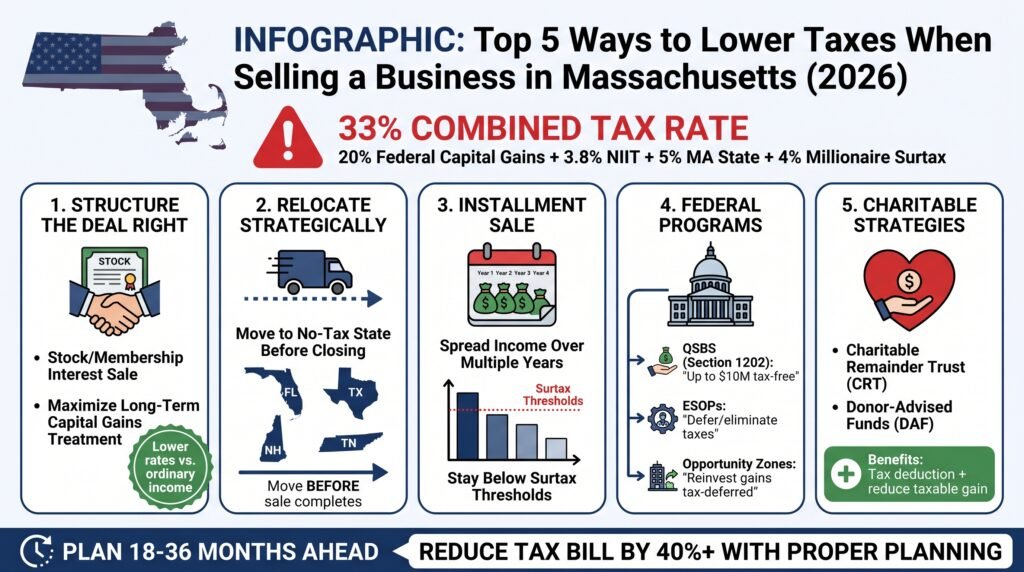

Quick Summary

Massachusetts business sellers can face a combined tax rate of nearly 33% (federal capital gains + 3.8% NIIT + 5% state rate + 4% millionaire surtax). The five key strategies to reduce that burden are: (1) structuring the deal as a stock/membership interest sale to maximize long-term capital gains treatment; (2) relocating to a no-tax state before closing; (3) using installment sales to spread income across multiple years and stay below surtax thresholds; (4) leveraging federal programs like QSBS (Section 1202), ESOPs, or Opportunity Zone funds; and (5) integrating charitable tools like Charitable Remainder Trusts or Donor-Advised Funds before the sale. Planning 18–36 months ahead can reduce your total tax bill by 40% or more.

Table of Contents

- Quick Summary

- Smart tax strategies can save you hundreds of thousands when you exit your Massachusetts business.

- 1. Structure the Deal to Favor Long-Term Capital Gains (INFO)

- 2. Time Your Residency: Sell Before or After Leaving Massachusetts

- 3. Use Installment Sales and Timing to Spread the Tax Hit

- 4. Leverage Special Federal Rules: QSBS, ESOPs, and Opportunity Zones

- 5. Integrate Charitable and Estate Planning Before the Sale

- Conclusion: Choosing Your Best Path Forward

- Assembling a Professional Exit Team to Maximize Profits and Avoid Unnecessary Losses

- Frequently Asked Questions

Smart tax strategies can save you hundreds of thousands when you exit your Massachusetts business.

