Quick Summary

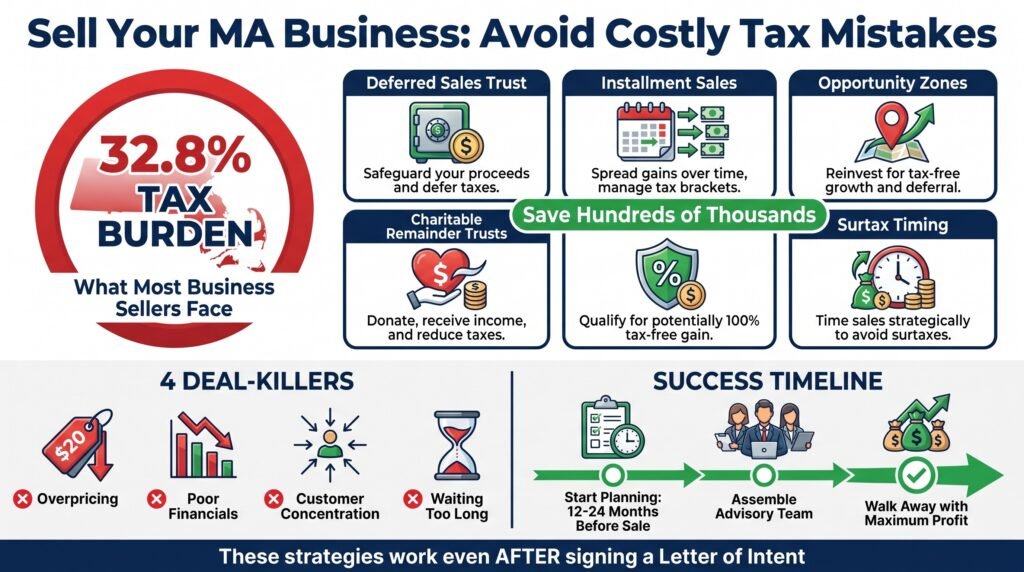

Massachusetts business sellers can face a combined tax burden of up to 32.8%, but most don’t know that legitimate tax-reduction strategies are still available after signing a Letter of Intent.

This article covers six IRS-recognized approaches (Deferred Sales Trust, installment sales, Opportunity Zone investing, Charitable Remainder Trusts, QSBS exclusion, and surtax timing) that can save sellers hundreds of thousands of dollars.

It also highlights the most common deal-killing mistakes, overpricing, poor financials, customer concentration, and waiting too long to plan, and explains why starting 12–24 months out with the right advisory team is the key to walking away with the most money.

