Quick Summary

- Start your exit planning 12 to 18 months before your target closing date, New York’s tax and legal complexity means rushed sales leave serious money on the table.

- New York’s combined state, city, and federal tax burden on business sale proceeds can exceed 40 percent, without a proactive strategy, taxes become the largest single cost of your exit.

- Asset sales and stock sales are taxed very differently, the structure of your deal has a direct and significant impact on what you walk away with.

- Business valuation in New York depends heavily on industry, cash flow, and how well you’ve prepared your financials, sellers who clean up their books before listing consistently achieve higher multiples.

- There are legal strategies, including installment sales, Opportunity Zone investments, and charitable giving vehicles, that can dramatically reduce your tax bill, but they require advance planning, not last-minute moves.

- Selling your New York business is one of the most financially consequential decisions you’ll ever make, and most owners only do it once.

- That single opportunity is exactly why this guide exists. Whether you’re planning to exit in 12 months or just starting to think about it, the decisions you make now will determine how much of your business’s value you actually keep. Earned Exits business brokers works with New York City business owners navigating exactly this process, and the patterns are clear: sellers who plan ahead win, and sellers who wait pay for it, literally.

New York Business Sales in 2026: What You Need to Know Now

The New York business sale market in 2026 is active, but it rewards prepared sellers and punishes unprepared ones. Buyer expectations have risen, due diligence is more thorough than ever, and the tax environment demands a sophisticated exit strategy before you ever list your business.

Why 2026 Is a Pivotal Year to Sell a New York Business

Federal tax policy remains in flux, and business owners who have been watching and waiting are beginning to move. Potential changes to capital gains tax rates and estate tax exemptions have created real urgency for sellers who want to lock in current rates before the legislative landscape shifts.

New York City’s economy has continued its post-pandemic recovery, with buyer demand particularly strong in sectors like professional services, healthcare, food and beverage, and technology-enabled businesses. Multiples in many of these categories remain favorable for sellers who bring clean financials and documented cash flow to the table.

Federal capital gains policy uncertainty is pushing prepared sellers to act sooner rather than later

Buyer activity is elevated across most New York City business categories in 2026

Interest rate stabilization has improved deal financing conditions for qualified buyers

Baby Boomer business owners continue to drive a surge in listings, creating competitive pressure to differentiate.

The Real Cost of Waiting: Tax Exposure Without a Plan

This is the single most important thing to understand before entering the market: tax planning for a California business sale must be done in advance. Once escrow closes, the transaction is set in stone. There is no restructuring after the fact, no going back to allocate proceeds differently, and no opportunity to implement deferral strategies retroactively.

Every month you delay exit planning in New York is a month you’re not implementing strategies that could save you hundreds of thousands of dollars. New York State and New York City together impose income taxes that, combined with federal capital gains rates, can push your total tax burden well above 40 percent on sale proceeds. Without a plan in place before closing, there is very little your advisors can do after the fact.