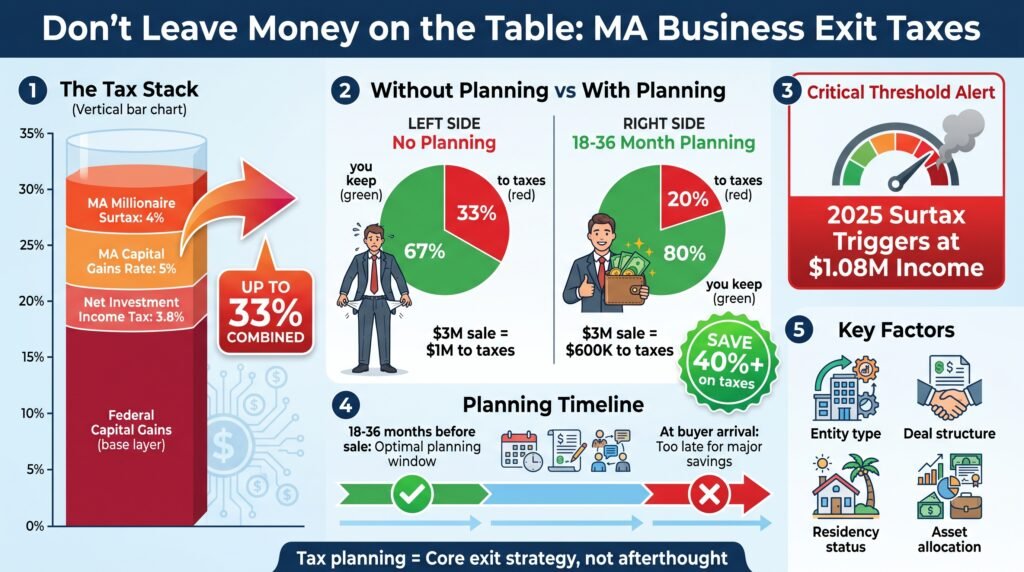

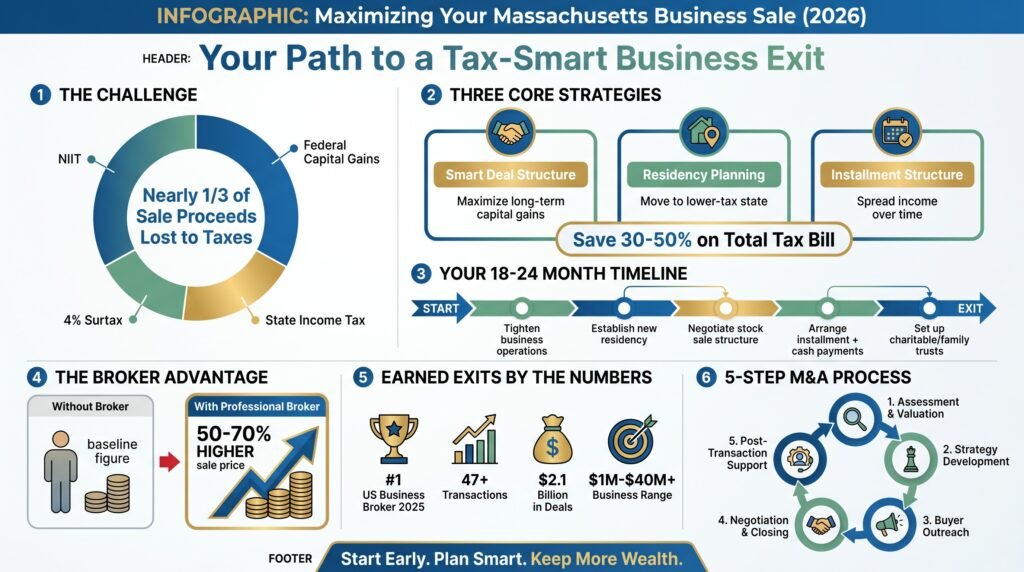

If you sell your business in Massachusetts without advance planning, you will more likely hand over close to one-third of your sale proceeds to federal and state taxes instead of keeping that wealth for retirement or your next chapter.

This matters because Massachusetts now stacks a 4% millionaire surtax on top of its regular 5% capital gains rate, and when you add federal taxes plus the 3.8% Net Investment Income Tax, a large business exit can trigger a combined tax rate approaching 33% on your gains.

In 2025, the surtax threshold sits at roughly $1.08 million of income, so moderate-sized exits hit it fast.

