Quick Summary

Selling a business in California can trigger a combined federal and state tax burden exceeding 50% if you do not plan ahead. California taxes capital gains as ordinary income, making tax strategy one of the most important parts of any business exit.

This guide explains five legitimate ways business owners can potentially reduce or defer taxes before closing a sale:

- Installment sales spread payments over multiple years to reduce tax exposure in any single year.

- Opportunity Zone investments may defer federal capital gains taxes when proceeds are reinvested properly.

- Charitable Remainder Trusts (CRTs) can help defer taxes while creating long-term income and charitable benefits.

- Strategic goodwill allocation may lower federal tax treatment on portions of the sale.

- Proper deal structuring between an asset sale and stock sale can dramatically impact after-tax proceeds.

The article also emphasizes that tax planning must happen before signing the deal. Once the transaction closes, most tax-saving opportunities disappear. Early preparation, clean financials, and professional guidance can significantly increase both valuation and net proceeds from the sale.

Strategic tax planning can save you hundreds of thousands or even millions when you exit your business.

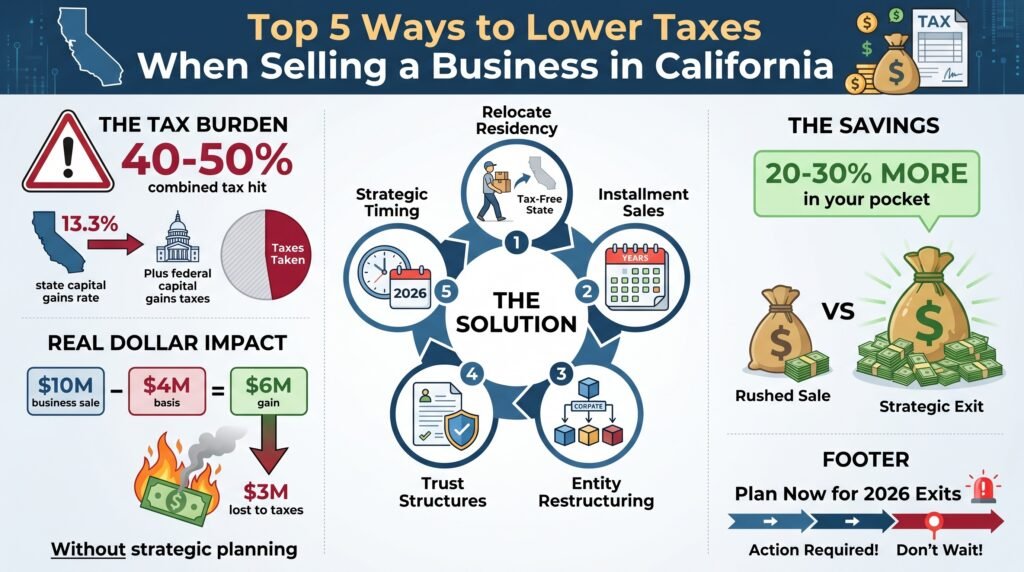

Selling a business in California comes with a significant tax burden. The state’s 13.3% top income tax rate on capital gains, combined with federal capital gains taxes, can consume 40-50% of your sale proceeds. For a business owner selling a company for $10 million with a $4 million basis, that’s potentially $3 million going to taxes instead of your pocket.

The difference between a rushed sale and a strategic exit can mean millions in after-tax proceeds. Business owners who apply tax strategies like establishing residency in no-tax states, using installment sales, or restructuring entities save 20-30% or more compared to those who simply sign on the dotted line. The tactics below range from straightforward relocations to complex trust structures, but each offers substantial savings when executed correctly.

California’s aggressive pursuit of tax revenue amid ongoing wealth migration makes planning more critical than ever for 2026 exits.

