Quick Summary

New Jersey business owners can dramatically reduce their tax burden when selling by planning well in advance. The five key strategies are:

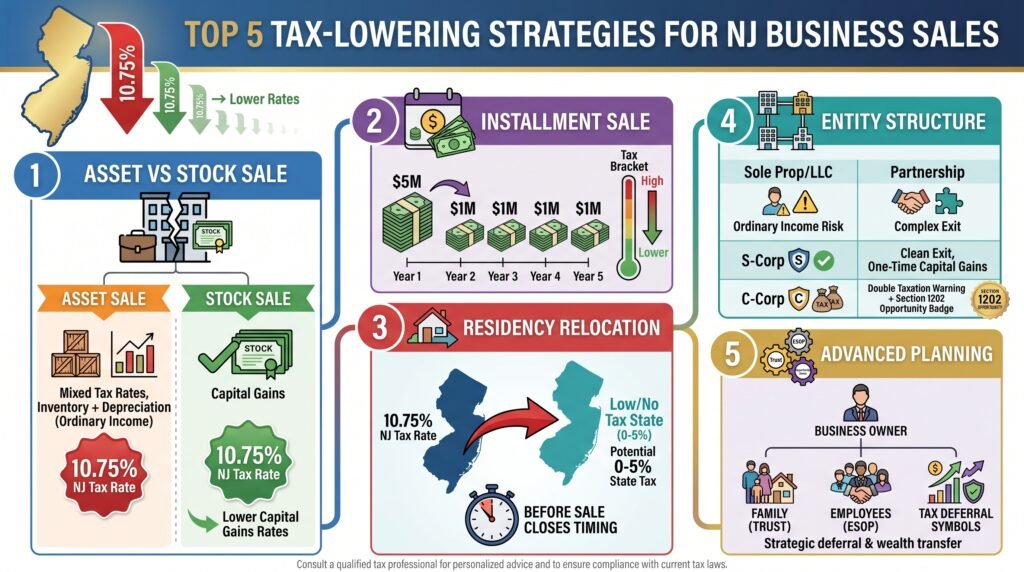

- Asset vs. Stock Sale Structure — Selling stock or membership interests typically generates better capital gains treatment than an asset sale; strategic price allocation (favoring goodwill over inventory/equipment) can cut combined taxes by 10–25%.

- Installment Sales — Spreading payments over multiple years keeps income out of the highest tax brackets and pairs well with relocation planning, potentially saving 5–15% in effective tax rate.

- Residency Relocation — Genuinely moving to a no-income-tax state (like Florida or Texas) before the sale closes can eliminate NJ’s 10.75% top rate on the gain — but requires a real move, 24–36 months of planning, and thorough documentation.

- Entity Structure Cleanup — S corps typically offer the cleanest exits (single-level capital gains); C corps may qualify for the federal QSBS exclusion (up to 100% gain exclusion) if requirements are met. Start 3–7 years out.

- Advanced Tools (Trusts, ESOPs, Opportunity Zones) — For exits over $3M, tools like Charitable Remainder Trusts, ESOPs, and Qualified Opportunity Zone investments can defer or eliminate 20–50% of tax liability.

Bottom line: Owners who start planning 3–5 years early can reduce their total tax burden by 15–30%, potentially saving $600K–$3M+ depending on deal size.

Table of Contents

- Quick Summary

- The strategies that can save you hundreds of thousands when you exit your business.

- Top 5 Tax-Lowering Strategies for New Jersey Business Sales

- 1. Asset vs Stock Sale Structure with Strategic Price Allocation

- 2. Installment Sale to Spread Income Across Multiple Tax Years

- 3. Residency and Relocation Timing Strategy

- 4. Entity Structure Planning and Pre-Sale Cleanup

- 5. Advanced Planning with Trusts, ESOPs, and Opportunity Zones

- Finding the Right Strategy for Your Exit

- Frequently Asked Questions

The strategies that can save you hundreds of thousands when you exit your business.

If you have a pattern of treating taxes as an afterthought when planning to sell your business, then you need to change this approach.

You’re probably continuing this pattern because you don’t see how much it’s costing you. Have you ever focused solely on getting the highest purchase price, only to find out about that taxes consumed 30% or more of your proceeds?

Or maybe you’ve signed a letter of intent without considering whether an asset sale or stock sale would be better for your situation?