Interestingly, when you plan 18 to 36 months ahead, you can often cut your total tax bill by 40% or more.

But it’s much harder to create meaningful savings if you wait until a buyer shows up.

So, it’s really important to map out your exit strategy early, especially when you are dealing with both state and federal rules that treat different parts of a sale in completely different ways.

Also, don’t forget that where you live for tax purposes in the year you close can be just as important as the sale price itself.

To keep the maximum amount of wealth from your business sale, you should treat tax planning as a core part of your exit process, not an afterthought.

Of course, your specific tax outcome depends on entity type, deal structure, your residency status, and how the purchase price gets allocated across different asset classes.

Below are the five most effective ways to lower your taxes when selling a business in Massachusetts in 2026. These strategies work for both small Main Street businesses and larger closely held companies.

1. Structure the Deal to Favor Long-Term Capital Gains

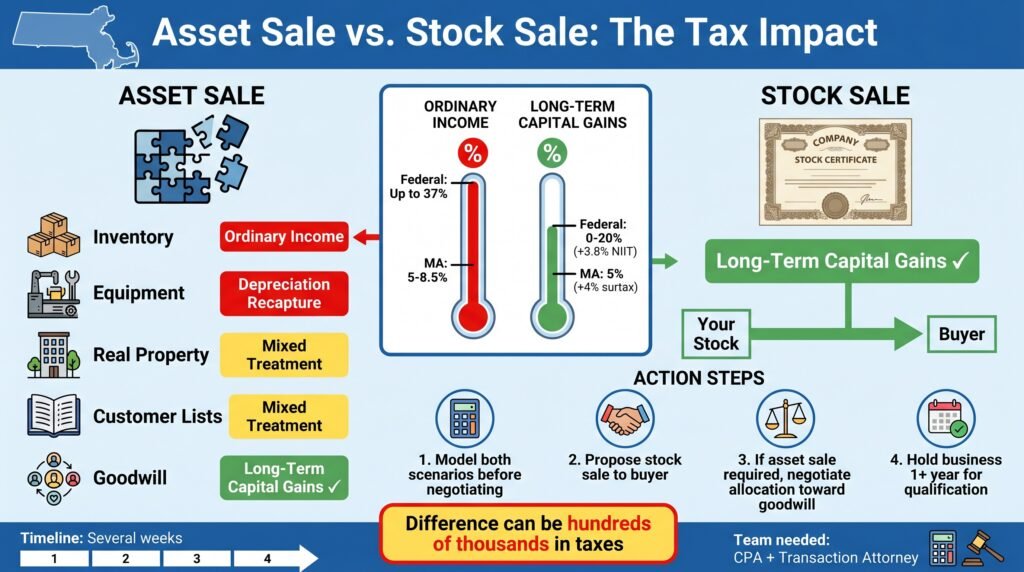

The way you structure your sale determines how much you pay in taxes, often more than the actual purchase price does. Massachusetts follows federal tax concepts, which means the difference between an asset sale and a stock sale can shift your tax bill by tens or even hundreds of thousands of dollars.

Asset sale versus stock sale

In an asset sale, the buyer purchases person assets like inventory, equipment, real property, customer lists, trademarks, and goodwill. The purchase price gets allocated across these different categories, and each category faces different tax treatment.

Inventory is taxed as ordinary income.

Depreciation recapture on equipment also gets hit with higher ordinary rates. Only certain parts, like goodwill and capital assets, qualify for long-term capital gains treatment.

In a stock sale or membership interest sale, you sell your ownership interest in the company as a single transaction. This usually produces one large capital gain equal to your sale price minus your basis in the stock.

If you have owned the business for more than one year, that gain qualifies as long-term capital gain at the federal level.

Why this saves money

Long-term federal capital gains rates run 0%, 15%, or 20% depending on your income, plus possibly 3.8% NIIT. Massachusetts taxes most long-term gains at 5%, plus the 4% surtax above the threshold.