Table of Contents

- Quick Summary

- 6 Tax Strategies to Use After You Sign the Letter of Intent

- Common Mistakes That Kill Massachusetts Business Sales

- Your Exit Strategy Determines How Much You Walk Away With

- How to Prepare Your Business for Sale: Start 2 Years Out

- Frequently Asked Questions

6 Tax Strategies to Use After You Sign the Letter of Intent

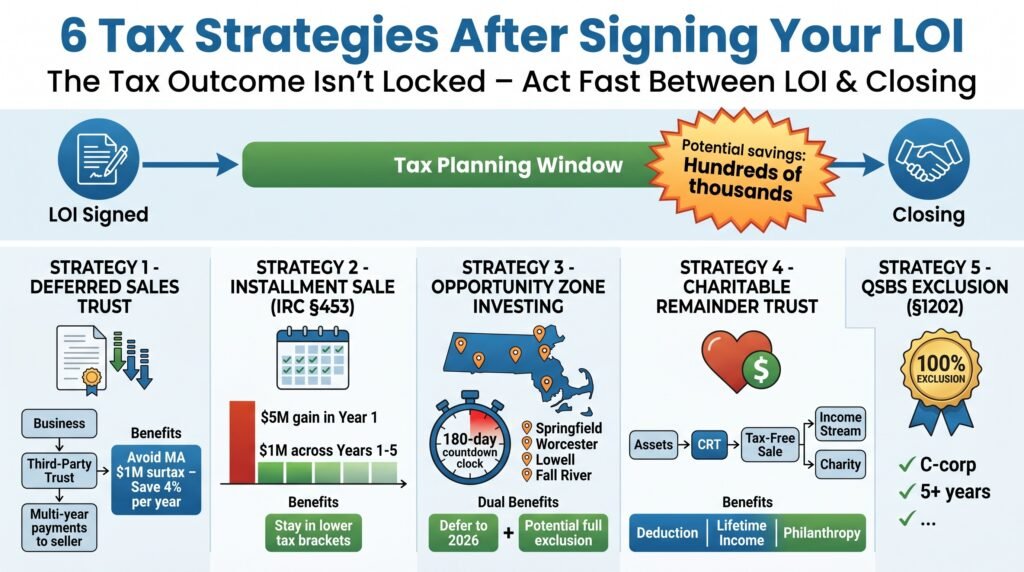

Most business owners assume that once the Letter of Intent is signed, the tax outcome is locked in. It isn’t. There are still legitimate, IRS-recognized strategies available after the LOI stage that can substantially reduce what you owe, sometimes by hundreds of thousands of dollars.

The key is acting quickly and working with the right advisors. Some of these strategies require structural decisions or trust formations that take time to implement, and the window between LOI and closing is often shorter than sellers expect. Here are six strategies that Massachusetts business owners should know about before the ink dries.

1. Deferred Sales Trust: Spread the Tax Burden Over Time

A Deferred Sales Trust (DST) allows you to sell your business to a trust, which then pays you in installments over time rather than in a single lump sum. Because you receive proceeds gradually, you recognize capital gains only as payments arrive, not all at once in the year of sale. This is particularly powerful in Massachusetts because it can keep your annual income below the $1 million surtax threshold each year, potentially saving you 4% on every dollar that would have otherwise crossed that line.

The trust is established by a third-party trustee and must be structured carefully to meet IRS requirements. When done correctly, it is a fully legal tax-deferral strategy, not a tax dodge. The difference between deferring and dodging matters enormously, both legally and practically.

2. Installment Sales Under IRC §453: Defer Gains Across Tax Years

An installment sale under Internal Revenue Code Section 453 lets you receive sale proceeds over multiple years and report gains proportionally as payments come in. This is one of the most straightforward and commonly used strategies for business sellers who want to reduce the immediate tax hit. By spreading a $5 million gain across five tax years instead of recognizing it all in year one, you may avoid the Massachusetts surtax entirely in subsequent years, and stay in lower federal capital gains brackets as well.

3. Opportunity Zone Investing: Defer and Reduce Capital Gains

If you reinvest your capital gains from the business sale into a Qualified Opportunity Zone Fund within 180 days of closing, you can defer recognition of those gains until the earlier of the fund sale date or December 31, 2026. Massachusetts has designated Opportunity Zones primarily in Gateway Cities including Springfield, Worcester, Lowell, and Fall River, giving Massachusetts sellers access to local reinvestment options. In addition to deferral, gains on the Opportunity Zone investment itself may be partially or fully excluded from tax if held long enough, making this a dual-benefit strategy.

4. Charitable Remainder Trust: Give to Charity, Keep an Income Stream

A Charitable Remainder Trust (CRT) allows you to transfer appreciated business assets into a trust before the sale closes. The trust sells the business tax-free, reinvests the full proceeds, and then pays you, or another named beneficiary, an income stream for a set number of years or for life. At the end of the trust term, the remaining assets pass to a designated charity.

The immediate benefit is a partial charitable deduction in the year of the sale. The longer-term benefit is that you receive a lifetime income stream from a larger asset base than if you had paid taxes upfront. For business owners with philanthropic intentions, a CRT can simultaneously reduce tax liability, provide retirement income, and support causes they care about, a genuinely powerful combination.