5 Strategies to Lower Your Tax Bill

1. Relocate to a No-Tax State Before the Sale

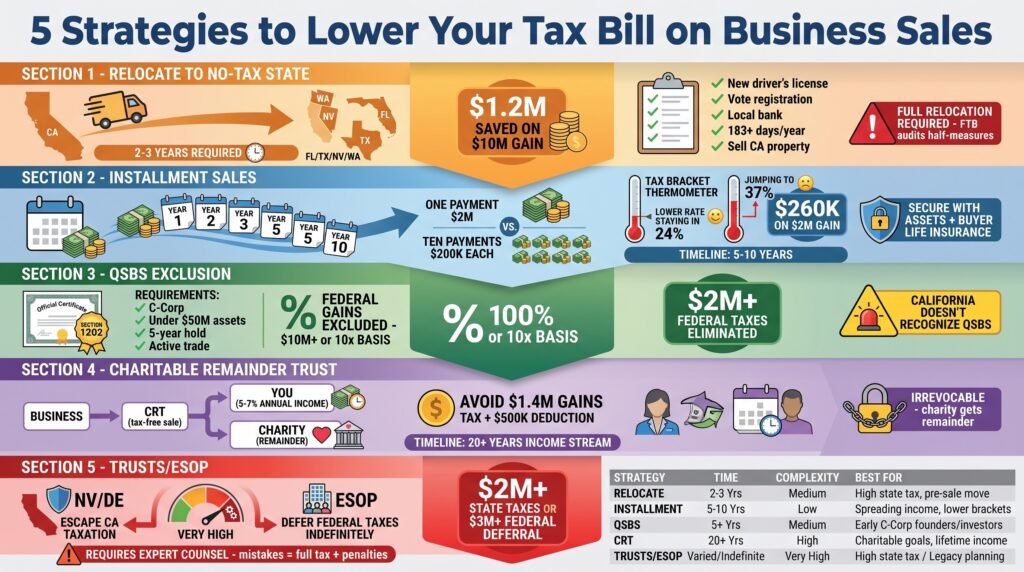

Moving your legal residence to a state with no income tax eliminates California’s 13.3% state tax on your business sale gains. States like Florida, Texas, Nevada, and Washington impose zero state income tax, allowing you to keep the entire state portion of your proceeds.

This strategy needs genuine relocation, not just a mailbox. You need to establish domicile in your new state at least 2-3 years before the sale.

California’s Franchise Tax Board actively audits these moves, looking for evidence you still maintain significant ties to the state.

Time required: 2-3 years least for safe harbor.

Setup complexity: Moderate. You need to physically move, obtain new driver’s license, register to vote, open local bank accounts, and spend more than 183 days per year in the new state.

Potential savings: On a $10 million gain, about $1.2-1.3 million in state taxes.

Best for: Business owners with flexible living situations and sale timelines of 2+ years out.

Watch out for: California will examine your calendar, credit card statements, cell phone records, and property ownership. Maintain detailed records of your days in each state.

Sell any California real estate and close California-based businesses.

Half-measures trigger audits you’ll likely lose.

2. Use Installment Sales to Spread Gains Over Years

An installment sale allows you to receive payments over multiple years as opposed to a lump sum, reporting the taxable gain proportionally as you receive each payment. This keeps you out of the highest tax brackets and can preserve deductions that phase out at high income levels.

Under IRC Section 453, you structure the sale so the buyer pays you over 5-10 years (or longer) with interest. If you sell your business for $8 million with a $2 million gain, you might receive $800,000 annually for 10 years.

Each year, you’d report only $200,000 of gain instead of the full $2 million hitting your taxes in year one.

Time required: Negotiations add a few weeks, tax benefits span the payment period.

Setup complexity: Moderate. Requires buyer agreement, promissory note, and often security interest in business assets.

Potential savings: Staying in the 24% federal bracket versus jumping to 37% could save $260,000 on a $2 million gain.

Best for: Owners selling to buyers who prefer financing, or those wanting steady income in retirement.

Watch out for: Buyer default risk. If they can’t pay, you’ve already reported some gain but might not collect.

Secure the note with assets and consider requiring life insurance on the buyer.

Not available for inventory sales. California still taxes its portion unless you’ve relocated first.

3. Leverage Qualified Small Business Stock (QSBS) Exclusion

Section 1202 of the tax code allows you to exclude up to 100% of federal capital gains on qualified small business stock, with gain exclusions of at least $10 million or 10 times your basis, whichever is greater. This federal benefit can eliminate $2+ million in federal taxes.

Your business must be a C-corporation, have gross assets under $50 million when the stock was issued, and you must hold the stock for at least five years. The business must be an active trade (not real estate, financial services, or other disqualified activities).

Time required: Minimum 5-year hold period from stock issuance.

Setup complexity: Complex. May need converting from S-corp or LLC to C-corp, which triggers immediate tax consequences and needs waiting periods.

Potential savings: Up to $2 million+ in federal taxes on a $10 million gain. California does not conform, so state taxes still apply (unless you relocate).

Best for: Tech startups, software companies, and manufacturing businesses structured as C-corps from inception.

Watch out for: California does not recognize QSBS exclusions, so you’ll still owe the full 13.3% state tax. The 5-year clock starts fresh with new stock issuances.

Converting entity types can trigger built-in gains taxes.

Professional valuation required to prove asset limits at issuance.