Ordinary income gets taxed at much higher federal rates (up to 37%) and at 5% to 8.5% in Massachusetts, and it still counts toward the surtax.

Total time: Several weeks to negotiate and document the structure.

How easy to start: Requires coordination with your buyer and tax advisors, but the payoff is often massive.

What you need: A transaction attorney, a good CPA, and willingness to negotiate allocation terms with the buyer.

How to do it:

Work with your advisors to model both an asset sale and a stock sale before you enter negotiations. Show your buyer how much you need in after-tax proceeds and propose a stock sale if possible.

If the buyer insists on an asset sale, negotiate the allocation so more value goes to goodwill and long-term capital assets instead of inventory or heavily depreciated equipment.

Sometimes offering a slightly lower price in exchange for better allocation can increase your take-home amount. Make sure you have held your business for more than one year to qualify for long-term capital gains rates.

2. Time Your Residency: Sell Before or After Leaving Massachusetts

Where you live when you sell your business can be the single largest tax decision you make. Massachusetts taxes residents on all income, no matter where it comes from.

The state also applies a 5% rate to most long-term capital gains and stacks the 4% surtax on top of income above roughly $1.08 million.

On a $10 million sale, that means Massachusetts alone could take close to 9% of your gain if you stay a resident. More business owners are choosing to establish residency in states like Florida, Texas, or Nevada before closing a sale, especially when they plan to relocate anyway.

Why this saves money

Moving to a no-tax state before you sell can eliminate most or all state tax on intangible assets like stock gains, depending on how the transaction is structured and what residency you can prove. Even if you are selling a business that operates in Massachusetts, gain from selling stock or membership interests may not be sourced to Massachusetts if you are a nonresident at the time of sale.

The rules are complex, but the savings can run into seven figures for large exits.

Total time: Plan to move at least 18 months before your anticipated sale date.

How easy to start: Requires a genuine relocation, not just a change of address. You need to spend more than half the year in the new state, move your home and key ties, and document everything carefully.

What you need: A relocation plan, legal and tax advisors who understand multi-state sourcing rules, and the flexibility to move before signing any binding sale agreement.

How to do it:

Decide whether to sell your business before moving or move first and then sell. If you stay in Massachusetts during the sale year, expect to pay the full 5% plus surtax.

If you move to a no-tax state and establish real residency before signing a letter of intent, you can often avoid most state tax on stock or membership interest sales.

Start by moving your home, drivers license, voter registration, and primary relationships to the new state. Spend the majority of your time there.

Work with advisors to create a residency timeline and documentation trail.

Close the sale only after you have clearly established nonresident status. This strategy ties directly into broader wealth and tax migration trends and is central to many business exit strategy relocation plans.