How to Build an Business Exit Strategy That Actually Works

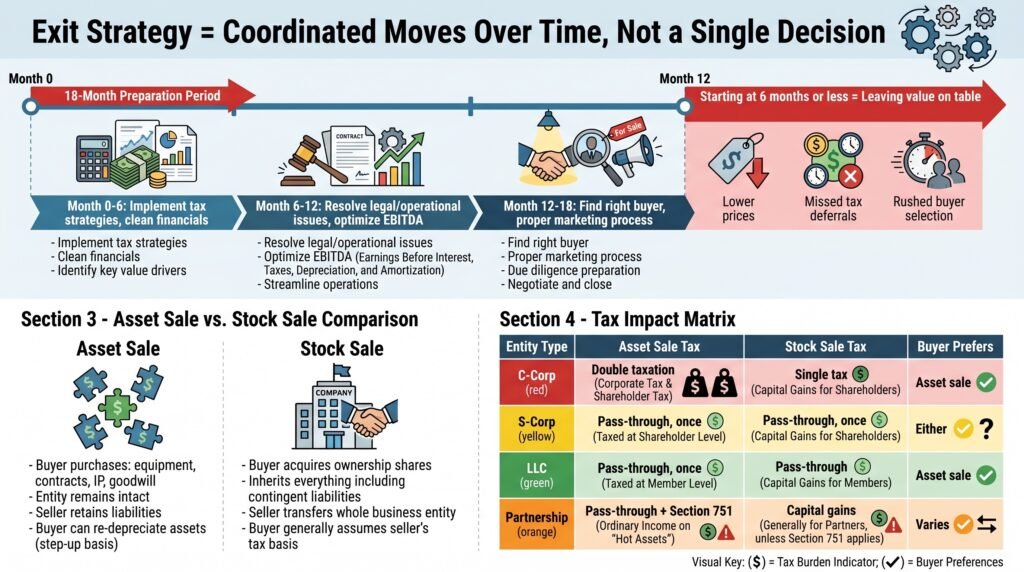

An exit strategy is not a single decision, it’s a coordinated set of moves made over time that maximizes what you walk away with and minimizes what you owe. Most successful New York business exits involve a team of advisors working in parallel, not sequentially.

Start 12 to 18 Months Before You Plan to Close

The 12-to-18-month window before your anticipated close date is not arbitrary. It’s the minimum time needed to implement meaningful tax strategies, clean up your financials, resolve any legal or operational issues that could suppress your valuation, and find the right buyer through a proper marketing process.

Sellers who begin this process late, say, six months out or less, routinely leave value on the table. They accept lower prices because they haven’t had time to optimize EBITDA, they miss out on tax deferral strategies that require advance structuring, and they rush through buyer selection out of time pressure rather than strategic fit.

The allocation negotiation is a leverage point many sellers overlook. Shifting more of the purchase price toward goodwill and intangibles can reduce your federal tax exposure meaningfully, even if California taxes both at ordinary income rates.

Choose the Right Type of Sale: Asset Sale vs. Stock Sale

This is one of the most important structural decisions in any New York business sale, and it is often misunderstood. In an asset sale, the buyer purchases individual assets and liabilities of the business, equipment, contracts, intellectual property, goodwill, rather than the entity itself. In a stock sale, the buyer acquires the actual ownership shares of the company and inherits everything, including contingent liabilities.

How Your Business Structure Affects Your Exit Options

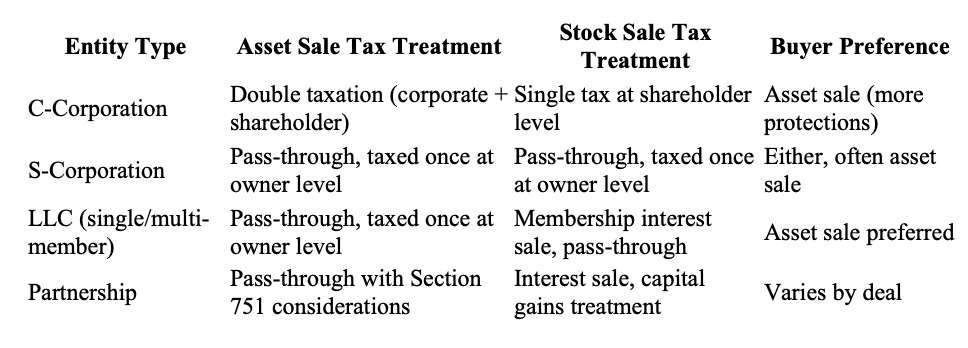

Your business entity type, C-Corp, S-Corp, LLC, or partnership, has a direct impact on how a sale is taxed and which deal structures are even available to you. This is not a minor technicality. It is a fundamental determinant of your net proceeds.

C-Corporation owners face the most challenging tax situation. A stock sale allows them to pay tax once at the shareholder level, but buyers strongly prefer asset sales in C-Corp transactions, which triggers two layers of taxation: once at the corporate level and again when proceeds are distributed to shareholders.