When you keep delaying tax planning until right before closing, you’re actually eliminating options that could save you six or even seven figures. This cycle continues because business owners are busy running their companies, and tax planning feels abstract compared to daily operations.

For decades, accountants have told business owners to “talk to your tax advisor” before selling.

But meaningful tax savings rarely happen through last-minute conversations alone. Studies show that owners who begin tax planning three to five years before a sale can reduce their combined federal and state tax burden by 15 to 30 percent compared to those who wait.

Almost everyone who tries the common “we’ll figure out taxes at closing” approach ends up disappointed when they see their net proceeds. This approach simply doesn’t work.

Despite this, it’s still the norm, even among successful business owners. The real solution isn’t something you can fix through quick decisions at the negotiating table.

You need to treat your business exit as a multi-year tax planning project instead.

If you’ve got a business with recurring revenue, professional management, and clean books, you’re in a strong position. If you need know if your business is order before you take it to market, take a quick business readiness quiz here. Otherwise, let’s get started.

Top 5 Tax-Lowering Strategies for New Jersey Business Sales

1. Asset vs Stock Sale Structure with Strategic Price Allocation

The way you structure your deal decides whether you pay capital gains rates on most of the proceeds or get hit with ordinary income rates on significant portions. In an asset sale, the buyer purchases your business assets directly, which often creates a mix of capital gain and ordinary income for you as the seller.

Items like inventory and depreciation recapture get taxed as ordinary income.

In a stock sale or membership interest sale, you sell your ownership in the entity itself, which typically generates more favorable capital gains treatment, especially for C corps and S corps. New Jersey taxes capital gains as ordinary income at rates up to 10.75%, so the federal distinction matters more than the state one, but allocation still affects your overall tax bill significantly.

Total time to apply: Start 12 to 36 months before selling for best results.

Complexity level: Moderate to high. You need experienced tax and legal advisors who understand New Jersey rules.

Who this works for: Any business owner selling a company, but particularly valuable for S corps, C corps, and LLCs with substantial goodwill or intangible assets.

Key requirements: Clean financial records, professional advisors who can model both scenarios, and negotiating power with buyers who may prefer asset sales for their own tax reasons.

Expected tax savings: Can reduce combined tax by 10 to 25 percent of sale price depending on allocation.

The purchase price allocation among categories like goodwill, equipment, real estate, inventory, and consulting agreements makes a massive difference. More allocation to goodwill and capital assets means more capital gain treatment federally.

Less allocation to items that trigger ordinary income or recapture means lower overall tax.

Both buyer and seller must agree to the allocation and report it consistently on Form 8594, so this becomes a negotiation point. Work with your CPA early to understand what allocation would be ideal for your situation, then build that into your negotiating strategy.

If the buyer insists on an asset sale for liability protection, you can often negotiate a higher price or better allocation in exchange for accepting their preferred structure.