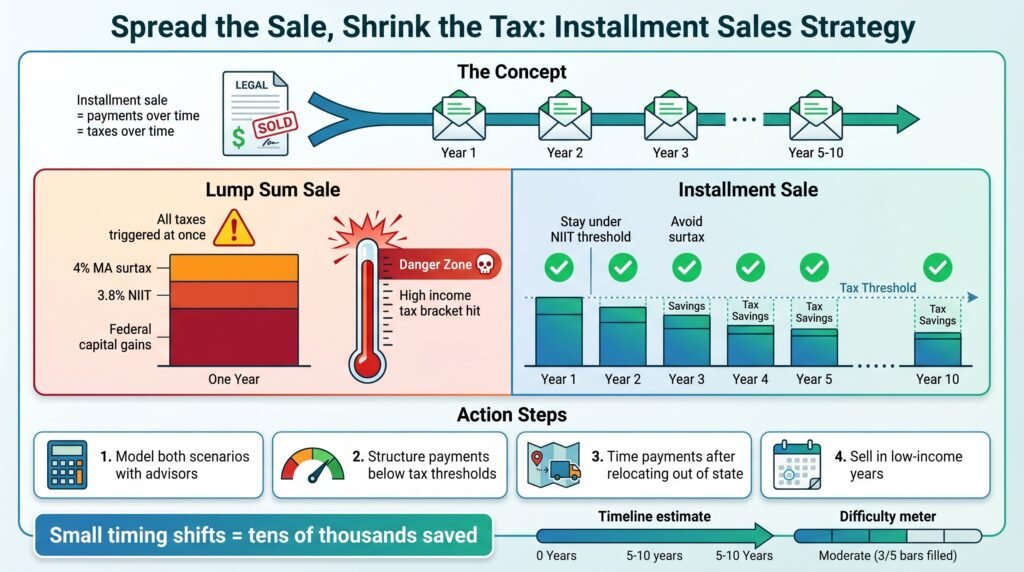

3. Use Installment Sales and Timing to Spread the Tax Hit

An installment sale lets you receive part of the purchase price over time through seller financing, earn-outs, or deferred payments. Under federal and Massachusetts rules, you usually recognize gain as you receive payments instead of all in the year of closing, as long as at least one payment arrives after the year of sale.

Why this saves money

Spreading gain over many years keeps you in lower federal capital gains brackets each year. It can also reduce or eliminate the 3.8% federal Net Investment Income Tax and the Massachusetts 4% surtax, both of which only apply above certain income thresholds.

Instead of one very high-income year that triggers every possible tax, you engineer steadier income that avoids the top brackets.

Total time: Depends on the payment schedule, often five to ten years.

How easy to start: Relatively straightforward if the buyer is creditworthy and willing to pay over time, and if you can afford to wait for full payment.

What you need: A solid buyer with good credit, legal documents for the note or earn-out, and willingness to accept payment risk in exchange for tax savings.

How to do it:

Ask your advisors to model a lump-sum sale versus an installment structure. Compare the total after-tax proceeds under each scenario, factoring in the time value of money and any interest you will earn on deferred payments.

Negotiate payment terms that keep your annual income below the NIIT and surtax thresholds if possible.

If you plan to move out of state after closing, structure installment payments to arrive after you become a nonresident, which may reduce state tax on those later payments depending on sourcing rules. You can also apply simple timing by selling in a year when other income is lower, such as after you stop taking a salary or before you start large retirement distributions.

Small timing decisions can shift tens of thousands of dollars in combined tax.

4. Leverage Special Federal Rules: QSBS, ESOPs, and Opportunity Zones

Federal law offers three powerful tools that can dramatically cut your tax bill, but all three need advance planning and specific structures.

Qualified Small Business Stock (QSBS) under Section 1202

If your company is a C corporation and meets certain criteria, your stock may qualify as QSBS. The corporation’s gross assets must not exceed $50 million when the stock is issued. You must hold the stock for at least five years.

If you meet all requirements, you can potentially exclude up to 100% of your gain from federal income tax, up to the greater of $10 million or ten times your basis in the stock.

Recent planning discussions refer to legislative changes that may increase the exclusion cap for stock acquired after 2025. This does not automatically eliminate Massachusetts tax, but removing the federal piece cuts your largest tax burden.

Employee Stock Ownership Plans (ESOPs)

C corporations can sell stock to an ESOP, which is a trust that holds stock for the benefit of employees. If the structure qualifies under Section 1042, you may be able to defer federal capital gains by rolling sale proceeds into qualified replacement securities.

Owners who want to reward employees and keep the company independent sometimes choose ESOPs as part of their exit strategy.

Qualified Opportunity Zone (QOZ) Funds

If you realize a large capital gain from selling your business, you can invest part or all of that gain into a Qualified Opportunity Zone Fund within 180 days. You defer tax on the reinvested gain until December 31, 2026, or earlier if you sell the fund interest.

If you hold the QOZ investment for at least ten years, you may permanently exclude any appreciation on the QOZ investment itself.

The deferral period now ends in late 2026, but the ability to avoid tax on future QOZ gains still makes the program attractive for some exits.