4. Set Up a Charitable Remainder Trust (CRT)

A charitable remainder trust let’s you transfer appreciated business assets to an irrevocable trust that sells them tax-free, pays you an income stream for life or a term of years, and ultimately distributes the remainder to charity. You avoid immediate capital gains tax and receive a charitable deduction.

You fund the CRT with your business interest before the sale. The trust, as a 501(c)(3) entity, sells the business without paying capital gains tax.

You receive an annual payment (typically 5-7% of the trust value), which is taxed as received. After your death or the term ends, the remaining assets go to your chosen charity.

Time required: Several months to establish and fund before the sale, benefits last 20+ years.

Setup complexity: High. Requires estate planning attorney, trustee, IRS filing, and careful structuring.

Potential savings: Avoiding $1.4 million in federal gains tax on a $7 million sale, plus immediate charitable deduction worth $500,000+ against other income.

Best for: Business owners with philanthropic goals who want lifetime income and substantial current deductions.

Watch out for: The arrangement is irrevocable. The charity must receive the remainder, so you can’t change your mind.

Minimum annual payout requirements mean smaller trusts generate minimal income.

California partially conforms, providing some state deduction benefits. The income you receive is still taxable, though often at lower rates than a lump sum would be.

5. Restructure into Non-grantor Trusts or Use ESOP for Deferral

Advanced entity restructuring can shift income away from California’s reach or defer federal taxes entirely. Non-grantor trusts established in no-tax states can sell business interests without California taxation, while Employee Stock Ownership Plans (ESOPs) allow C-corp owners to defer federal taxes indefinitely by rolling proceeds into qualified replacement securities.

Non-grantor trusts: You convert your LLC to a partnership and contribute interests to a properly structured trust in a state like Nevada or Delaware. When the trust sells, precedents like Fielding suggest California can’t tax the gain if you’re a nonresident.

This preserves deductions and avoids NIIT (Net Investment Income Tax).

ESOP route: Your C-corp establishes an ESOP that purchases your shares. You sell at least 30% to the ESOP, then roll your proceeds into qualified replacement securities (stocks and bonds of U.S. operating companies).

You defer federal capital gains as long as you hold those securities.

Time required: 3-5 years for trust strategies, 1-2 years for ESOP setup.

Setup complexity: Very high. Requires specialized attorneys, annual filings, and ongoing compliance.

Potential savings: $2 million+ in state taxes for trust route, indefinite federal deferral via ESOP can save $3 million+ over time on large transactions.

Best for: Sophisticated owners with significant gains ($20 million+) and long planning horizons, or C-corp owners with 30+ employees for ESOP.

Watch out for: Trust strategies face California scrutiny and need ironclad documentation of nonresident status and trust administration outside California. ESOP needs professional valuation, DOL compliance, and ongoing fiduciary responsibilities.

Both need expert legal and tax counsel.

Mistakes trigger full taxation plus penalties.

Making Your Decision

Relocating to a no-tax state paired with an installment sale offers the most accessible combination of substantial savings and manageable complexity for most business owners. This approach eliminates California’s 13.3% state tax entirely when done correctly, while spreading federal taxes across multiple years keeps you in lower brackets.

A business owner with a $10 million sale and $6 million basis saves about $520,000 in state taxes through relocation alone, plus another $200,000-$400,000 by avoiding federal bracket creep through installment payments.

The beauty of this combination comes from its relative simplicity compared to trusts or ESOP structures. You can document your relocation with clear evidence like lease agreements, utility bills, and time-tracking apps.

The installment sale needs buyer agreement but no complex entities or irrevocable commitments.

One Florida-relocated seller we reviewed spread a $15 million payment over seven years and netted 35% more after-tax compared to selling as a California resident with a lump sum payment.

Start your planning now if you’re considering a 2027 or later exit. Meet with a tax attorney who practices in both California and your target state.

Build your residency file with daily location records, sell California property, and cut professional and social ties.

Model your installment scenarios with your CPA to find the optimal payment structure.

For owners with very large gains ($20 million+) and longer timelines, combining relocation with nongrantor trust planning or QSBS strategies can push savings past $4 million. These complex routes make sense when the extra legal costs of $100,000-$200,000 are dwarfed by the tax savings.

Match your strategy to your timeline, business structure, and proceeds. Every situation differs, but doing nothing costs far more than any professional fees you’ll pay for proper planning.

Read our other more in depth articles for selling your business in California below:

- Top 5 Key Considerations When Selling a Business in California (2026)

- How to Sell a Business in California (2026)- Taxes, Timing & Exit Strategy – Pt1

- California Business Exit Strategy (2026)- How to Maximize Value and Reduce Taxes – Pt2

- 2026 California Business Sale Guide- Exit Strategy, Taxes & Timing – Pt3

Business Seller Checklist

Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If you are further along in the process, read our 3-part article for successful business exit planning when selling your California business here.