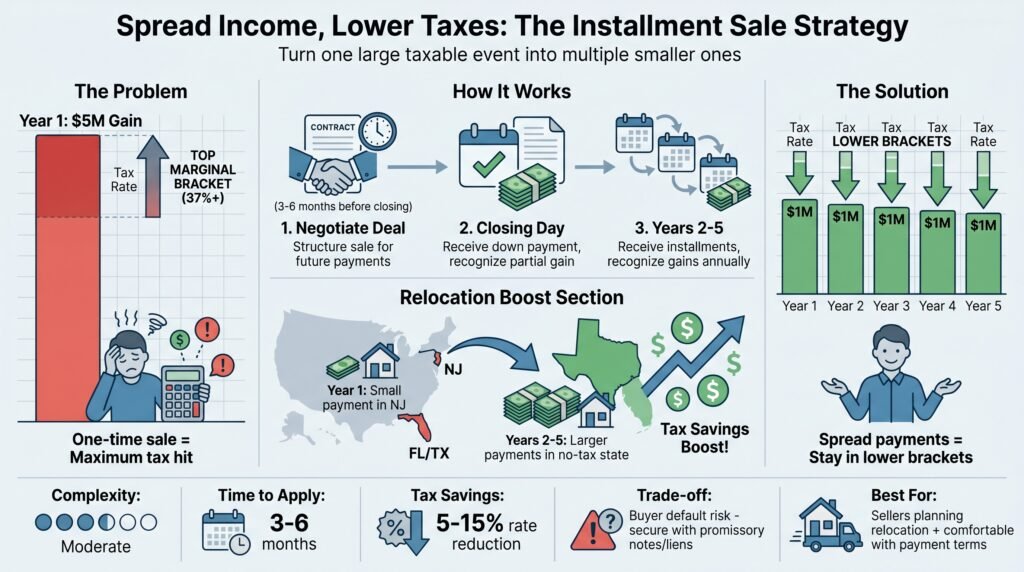

2. Installment Sale to Spread Income Across Multiple Tax Years

An installment sale let’s you receive payments over several years instead of a lump sum at closing. If structured correctly under federal tax rules, you recognize gain as you receive payments, which spreads taxable income across many years.

This approach can keep you out of the highest federal brackets and may reduce the impact of New Jersey’s progressive income tax rates.

Instead of showing a five million dollar gain in one year and paying tax at the top marginal rates on most of it, you might show one million per year for five years, potentially staying in lower brackets.

Total time to apply: Plan during deal negotiation, typically 3 to 6 months before closing.

Complexity level: Moderate. Requires careful contract drafting and understanding of installment sale rules.

Who this works for: Sellers comfortable with payment risk who want to smooth income and potentially coordinate with relocation plans.

Key requirements: Buyers willing to pay over time, adequate security like promissory notes or liens, and professional tax guidance to structure the installment properly.

Expected tax savings: Can reduce effective tax rate by 5 to 15 percent depending on bracket management and state residency planning.

Installment sales work particularly well if you plan to relocate. You might close the sale while still a New Jersey resident with a modest down payment, then receive larger installments after establishing residency in a state with no income tax like Florida or Texas.

Whether New Jersey can tax those later payments depends on sourcing rules and how the deal is structured, so this strategy requires careful planning with advisors who know both New Jersey law and your destination state.

The trade-off is that you carry the risk that the buyer might default on future payments, so negotiate strong security provisions and possibly need interest on the deferred amounts.

3. Residency and Relocation Timing Strategy

Where you live when the gain is recognized decides which state gets to tax it. New Jersey taxes residents on all income regardless of source, which means if you sell your business as a New Jersey resident, the state claims its share of the gain.

But if you establish legal residency in a lower tax state before the sale closes and structure the deal so gain is recognized after you leave, you can potentially eliminate or reduce New Jersey’s 10.75% top rate on the transaction.

This is the core of business exit strategy relocation planning and a major factor in tax and wealth flight from high tax states.

Total time to apply: Best started 24 to 36 months before your target sale date.

Complexity level: High. Residency is determined by many factors and New Jersey will scrutinize any move near a large transaction.

Who this works for: Business owners planning to relocate anyway and willing to make a genuine move, not a paper change.

Key requirements: Establishing a new domicile with home purchase or lease, spending the majority of your time there, changing voter registration and driver’s license, moving family and social ties, and documenting everything carefully.

Expected tax savings: Can eliminate up to 10.75% New Jersey tax on the gain, potentially saving hundreds of thousands to millions on large exits.

Residency is fact-specific and New Jersey looks at the totality of your circumstances. Simply buying a condo in Florida while keeping your primary home, family, and business activities in New Jersey will not change your residency.

You need to genuinely move your life.

Plan to spend more than 183 days per year in your new state, move your important personal and financial relationships, and maintain detailed records of where you spend your time. Even after changing residency, New Jersey can still tax New Jersey source income for non-residents, so how the gain is sourced matters.

An equity sale of stock in an entity may be sourced differently than an asset sale of business property located in New Jersey.

Work with tax professionals who handle multi-state transactions to understand what portion of your gain New Jersey might still claim and how to structure the deal to minimize that.