Total time: QSBS needs a five-year hold. ESOP and QOZ structures can move faster but still need months of planning.

How easy to start: All three are complex and need specialized advisors.

What you need: For QSBS, a C corporation that qualifies and five years of patience. For ESOPs, a C corporation and employees you want to benefit.

For QOZ, liquid proceeds to invest within 180 days and a risk tolerance for opportunity zone investments.

How to do it:

Review whether your corporation can be restructured to qualify for QSBS years before your sale. If you already have a C corporation, explore whether selling to an ESOP aligns with your goals.

If you expect a large taxable gain and cannot use QSBS or an ESOP, consider rolling a portion of your proceeds into a QOZ fund.

Model the tax savings under each scenario and compare them against the restrictions and risks involved.

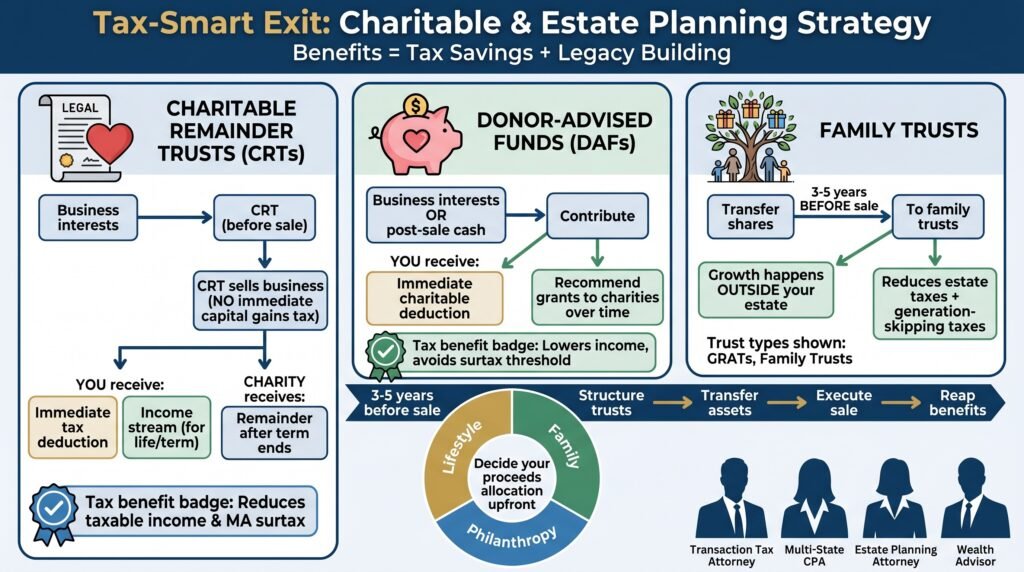

5. Integrate Charitable and Estate Planning Before the Sale

Combining charitable giving and estate planning with your business exit can produce both tax savings and legacy benefits. Charitable Remainder Trusts and Donor-Advised Funds are the two most common tools.

Charitable Remainder Trusts (CRTs)

You transfer business interests into a CRT before the sale. The CRT sells the business without immediate capital gains tax at the trust level.

You receive an immediate charitable income tax deduction based on the present value of the remainder that will eventually go to charity.

The CRT pays you and possibly your spouse an income stream for a term of years or life, and you pay tax only as you receive distributions. This reduces your taxable income in the year of sale and can lessen the impact of the Massachusetts surtax.

Donor-Advised Funds (DAFs)

You contribute appreciated business interests or post-sale cash to a DAF. You get a charitable deduction in the year of contribution and can recommend grants to charities over time.

This lowers your overall taxable income and may keep you closer to the surtax threshold.

Family trusts and wealth transfer

Setting up family trusts, Grantor Retained Annuity Trusts, or other estate vehicles before you sell moves some shares out of your estate. Any growth after the transfer happens outside your estate and reduces future estate and generation-skipping transfer taxes.