5. Qualified Small Business Stock Exclusion: Up to 100% Federal Tax Exclusion

Under IRC Section 1202, shareholders who hold Qualified Small Business Stock (QSBS) for more than five years may be able to exclude up to 100% of their federal capital gains from the sale, up to $10 million or 10 times the original investment, whichever is greater. To qualify, the business must be a C-corporation with gross assets under $50 million at the time the stock was issued, and it must operate in an eligible industry (most service-based businesses do not qualify, but tech, manufacturing, and certain other sectors do).

This exclusion does not apply at the Massachusetts state level, the Commonwealth does not conform to Section 1202. But eliminating the federal capital gains tax entirely on a qualifying transaction is significant enough to warrant serious evaluation, especially for founders of early-stage companies who are now approaching an exit.

6. Timing the Close Around Massachusetts’ $1 Million Surtax Threshold

If your projected sale proceeds, combined with your other income for the year, are going to push you above $1 million in Massachusetts taxable income, the timing of your closing date is a genuine tax lever. By negotiating a closing that falls in a tax year where your other income is lower, or by structuring the deal as an installment sale that deliberately manages annual income levels, you may be able to reduce or entirely avoid the 4% surtax on amounts above the threshold.

This isn’t about gaming the system, it’s about understanding how Massachusetts tax law works and making informed structural decisions before the deal is done. The surtax is based on annual income, not the total sale price, so spreading recognition across years is a completely legitimate planning approach.

Example: A Massachusetts business owner sells for $3 million in total proceeds, generating $2.2 million in capital gains. If all gains are recognized in one tax year and their other income is $150,000, approximately $1.35 millions of those gains exceed the $1 million threshold, triggering roughly $54,000 in additional surtax. Structuring the same deal as a three-year installment sale at $733,000 per year could keep annual income below $1 million entirely, potentially eliminating the surtax and saving over $50,000 in Massachusetts taxes alone.

Common Mistakes That Kill Massachusetts Business Sales

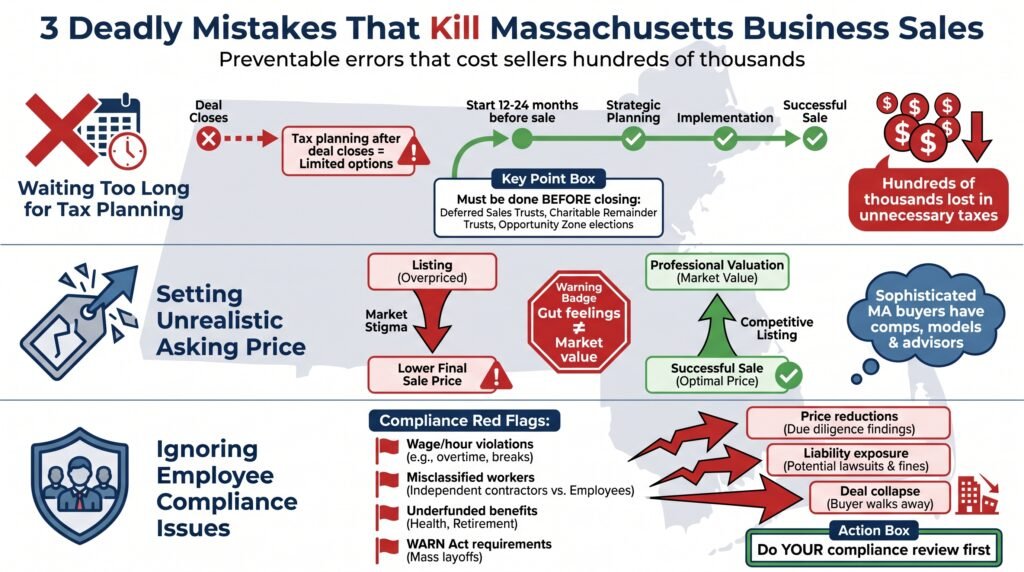

Most failed or underperforming business sales come down to the same preventable mistakes. Knowing what they are, before you’re in the middle of a transaction, gives you a meaningful advantage over sellers who learn these lessons the hard way.