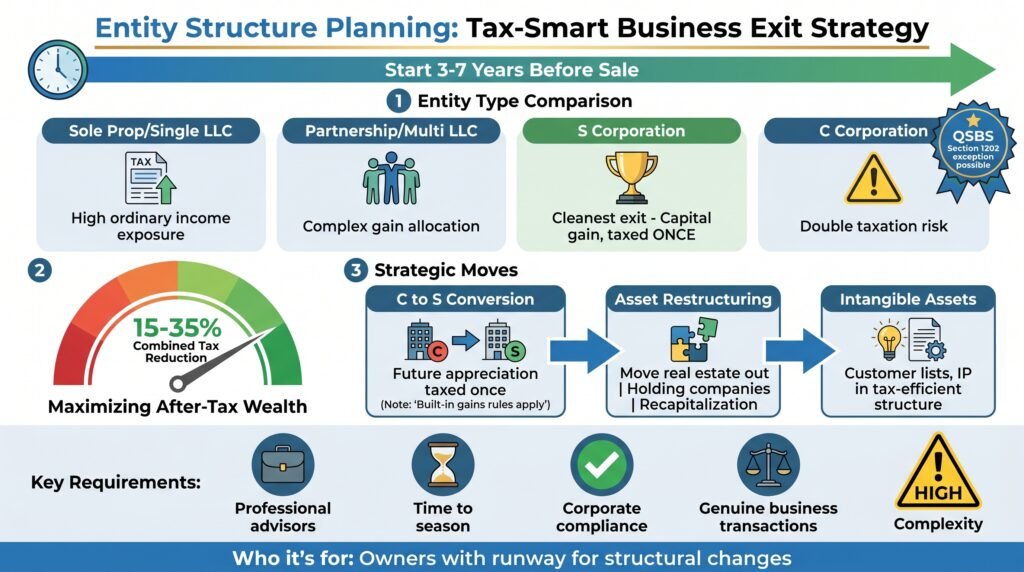

4. Entity Structure Planning and Pre-Sale Cleanup

Your business entity type directly affects your menu of tax options when selling. Sole proprietorships and single-member LLCs report sales on personal returns with potentially more ordinary income exposure.

Partnerships and multi-member LLCs have complex rules about how gain is allocated among partners.

S corporations often provide the cleanest exits because stock sales generate capital gain taxed once at the shareholder level. C corporations can trigger double taxation if you sell assets at the corporate level and then distribute proceeds, but C corp stock sales might qualify for Qualified Small Business Stock exclusions under federal Section 1202 if requirements are met.

Total time to apply: Start 3 to 7 years before selling for best results, particularly if you need to make an S election or restructure.

Complexity level: High. Entity changes have tax consequences and timing requirements.

Who this works for: Business owners with enough runway to make structural changes before a sale.

Key requirements: Professional advice from tax attorneys and CPAs, patience to let elections age properly, and clean compliance with all corporate formalities.

Expected tax savings: Can reduce combined tax by 15 to 35 percent in some cases, particularly when avoiding C corp double tax or qualifying for QSBS treatment.

If you now operate as a C corporation and think you might sell in five to seven years, consider electing S corporation status now. Future appreciation after the election will only be taxed once when you sell stock.

If you converted from C to S recently, built-in gains rules may apply for a period, so timing matters.

If your business has grown significantly and you have valuable intangible assets like customer lists or intellectual property, consider whether those assets are held in the most tax-efficient structure. Pre-sale restructuring might include moving real estate out of an operating entity, creating holding company structures, or recapitalizing to shift future growth.

These moves need to be genuine business transactions, not artificial steps solely for tax avoidance, and they often need years to season before a sale.

5. Advanced Planning with Trusts, ESOPs, and Opportunity Zones

For high-value exits or owners with specific goals around family wealth transfer, employee ownership, or charitable giving, several sophisticated tools can reshape or defer taxes. An intentionally defective grantor trust can let you transfer business interests to family members years before a sale and move future appreciation outside your taxable estate.

Employee Stock Ownership Plans let C corporation owners sell to employees and defer tax by rolling proceeds into qualified replacement securities.

Charitable Remainder Trusts let you donate appreciated business interests to charity, have the trust sell without immediate tax, and receive income over your lifetime while getting a charitable deduction.

Qualified Opportunity Zone investments let you defer federal capital gains by reinvesting sale proceeds into designated economically distressed areas within 180 days.

Total time to apply: Varies widely. Trusts may need 5 to 10 years.

ESOPs take 12 to 24 months.

QOZ investments have a 180-day window after gain recognition.

Complexity level: Very high. These strategies need specialized advisors and significant setup costs.

Who this works for: Larger transactions, typically exits above three million dollars, where the tax savings justify the complexity and cost.

Key requirements: Specialized attorneys, investment advisors, and tax professionals, plus clear non-tax business purposes for the structures you create.

Expected tax savings: Can defer or eliminate 20 to 50 percent of tax liability depending on strategy and structure, but often with trade-offs like giving up control or accepting investment restrictions.