Total time: Start three to five years before a potential sale to allow time for holding periods, restructuring, and trust funding.

How easy to start: Requires a coordinated team of advisors and careful planning, but can save enormous amounts of tax and create a lasting legacy.

What you need: Transaction tax attorney, CPA with multi-state experience, estate planning attorney, and wealth advisor who can model scenarios.

How to do it:

Decide in advance how much of your sale proceeds you want for lifestyle, how much for family, and how much for philanthropy. Work with your estate planning attorney to set up a CRT or fund a DAF before the sale.

To benefit family members, transfer some shares into trusts years before the sale so growth happens outside your estate.

Coordinate all planning with your transaction advisors so charitable deductions and trust structures align with your sale timeline and deal structure.

Conclusion: Choosing Your Best Path Forward

Selling your business in Massachusetts in 2026 means facing a tax system that can claim almost one-third of your sale proceeds when you add federal capital gains, NIIT, state income tax, and the 4% surtax. The good news is you have more tools than ever to manage those taxes if you plan ahead.

For most owners, the combination of smart deal structure that maximizes long-term capital gains, residency planning that considers a move before the sale, and a reasonable installment structure to spread income over time delivers the largest share of savings with manageable complexity. These three strategies alone can often cut your total tax bill by 30% to 50% compared to doing nothing.

An owner who plans ahead might tighten up the business for sale over 18 to 24 months, move to a lower-tax state and establish genuine residency, negotiate a stock sale that produces mostly long-term capital gains, take part of the price in installments and part in cash, and set aside a portion of equity or proceeds in a charitable or family trust.

This kind of plan directly addresses tax and wealth flight concerns and gives you control over where you live, how you spend your time, and what your money supports after the sale.

If you want one clear next step, start early. Begin by mapping your goals, then sit down with a tax-savvy CPA and transaction attorney who understand both Massachusetts rules and multi-state planning.

The sooner you treat your business exit as a multi-year project instead of a one-time event, the more control you gain over the outcome and the more wealth you keep.

Assembling a Professional Exit Team to Maximize Profits and Avoid Unnecessary Losses

Past the state-specific planning, an experienced business broker and M&A Advisor can help you maximize a profitable exit far beyond selling your business independently.

Business Broker: Works on success fee (8–12%). Focuses on Main Street and lower middle market buyers. Top business brokers maintain extensive networks of qualified, motivated buyers seeking specific acquisition opportunities. Top business brokers maintain extensive networks of qualified, motivated buyers seeking specific acquisition opportunities.

M&A Advisor: May charge retainer plus success fee. Runs a structured auction or targeted buyer outreach process. Engages private equity, strategic acquirers, and search funds. Provides deal structuring guidance throughout.

Earned Exits has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes outcomes for business owners.

Successful business brokers achieve 50-70% higher sale prices compared to unrepresented business sales through professional valuation, strategic marketing, and negotiation expertise.

The most effective business brokers maintain confidentiality throughout the sales process while connecting sellers with qualified, vetted buyer networks.

Earned Exits has facilitated over 47 successful business transactions worth $2.1 Billion, demonstrating how specialized industry knowledge translates to exceptional results.

Choosing the right broker involves matching your business size ($1M-$40M+) with a firm whose expertise aligns with your specific industry and sale objectives.

Also, Earned Exits provides M&A advisory services. The company’s M&A process is intentionally designed to deliver a smooth, well-managed experience from initial planning through closing and beyond.

With more than 30 years of combined experience, our team provides hands-on guidance at every stage. Below is an overview of how our process works:

Initial assessment and preparation: We start with a complimentary business valuation, uncover key value drivers, and position your company for a successful sale or acquisition.

Tailored M&A strategy: The company’s experienced advisors craft a customized transaction strategy aligned with your objectives, ensuring each phase is thoughtfully planned and executed.

Targeted buyer outreach: Your business is presented to a select group of qualified buyers and investors through our established network, allowing us to identify the strongest strategic fit.

