cannot operate, preventing financial collapse during recovery periods.

Contingency planning develops specific scenarios and response strategies before crises hit. The best contingency plans address specific threats relevant to your business, including major customer loss, key supplier failure, technology disruption, regulatory changes, or competitive threats.

These plans define trigger points that activate specific responses, preventing decision paralysis when crises actually occur.

Contingency planning develops specific scenarios and response strategies before crises hit. The best contingency plans address specific threats relevant to your business, including major customer loss, key supplier failure, technology disruption, regulatory changes, or competitive threats.

A comprehensive buy-sell agreement should specify trigger events that activate the agreement, including death, disability, retirement, voluntary departure, and divorce. It should define valuation methods for determining business worth, payment terms for buying out departing owners, and funding mechanisms like life insurance.

Key Takeaways

The 5 Ds represent existential threats that can destroy the business value you’ve spent decades building. Systematic planning changes these threats into manageable risks with known solutions.

Death planning needs life insurance, buy-sell agreements, estate documents, and succession plans that enable business continuity when ownership suddenly transfers.

Disability planning demands adequate insurance coverage, documented processes, cross-trained employees, and legal mechanisms enabling others to make decisions during your incapacity.

Divorce planning protects business assets through prenuptial or postnuptial agreements, buy-sell provisions addressing divorce triggers, and transfer restrictions preventing unintended ownership transfers.

Disagreement planning establishes governance frameworks, dispute resolution mechanisms, and clear decision-making authority that prevent partnership conflicts from paralyzing operations.

Distress planning maintains cash reserves, diversifies revenue sources, secures appropriate insurance coverage, and develops contingency plans enabling rapid response to external shocks.

Comprehensive planning addressing all five Ds doesn’t just protect against catastrophic loss. It actively increases business value by demonstrating operational maturity, reducing key person dependencies, and proving sustainability beyond current ownership.

Find out how an experienced business broker, like Earned Exits, can help you navigate the complicated terrain when exiting your business for whatever reason. With over 30 years of combined experience guiding business transitions, the team has successfully facilitated more than 47 successful business transactions worth $2.1 Billion across 17 different business sectors.

Click here to get started today with a free business valuation from Earned Exits and see how their proven 10-step exit process helps owners achieve maximum value on their terms

People Also Asked

What happens to a business when the owner dies?

When a business owner dies without proper planning, the business typically experiences a significant decline. Sales drop an average of 60% within four years, and employment falls by 17%.

Client relationships deteriorate rapidly because they are often tied to the owner personally.

Key employees leave because of uncertainty about the company’s future. Without predetermined succession plans and proper funding through life insurance, the business often gets sold at fire-sale prices or simply closes.

How much disability insurance do business owners need?

Business owners need two types of disability coverage. Personal disability insurance should replace enough income to cover your living expenses, typically 60-70% of your salary.

Business overhead expense insurance should cover fixed business costs like rent, utilities, and essential payroll during your absence.

Calculate your actual monthly business expenses and confirm your coverage matches that amount for at least 12-24 months.

Can my spouse take my business in a divorce?

In community property states, your spouse may be entitled to 50% of the business value accumulated during the marriage, regardless of whose name is on the ownership documents.

In equitable distribution states, courts divide marital property fairly, which doesn’t always mean equally, but can still result in significant business value going to your spouse.

Prenuptial agreements, postnuptial agreements, and buy-sell agreements with divorce provisions can protect business ownership from divorce settlements.

What should a buy-sell agreement include?

A comprehensive buy-sell agreement should specify trigger events that activate the agreement, including death, disability, retirement, voluntary departure, and divorce. It should define valuation methods for determining business worth, payment terms for buying out departing owners, and funding mechanisms like life insurance.

The agreement should also include transfer restrictions preventing owners from selling to outside parties without approval and dispute resolution procedures.

How long does it take to prepare a business for sale?

Preparing a business properly for sale typically takes three to five years. This timeline allows you to document processes, reduce key person dependencies, strengthen financial performance, diversify customer concentration, and develop management teams that can operate without you.

Businesses sold without this preparation period typically receive significantly lower valuations because buyers discount heavily for transition risks.

What percentage of business value should be kept in cash reserves?

Most businesses should maintain three to six months of operating expenses in cash reserves. However, businesses with high customer concentration should keep six to twelve months.

Companies with long sales cycles, high fixed costs, or exposure to economic volatility should maintain even larger reserves.

The specific amount depends on how quickly you could reduce expenses or generate emergency revenue if your primary income source disappeared.

Let the Earned Exits business advisory team guide you through the business exit planning and execution process. The company specializes in comprehensive exit planning that addresses both financial and personal dimensions of business transitions.

Contact Earned Exits today to begin developing your customized exit strategy designed to maximize value while ensuring post-sale fulfillment and security. Get started today with the company’s free business valuation via the banner below and filling out their short form:

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.