These tools are rarely used in isolation. You might mix a partial ESOP transaction with an installment sale to outside buyers.

Or you might fund a charitable remainder trust with part of your business and sell the rest to family through an installment note.

The complexity and cost mean these strategies make sense primarily when the tax savings are substantial and you have other goals beyond pure tax reduction. If you are charitably inclined anyway, a CRT can be powerful.

If you want employees to own the business after you, an ESOP serves that purpose while providing tax benefits.

QOZ investments need you to redeploy your capital into specific investment types and hold for years to get most benefit, so consider whether that fits your overall financial plan.

Finding the Right Strategy for Your Exit

The most effective approach for most New Jersey business owners combines early entity cleanup with careful deal structure negotiation. If you know you want to sell within three to five years, schedule a meeting with your CPA and a business attorney now.

Run a preliminary valuation and model the tax consequences of selling today under different structures.

Ask whether your current entity type is optimal. Consider whether an S election makes sense.

Begin documenting your financials cleanly and consider whether any assets should be repositioned.

As you get closer to sale discussions, usually within 12 to 24 months of your target date, start thinking seriously about structure and timing. If relocation is part of your plan, begin making genuine moves to establish residency in your target state.

When you receive offers or start negotiations, bring your tax advisor into the conversation early.

Model the tax impact of asset versus stock sales. Negotiate allocation of purchase price.

Consider whether an installment structure makes sense for your situation and risk tolerance.

For larger exits, typically above two to three million dollars in proceeds, explore whether advanced planning tools might help. These are not necessary for every sale, but they can provide meaningful benefits when the numbers justify the complexity.

The key is starting early enough that you have real options, not waiting until you’ve already signed a letter of intent and have limited flexibility.

Your goal should be walking away from the closing table with the most after-tax wealth possible while meeting your other goals around timing, employee treatment, and family wealth transfer.

The difference between planning well and treating taxes as an afterthought can easily be 20 to 30 percent of your total sale proceeds.

However, there are top ranking business brokers that require a smaller part of the sales proceeds, while still delivering 20 -30% higher exit profits than going it alone. We will discuss this further.

On a three-million-dollar business sale, that’s $600,000 to $900,000.

On a ten-million-dollar exit, the planning could save you two to three million dollars.

Those numbers justify the time and cost of working with experienced business brokers. To learn about the many profitable advantages of working an experienced business broker, read our comprehensive article here.

Earned Exits has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes outcomes for business owners.

Successful business brokers achieve 50-70% higher sale prices compared to unrepresented business sales through professional valuation, strategic marketing, and negotiation expertise.

The most effective business brokers maintain confidentiality throughout the sales process while connecting sellers with qualified, vetted buyer networks.

Earned Exits has facilitated over 47 successful business transactions worth $2.1 Billion, demonstrating how specialized industry knowledge translates to exceptional results.

Choosing the right broker involves matching your business size ($1M-$40M+) with a firm whose expertise aligns with your specific industry and sale objectives. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

If you are further along in the process, read our more in-depth article for successful business exit planning when selling your New Jersey business here.

Frequently Asked Questions

Can I avoid New Jersey taxes entirely by moving before I sell my business?

Maybe, but the answer depends heavily on timing, how genuine your move is, and how the gain is sourced. New Jersey taxes residents on all income, so if you sell while you are still a resident, the state will tax the gain regardless of where the business is located. If you establish true legal residency in another state before the sale and recognize the gain after you have left, you may avoid New Jersey resident tax.

However, New Jersey can still tax nonresidents on New Jersey source income, so even after moving you might owe some New Jersey tax if the business is located in New Jersey and the sale is structured in certain ways.

This is highly fact-specific and requires professional guidance.

Simply having a second home in Florida while your family, business, and life stay centered in New Jersey will not change your residency.

How long does it take to change legal residency from New Jersey to another state?

New Jersey looks at factors like where you spend the majority of your days, where your primary home is located, where your spouse and dependents live, where you are registered to vote, where your driver’s license is issued, where you have bank and brokerage accounts, where you attend religious services, and many other factors.

A genuine change typically requires physically moving yourself and your family to the new state, establishing a new home there, spending more than half the year there, and shifting your personal, social, and financial life.