Negotiation and closing management: We lead negotiations to secure favorable terms that support your goals and manage the process through a successful close.

Post-transaction support: Following the sale, we remain engaged to facilitate a smooth transition, offering guidance on integration, planning, and next steps as needed.

Click the link below if you’re ready to get started right now with Earned Exits free business valuation.

Frequently asked questions

How is selling a business in Massachusetts taxed in 2026?

You face federal tax on capital gains at 0%, 15%, or 20% for long-term gains, plus possibly 3.8% Net Investment Income Tax for higher earners. Massachusetts taxes most long-term capital gains at 5%.

The state also applies a 4% surtax on all income, including capital gains, above around $1.08 million.

Short-term gains get taxed at higher federal ordinary rates and at 8.5% in Massachusetts. The combined rate can reach roughly 32.8% for large exits.

Does the Massachusetts Fair Share surtax always apply when I sell my business?

No. Most small business sales produce net gains below $1 million, which means the 4% surtax does not apply at all or applies only to the portion of income above the threshold. If you sell a small business for a modest gain, you may never trigger the surtax.

However, if you are expecting a large liquidity event, you should assume the surtax will matter and plan accordingly.

If I move out of Massachusetts before selling, will I avoid Massachusetts tax completely?

Not always. If you sell stock or membership interests after becoming a bona fide resident of a no-tax state, much of that gain may be taxed only at the federal level, depending on how Massachusetts sources income from intangibles.

If the sale involves assets or real property located in Massachusetts, the state can still tax income sourced there even if you have moved. The key is to plan well in advance, establish real residency elsewhere, and coordinate the deal structure to control which parts are treated as Massachusetts-source income.

What are the main legal requirements for selling a business in Massachusetts from a tax perspective?

You need to file appropriate final income tax returns for the business entity and for yourself as an owner. Make sure sales and use tax obligations are current and file final returns with the Massachusetts Department of Revenue if applicable.

Recognize and report capital gains on your personal return, along with any ordinary income portions of the sale.

Comply with any Massachusetts business tax credit recapture rules if you benefited from credits that need continued operations. Beyond taxes, you need to update corporate records, file changes with the Secretary of the Commonwealth, and handle licenses and allows.

If you are further along in the process, read our more in-depth article for successful business exit planning when selling your Massachusetts business here.

Discover how the Earned Exits’ proven 10-step process can help you achieve the maximum value for your business while ensuring a smooth transition to your next chapter. Click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

References and Sources

- Edelman Financial Engines, “Understanding Capital Gains Tax in Massachusetts.”

- Berkshire Money Management, “Selling Your Massachusetts Business? 6 Last-Minute Tax Strategies to Keep More Sale Proceeds.”

- Seder & Chandler, “Massachusetts Tax Implications of Selling Your Business.”

- U.S. Small Business Administration, “7 Tax Strategies to Consider When Selling a Business.”

- Brighton Jones, “Exit Planning Tax Strategies: Maximizing Your Business Sale.”

- ES Tax, “Tax Exit Strategies: Navigating Transitions with Financial Efficiency.”

- MGO CPA, “Tax Planning Strategies for Your Business Exit.”

- Madras Accountancy, “Exit Planning Tax Strategies: Maximizing After-Tax Wealth.”

- Kahn, Litwin, Renza & Co., “How to Avoid or Defer Capital Gains Tax on a Business Sale.”

- Commonwealth of Massachusetts, “Sales and Use Tax” and “Sales and Use Tax for Businesses.”

- MassBudget, “Very Few Small Businesses Sell for More Than $1 Million.”

- Inland Investments, “Small Business Exit Strategies for Tax Efficiency.”

- U.S. Bank, “Tax Implications of Selling a Business.”

- Goldman Sachs, “Key Tax Considerations When Exiting a Business.”

- Commons LLC, “How to Minimize Capital Gains Tax on a Business Sale in 2026.”

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.