Waiting Too Long to Start Tax Planning

The single most expensive mistake Massachusetts business sellers make is treating tax strategy as something to figure out after the deal closes. By then, most of your options are gone. Deferred Sales Trusts, Charitable Remainder Trusts, and Opportunity Zone elections all require structural steps that must happen before or at closing, not after.

If you wait until you’ve signed the purchase agreement to call a tax advisor, you may be writing a check to the Commonwealth for hundreds of thousands of dollars that proper planning could have legally reduced or deferred. Start your tax planning the moment you start thinking seriously about selling, ideally 12 to 24 months out.

Setting an Unrealistic Asking Price

Overpricing your business is one of the most reliable ways to ensure it never sells. Buyers in the Massachusetts market are sophisticated, and the ones worth selling to have access to industry comps, financial modeling tools, and experienced advisors who will quickly identify a price that doesn’t reflect reality.

An overpriced listing sits on the market, accumulates stigma, and often ends up selling for less than it would have if it had been priced correctly from the start. A professional valuation, not your gut feeling or what a competitor reportedly sold for, is the only reliable foundation for a defensible asking price.

Neglecting Employee and Benefits Obligations During the Sale

Massachusetts has some of the strongest employee protection laws in the country, and buyers conducting due diligence will scrutinize your compliance carefully. Outstanding wage and hour issues, misclassified workers, underfunded benefit obligations, or WARN Act notification requirements for larger businesses can all become deal liabilities.

If the buyer discovers these issues before you do, they will either demand price reductions, require indemnification clauses that expose you to future liability, or walk away entirely. Conducting your own employment compliance review before going to market is one of the most overlooked, and most important, steps in the preparation process.

Your Exit Strategy Determines How Much You Walk Away With

The difference between a reactive exit and a planned exit is almost always measured in dollars, significant ones. Business owners who approach their sale as a process rather than an event, who prepare their financials years in advance, who build advisory teams early, and who understand the tax levers available to them consistently walk away with more money, fewer post-closing obligations, and a cleaner transition into whatever comes next. The Massachusetts market is strong, buyer demand is real, and the opportunities for a well-prepared seller are genuine, but they don’t come to sellers who are unprepared.

Whether you’re three years from a potential exit or three months from signing an LOI, the most important step is the next one: get a valuation, talk to a transaction attorney, and start mapping your tax strategy now. Every month of preparation is an investment that pays at closing.

A lot of owners think they can sell their business themselves, especially if they already know a potential buyer. And sure, if you’re doing a small family succession or selling to a trusted employee, maybe you can cobble together a deal without professional help.

But for any arms-length transaction, especially if you’re trying to maximize value, you really need a team.

A business broker or M&A advisor brings market knowledge, valuation expertise, buyer networks, and process discipline. They know what deals are closing at in your industry.

They know how to package your financials and operations to tell a compelling story.

They know how to run a competitive process that creates urgency and drives up price. They act as a buffer between you and the buyer, which keeps emotions out of the negotiation and lets you keep running the business while they manage the process.

The classic adage applies, “If you want to go fast, go alone, if you want to go far, go together”

In addition to being ranked one of the top business brokers in 2025, Earned Exits provides M&A advisory services. The company’s M&A process is intentionally designed to deliver a smooth, well-managed experience from initial planning through closing and beyond. With more than 30 years of combined experience, our team provides hands-on guidance at every stage. Below is an overview of how our process works:

Initial assessment and preparation: We start with a complimentary business valuation, uncover key value drivers, and position your company for a successful sale or acquisition.

Tailored M&A strategy: The company’s experienced advisors craft a customized transaction strategy aligned with your objectives, ensuring each phase is thoughtfully planned and executed.

Targeted buyer outreach: Your business is presented to a select group of qualified buyers and investors through our established network, allowing us to identify the strongest strategic fit.

Negotiation and closing management: We lead negotiations to secure favorable terms that support your goals and manage the process through a successful close.