Frequently Asked Questions

How long do I need to live in a no-tax state before selling my business to avoid California taxes?

California courts look for genuine domicile change, not arbitrary time periods. Plan for at least 2-3 years of clear residency with supporting documentation.

Spend more than 183 days per year in your new state, obtain a driver’s license and voter registration there, close California bank accounts, sell California property, and maintain detailed calendars.

The Franchise Tax Board pursues these cases aggressively, so err on the side of over-documentation. Some practitioners recommend capturing three full calendar years in the new state if your gain exceeds $5 million.

Will California tax me on my business sale if I’m a nonresident?

California can tax business income “sourced” to the state even for nonresidents. However, if you sell corporate stock or partnership interests after establishing nonresident status, recent cases suggest California cannot tax the gain. Real estate located in California stays taxable.

Services performed in California are taxable.

The key distinction is between selling business assets (potentially taxable) versus selling ownership interests after you’ve established clear nonresident status (generally not taxable). This area is complex and fact-specific, requiring professional analysis of your business structure.

Can I use the QSBS exclusion if I convert my S-corp to a C-corp now?

Converting triggers a new five-year holding period starting from the conversion date. Your existing basis carries over, but any appreciation after conversion gets built-in gains tax treatment.

If your S-corp has significant existing appreciation, conversion may trigger taxes that offset QSBS benefits.

Run detailed projections with your tax advisor comparing the built-in gains tax hit against potential QSBS savings. Companies planning exits 6+ years out have better conversion economics than those looking to sell within three years.

What happens if the buyer defaults on an installment sale?

You’ve already paid tax on the gain portions received, but you may not collect future payments. Structure protection into the deal with security interests in business assets, personal guarantees, or life insurance on the buyer.

If you foreclose and take back the business or assets, complex tax rules govern how you report the transaction.

Consider requiring larger down payments (30-40%) for riskier buyers. Title insurance products exist for some transaction types.

Your transaction attorney should document the security thoroughly in the promissory note and security agreement.

Are charitable remainder trusts worth the complexity for business sales under $5 million?

CRTs make economic sense when charitable intent aligns with tax savings. For a $5 million gain, you might save $1 million in federal taxes and receive a $500,000+ charitable deduction, but setup costs run $15,000-$30,000 and annual administration adds $3,000-$5,000.

If you planned to leave money to charity anyway and want lifetime income, the economics work even on smaller transactions.

Without genuine charitable intent, other strategies deliver better after-tax results. The irreversible nature means you need high confidence in your decision.

How many employees do I need to establish an ESOP?

No legal least exists, but practical considerations suggest 30+ employees for cost-effectiveness. ESOP setup costs $80,000-$150,000, with annual administration of $20,000-$40,000 for valuations, Form 5500 filings, and compliance.

These costs per participant drop as headcount rises.

Companies with fewer than 20 employees rarely find ESOPs economical unless the business value exceeds $15 million. The Department of Labor scrutinizes small ESOPs heavily to confirm the transaction serves employees, not just the selling owner.

Can I combine multiple strategies like relocation plus QSBS plus installment sales?

Strategies stack effectively when structured properly. Relocate to eliminate state taxes, use QSBS to eliminate federal taxes (up to limits), and structure remaining gain as an installment sale to spread any non-QSBS-eligible portions.

A $25 million gain might break down as: $10 million QSBS-excluded (federal), $15 million via installment over 10 years, all while a Nevada resident (no state tax).

This creates most deferral and elimination across federal and state systems. Complex combinations need sophisticated tax counsel to avoid conflicts between provisions, but the savings on very large transactions justify the professional costs.

References:

[1] Nongrantor trust strategies and California sourcing rules

[2] Charitable Remainder Trust and ESOP tax treatment

[5] Installment sales and QSBS provisions under IRC

[6] California residency audit practices and wealth migration patterns

[9] Entity restructuring timelines and planning requirements

[13] Section 1202 QSBS qualification rules

[15] ESOP establishment and deferral mechanics

References

[1] Nongrantor trust strategies and California sourcing rules

[2] Charitable Remainder Trust and ESOP tax treatment

[5] Installment sales and QSBS provisions under IRC

[6] California residency audit practices and wealth migration patterns

[9] Entity restructuring timelines and planning requirements

[13] Section 1202 QSBS qualification rules

[15] ESOP establishment and deferral mechanics

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.