S-Corporation and LLC owners generally have more flexibility. Asset sales in these pass-through entities are taxed only at the individual level, avoiding the double-taxation problem. However, specific rules govern how different asset categories, like goodwill, equipment, and inventory, are taxed, and the allocation of purchase price between asset categories becomes a critical negotiation point. For more insights, check out this guide on business exit planning.

Partnerships follow similar pass-through treatment but introduce additional complexity around Section 751 “hot assets, items like unrealized receivables and inventory that are taxed as ordinary income rather than capital gains, regardless of how the deal is structured.

The Best Time to Sell Your New York Business in 2026

Timing a business sale involves two separate clocks, the market clock and the personal clock. The best outcomes happen when both are aligned.

Market Conditions That Drive Higher Sale Prices

Buyers pay more when they have confidence, confidence in the economy, in financing availability, and in the stability of the business they’re acquiring. In 2026, several market conditions are working in sellers’ favor in New York: financing conditions have improved from the high-rate environment of recent years, and strategic buyers (competitors and industry consolidators) are actively acquiring to grow market share.

That said, market conditions can shift quickly. Sellers who wait for the “perfect” moment often find themselves chasing a market that has already moved. The better approach is to get your business ready now, so that when conditions are favorable, as they currently are, you can move decisively.

Personal Timing: When Your Business Is at Peak Value

Your business is most valuable when revenue and earnings are trending upward, your management team is stable, your customer base is diversified, and your operations don’t depend entirely on you. Selling into a year of declining revenue, even if prior years were strong, gives buyers ammunition to negotiate your price down.

The optimal window to sell is typically two to three years into a sustained growth trend, late enough that the growth is credible and documented, but early enough that the story still has runway left for the buyer.

Sellers who are burned out, dealing with health issues, or facing partnership disputes often feel pressure to exit quickly. This urgency is almost always detected by experienced buyers and used as leverage. If any of these circumstances apply to you, the right move is to get your advisors involved immediately, not to rush to market, but to plan the exit as strategically as your timeline allows.

One metric worth watching closely before listing is your Seller’s Discretionary Earnings (SDE) or EBITDA, earnings before interest, taxes, depreciation, and amortization. These figures form the foundation of most business valuations, and even a modest improvement in trailing twelve-month EBITDA can have a multiplied effect on your final sale price.

How Buyer Demand in New York Affects Your Timeline

New York City attracts a uniquely competitive pool of business buyers, including private equity firms, family offices, strategic acquirers, and individual operators with SBA financing. This depth of demand is an advantage for sellers, but it also means buyers are sophisticated and have seen many deals. They know what a well-prepared business looks like, and they discount aggressively when they encounter one that isn’t.

Buyer demand in New York also varies significantly by industry and borough. Businesses in healthcare services, professional services, and essential trades consistently attract multiple offers. Retail and restaurant businesses require more targeted buyer outreach and benefit most from brokers with sector-specific networks.