Post-transaction support: Following the sale, we remain engaged to facilitate a smooth transition, offering guidance on integration, planning, and next steps as needed.

Click the link below if you’re ready to get started right now with Earned Exits free business valuation.

How to Prepare Your Business for Sale: Start 2 Years Out

A well-prepared business sells faster, at a higher price, and with fewer surprises during due diligence. Starting early gives you time to address the red flags buyers will find anyway, but on your terms, not theirs.

- Get 3 years of clean, professionally prepared financial statements

- Separate personal and business expenses completely

- Resolve any outstanding legal disputes or compliance issues

- Diversify your customer base to reduce concentration risk

- Document all systems, processes, and standard operating procedures

- Ensure all intellectual property is formally owned by the business entity

- Review all contracts, leases, and vendor agreements for assignability

None of these items are difficult on their own, but most business owners are too close to their operations to see them objectively. A business broker or M&A advisor can do a pre-sale readiness assessment that identifies exactly where the gaps are, and quantifies what fixing them is worth in dollar terms at closing.

Clean Up Your Financials Before Buyers See Them

Financial due diligence is where deals slow down or die. Buyers and their accountants will scrutinize every line item across at least three years of financial statements, and anything that looks inconsistent or unexplained creates doubt. Doubt leads to lower offers, longer timelines, and sometimes dead deals.

The most important things to have in order before going to market include:

- Three years of tax returns that reconcile cleanly with your P&L statements

- A clear record of all owner add-backs with documentation

- Accounts receivable aging reports that show collectability

- Documented revenue recognition practices, especially for recurring or deferred revenue

- Payroll records and benefit obligations that are current and compliant

If you’ve been using a bookkeeper rather than a CPA, this is the time to upgrade. Buyers pay more for businesses where the numbers are clean, consistent, and easy to verify.

Fix Customer Concentration Before It Kills Your Deal

Customer concentration is one of the most common deal-killers in Massachusetts business sales. If one customer accounts for more than 20% to 25% of your total revenue, most buyers will see that as a significant risk, and price it accordingly with either a lower offer or earn-out provisions that delay when you actually receive your money. Spending 12 to 18 months actively growing your second and third-tier client relationships before going to market can have an outsized impact on your final sale price.

Intellectual Property, Contracts and Leases Buyers Will Scrutinize

Massachusetts buyers, especially those backed by private equity, conduct thorough legal due diligence on every agreement the business has signed. That includes your commercial lease (and whether it can be assigned to a new owner without landlord approval), customer contracts (and whether they contain change-of-control clauses that could terminate them at sale), vendor agreements, and any IP ownership documentation.

Discovering mid-due-diligence that your commercial lease requires landlord consent, and your landlord is unresponsive or demanding rent increases as a condition, can delay or collapse a deal. Identifying and resolving these issues before you go to market keeps you in control of the process.

Why Documented Systems Add Real Dollar Value to Your Sale

A business that runs on the owner’s knowledge alone is a business that buyers are afraid to purchase. If your operations live in your head, how you price jobs, manage key relationships, handle exceptions, train new staff, buyers will either walk away or heavily discount their offer to account for the risk of losing you after closing.

Documented systems tell a buyer that the business can run without you, which is exactly what they need to feel confident writing a large check. Standard operating procedures, employee training manuals, customer onboarding workflows, and even simple process checklists can meaningfully increase your valuation multiple. Think of every documented system as a risk-reduction asset, and buyers pay for risk reduction every time.

Business Seller Sanity Checklist

As we covered in the first part of this series, it’s time for another seller sanity check. Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If your business is valued at $1 to $40 million, an experienced business broker like Earned Exits will leverage more potential buyers and an average increase of profit of 20 to 30% more than going it alone.

The classic adage applies, “If you want to go fast, go alone, If you want to go far, go together”

Stated simply, alone is cheaper, but not always most profitable. Our comprehensive review of Earned Exits business brokers here.

The company has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes real value for owners selling businesses valued $1M–$40M+. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

Learn more about additional Massachusetts tax strategies and more in this article.