You should plan on at least 12 to 24 months of clearly documented time in your new state before a major transaction to reduce audit risk.

The closer your move is to a large business sale, the more scrutiny you can expect from New Jersey tax authorities.

What entity type is best for minimizing taxes when selling a business?

For most small to mid-sized business sales, S corporations often provide the cleanest and most favorable tax treatment. When you sell S corp stock, you recognize capital gain taxed once at your level.

There is no entity-level tax on the gain. C corporations can create double taxation if you sell assets inside the corporation and then distribute the proceeds, though C corp stock sales might qualify for Qualified Small Business Stock exclusion if you meet all the technical requirements.

Sole proprietorships and single-member LLCs are treated as disregarded entities, so sales are reported on your personal return, often with a mix of capital gain and ordinary income. Partnerships and multi-member LLCs have complex allocation rules.

The best structure depends on your specific situation, but if you are thinking about selling within five to seven years and now operate as a C corp or sole proprietorship, talk to your CPA about whether electing S corp status makes sense.

What is the Qualified Small Business Stock exclusion and should I count on it?

Section 1202 of the Internal Revenue Code allows taxpayers to exclude up to 100% of gain on the sale of qualified small business stock, subject to limits, if they meet very specific requirements. Your business must be a C corporation.

The stock must have been issued after August 10, 1993.

You must have acquired the stock at original issuance, not by purchase from another shareholder. You must hold the stock for more than five years.

The corporation must meet an active business requirement and asset tests.

The exclusion is limited to the greater of ten million dollars or ten times your basis in the stock. QSBS can provide extraordinary tax savings if you qualify, but the rules are technical and many business owners do not meet all the requirements.

If you think you might qualify, talk about it with a tax advisor well before selling, because some actions like converting from an S corp to a C corp or recapitalizing can reset your holding period or disqualify the stock.

Do I need to file anything special with New Jersey when I close or sell my business?

Yes. If you are selling substantially all the assets of a business, New Jersey’s Bulk Sale law requires the buyer or their attorney to file Form C-9600 and supporting documents with the Division of Taxation before closing.

This form informs the state of the transaction so it can check for outstanding tax liabilities.

If the form is not filed, the buyer can be held responsible for your unpaid New Jersey taxes. You also need to file final federal and state income tax returns for your entity, final employment tax returns if you had employees, and if you are dissolving the entity entirely, file a Certificate of Dissolution for a corporation or Certificate of Cancellation for an LLC with the New Jersey Division of Revenue and Enterprise Services.

Keep all business records for at least seven years after filing your final returns, as the IRS and New Jersey can audit closed businesses.

Do I need a broker to sell my business in New Jersey?

While you can legally sell your business yourself, working with an experienced business broker significantly increases your sale price, shortens the timeline, and improves your odds of closing.

Brokers have buyer networks, understand market valuations, manage the time-consuming process, negotiate effectively, and help avoid common deal-killing mistakes.

The commission they charge typically pays for itself through higher valuations and deal certainty.

The company has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes real value for owners selling businesses valued $1M–$40M+. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

Sources and References

- U.S. Small Business Administration, “7 Tax Strategies to Consider When Selling a Business.”

- The Curchin Group, “New Jersey Sales Tax Planning for Businesses.”

- Weiner Law Group, “Important Considerations When Closing a New Jersey Business.”

- BNY Mellon Wealth, “Reducing the Tax Impact on the Sale of Your Business.”

- Weiner Law Group, “Are You Selling a Business in New Jersey? Here Is a Checklist.”

- KRS CPAs, “The Tax Implications of Closing a Business.”

- Kahn, Litwin, Renza & Co., “How to Avoid or Defer Capital Gains Tax on a Business Sale.”

- New Jersey Division of Taxation, “Starting a Business in NJ / Bulk Sale C-9600 Notification.”

- Internal Revenue Service, “Closing a Business.”

- Goosmann Law Firm, “How to Minimize Capital Gains Tax for Business Owners.”

- Beinhaker Law, “How to Sell or Transfer Ownership of a Small Business in New Jersey and New York.”

- Smolin CPAs, “Tax Considerations When You Decide to Close a Business.”

- First Citizens Wealth, “Top Year-End Tax Strategies for High Earners.”

- Stature Legal, “Sell Your Business.”

- James P.

Manahan, Esq., “Business Dissolution Attorney Lawrenceville, NJ.”

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.