New York Business Valuation: What Buyers Are Actually Paying

The Most Common Business Valuation Methods Used in New York

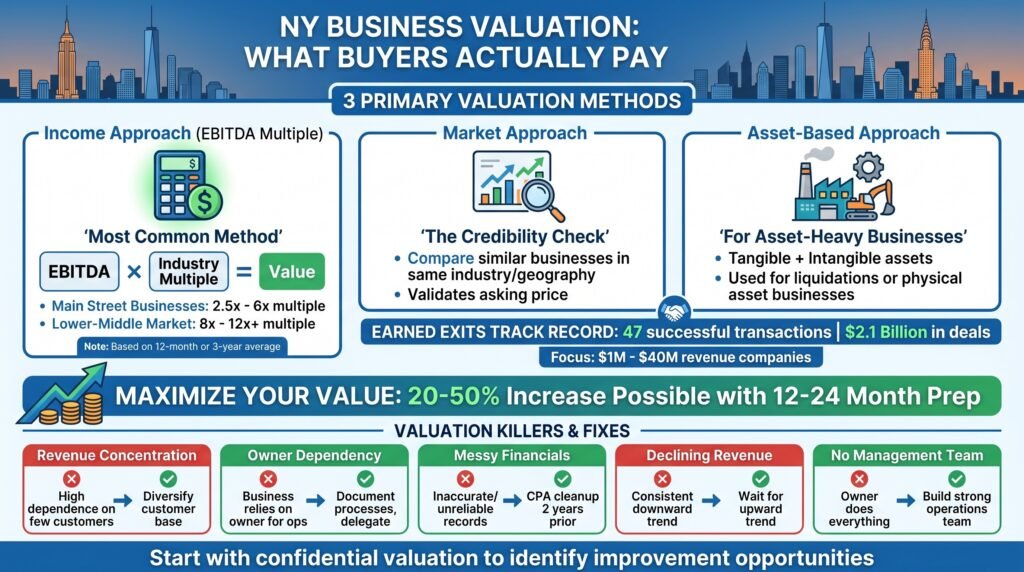

Most New York business sales are valued using one of three primary methods, and the right approach depends heavily on your industry, business size, and the nature of your cash flow. The income approach, specifically the EBITDA multiple method, is the most common for small to mid-sized businesses. A buyer or appraiser calculates your trailing twelve-month or three-year average EBITDA and applies an industry-specific multiple, which in New York typically ranges from 2.5x to 6x for Main Street businesses and can reach 8x to 12x or higher for lower-middle-market companies with strong recurring revenue.

The market approach compares your business to recent sales of similar businesses in the same industry and geography. This is useful for establishing a credibility check on your asking price. The asset-based approach values the business based on the net value of its tangible and intangible assets and is most commonly used for businesses with significant physical assets or those being liquidated rather than sold as going concerns.

Earned Exits has facilitated over 47 successful business transactions worth $2.1 Billion, demonstrating how specialized industry knowledge translates to exceptional results. Earned Exits focuses on brokering company sales with $1 – $40Million in revenue.

This industry-specific knowledge allows them to understand the unique value drivers, customer dynamics, and operational considerations that influence buyer perceptions within each sector.

Starting with a confidential valuation from a reputable firm like Earned Exits provides a baseline understanding of current market value while identifying specific opportunities to increase the valuation before sale.

This preparation phase frequently generates the highest return on investment in the entire exit process, with strategic improvements often increasing final transaction values by 20-50% when implemented 12-24 months before planned exits.

Click the link below if you’re ready to get started right beginning the exit process from your New York business with Earned Exits free business valuation.

What Hurts Your Valuation and How to Fix It Before Listing

There are several common valuation killers that consistently show up in New York business sales, and most of them are fixable with 12 to 18 months of preparation. Revenue concentration is one of the biggest: if a single customer represents more than 20 percent of your revenue, buyers will discount your price to account for that risk.

Start diversifying your customer base before you list. Similarly, owner dependency, where the business’s relationships, operations, or key decisions all run through you, signals fragility to buyers and suppresses your multiple. Document your processes, delegate key relationships, and ensure your management team can operate independently. For more insights on preparing your business for sale, consider exploring business exit planning strategies.

- Messy financials: Inconsistent bookkeeping, commingled personal and business expenses, and missing documentation will trigger price reductions and extended due diligence. Get a CPA to clean and recast your financials at least two years before listing.

- Declining revenue trend: Even one year of revenue decline gives buyers leverage. If you’re in a down cycle, consider waiting until the trend reverses before going to market.

- Undocumented intellectual property or key contracts: Verbal agreements, unsigned client contracts, and informal arrangements have no value in a due diligence process. Convert them to written, assignable contracts.