Frequently asked questions

What taxes do Massachusetts business sellers pay when they sell their business?

Massachusetts business sellers can face a combined tax burden of up to 32.8%. This includes federal capital gains tax, Massachusetts state income tax, and the Massachusetts Millionaire’s Surtax — an additional 4% on taxable income exceeding $1 million in a given year.

Can I still reduce my tax bill after signing a Letter of Intent?

Yes. Several IRS-recognized tax strategies remain available after the Letter of Intent is signed, including Deferred Sales Trusts, installment sales under IRC §453, Opportunity Zone investing, and Charitable Remainder Trusts. However, some require trust formations or structural decisions that take time, so acting quickly between LOI and closing is critical.

What is a Deferred Sales Trust and how does it work for Massachusetts sellers?

A Deferred Sales Trust (DST) allows you to sell your business to a third-party trust, which then pays you in installments over time. Because gains are recognized only as payments arrive, it can keep your annual income below Massachusetts’ $1 million surtax threshold each year — potentially saving 4% on every dollar that would have otherwise crossed that line.

What is the Massachusetts Millionaire’s Surtax and how does it affect a business sale?

Massachusetts imposes an additional 4% surtax on annual taxable income above $1 million. For business sellers, this means that if your sale proceeds push your total income over $1 million in the year of the sale, every dollar above that threshold is taxed an extra 4%. Structuring the deal as an installment sale or timing the closing strategically can help reduce or eliminate this surtax.

Does the Qualified Small Business Stock (QSBS) exclusion apply in Massachusetts?

The federal QSBS exclusion under IRC Section 1202 can allow eligible shareholders to exclude up to 100% of federal capital gains — up to $10 million — on the sale of qualifying C-corporation stock held for more than five years. However, Massachusetts does not conform to Section 1202, so the exclusion does not apply at the state level. Sellers should consult a qualified CPA before relying on this strategy.

What are the most common mistakes that hurt Massachusetts business sales?

The most common mistakes include: waiting too long to start tax planning (most strategies must be in place before closing), setting an unrealistic asking price, having messy or inconsistent financial statements, relying too heavily on a single customer for revenue, and failing to address employee compliance obligations before going to market.

How far in advance should I start preparing to sell my Massachusetts business?

Ideally, 12 to 24 months before your target sale date. This gives you time to clean up financials, reduce customer concentration, document business systems, resolve legal or compliance issues, and implement tax strategies that require advance planning — all of which can significantly increase your final sale price.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

References and Sources

Percy Law Group, PC. Buying or Selling a Small Business in Massachusetts: What You Need to Know. Published April 30, 2025. Available at: www.percylawgroup.com. Percy Law Group is a Massachusetts-based full-service legal team specializing in business transactions, mergers and acquisitions, and exit planning for small business owners across the Commonwealth.

Berkshire Money Management. Selling Your Massachusetts Business? 6 Last-Minute Tax Strategies to Keep More of the Sale Proceeds. Available at: berkshiremm.com. This source provided the foundational framework for the six post-LOI tax strategies discussed in this article, including the Deferred Sales Trust, installment sale structures, Opportunity Zone investing, and the mechanics of Massachusetts’ Millionaire’s Surtax as applied to business sale proceeds.

Berkshire Money Management. Exit Without Regret: When Is the Right Time to Sell Your Business? Published January 2, 2026. Available at: berkshiremm.com. This article provided perspective on exit timing, the psychological and financial dimensions of business owner readiness, and the market conditions that influence sale outcomes for Massachusetts business owners.

Internal Revenue Service. IRC Section 453 – Installment Method. IRC Section 1202 – Qualified Small Business Stock Exclusion. These federal tax code provisions govern installment sale treatment and the QSBS exclusion discussed in the tax strategy section. Massachusetts does not conform to IRC Section 1202 for state tax purposes; sellers should verify current federal and state conformity with a qualified CPA before implementing any tax strategy discussed in this article.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.