- Deferred maintenance and capital expenditures: Buyers inspect physical assets and will reduce their offer to account for needed repairs or equipment replacement. Address visible deferred maintenance before your business is shown.

- No management team: A business that collapses without its owner is a high-risk acquisition. Even partial delegation to a strong operations manager significantly improves buyer confidence and valuation.

Business Seller Check-In

Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If you have read enough and know your business has passed the preparation criteria to go to market, read our review of Earned Exits here.

If you have decided that Earned Exits is a good fit and your business size is $1M-$40M+, click the link below to contact Earned Exits today to start their free business valuation by filling out a short form.

In part 2 of this series, we will discuss New York’s tax burden on business sales, tax strategies that reduce what you owe after the sale, and more. Follow this blog for the most up-to-date articles on business selling and profitable exits.

Frequently Asked Questions

Below are the questions New York business owners most commonly ask when they begin thinking seriously about a sale.

When Should I Start Planning to Sell My New York Business?

You should start planning to sell your New York business at least 12 to 18 months before your target closing date, and ideally two to three years in advance if you want maximum flexibility to implement tax strategies, improve your financials, and time the market effectively. The earlier you start, the more options you have and the better your outcome is likely to be.

Sellers who begin planning three or more years out have time to grow EBITDA, reduce owner dependency, diversify their customer base, and implement charitable or deferral strategies that can save hundreds of thousands of dollars in taxes. Those who begin six months out or less are typically forced to accept the business as it is, which almost always means a lower price and a higher tax bill than necessary.

What Taxes Will I Owe When I Sell My Business in New York?

When you sell a business in New York, you will owe federal capital gains tax (up to 20 percent on long-term gains), the 3.8 percent Net Investment Income Tax if your income exceeds the applicable threshold, New York State income tax (up to 10.9 percent depending on income level), and New York City personal income tax (up to 3.876 percent if you are a city resident). Combined, these rates can push your total marginal tax rate on sale proceeds above 40 percent, though proactive planning strategies, including installment sales, Opportunity Zone investments, and charitable vehicles, can significantly reduce your effective rate. Any portion of your proceeds attributed to depreciation recapture will be taxed at ordinary income rates, which are even higher than capital gains rates, making purchase price allocation a critical negotiating point in your deal.

How Is a New York Business Valued Before a Sale?

Most New York businesses are valued using the EBITDA multiple method, your earnings before interest, taxes, depreciation, and amortization are multiplied by an industry-specific figure that reflects what buyers are currently paying for comparable businesses. For Main Street businesses, multiples typically range from 2.5x to 6x EBITDA.

Lower-middle-market companies with strong recurring revenue and scalable operations can achieve 8x to 12x or higher. Your specific multiple is influenced by factors including revenue trend, customer concentration, owner dependency, management team strength, industry dynamics, and the quality of your financial documentation.

Earned Exits has been recognized as the top business broker in the US for 2025, offering a seller-centric approach that maximizes real value for owners selling businesses valued $1M–$40M+. Click the link below to start Earned Exits’ free valuation process by filling out their short form.

References

- BNY Mellon Wealth Management, “Reducing the Tax Impact on the Sale of Your Business”

- SmartAsset, “How to Avoid Capital Gains Tax on a Business Sale”

- Brighton Jones, “Exit Planning Tax Strategies: Maximizing Your Business Sale”

- Richard Brothers Financial Advisors, “Tax Strategies After Business Sale for Maximizing Profits”

- Cummings & Co. Planning, “3 Ways To Reduce The Taxes You Pay When Selling Your Business to a Third Party”

- U.S. Small Business Administration, “7 Tax Strategies to Consider When Selling a Business”

- RBC Wealth Management, “Minimize tax and maximize your business sale”

- EP Wealth Advisors, “How to Manage Taxes When Selling a High-Value Business”

- U.S. Bank, “Tax Implications of Selling a Business”

- Exit Planning Institute, “Certified Exit Planning Advisor Resources”

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.