Quick Summary

Selling a business in California involves far more than simply finding a buyer. Owners who begin preparing 2–5 years in advance typically achieve higher valuations, smoother negotiations, and better after-tax outcomes.

Key considerations include organizing clean financial records, reducing owner dependence, protecting confidentiality during the sale process, understanding California’s significant tax implications, and choosing the right deal structure (asset sale vs. stock sale).

Buyers place a premium on businesses with documented systems, stable management teams, recurring revenue, and transferable operations. Working with experienced advisors—such as business brokers, tax strategists, and M&A attorneys—can help maximize sale value while avoiding costly mistakes during due diligence and negotiations.

Ultimately, successful exits are built through preparation, strategic planning, and timing rather than rushed decisions.

Introduction

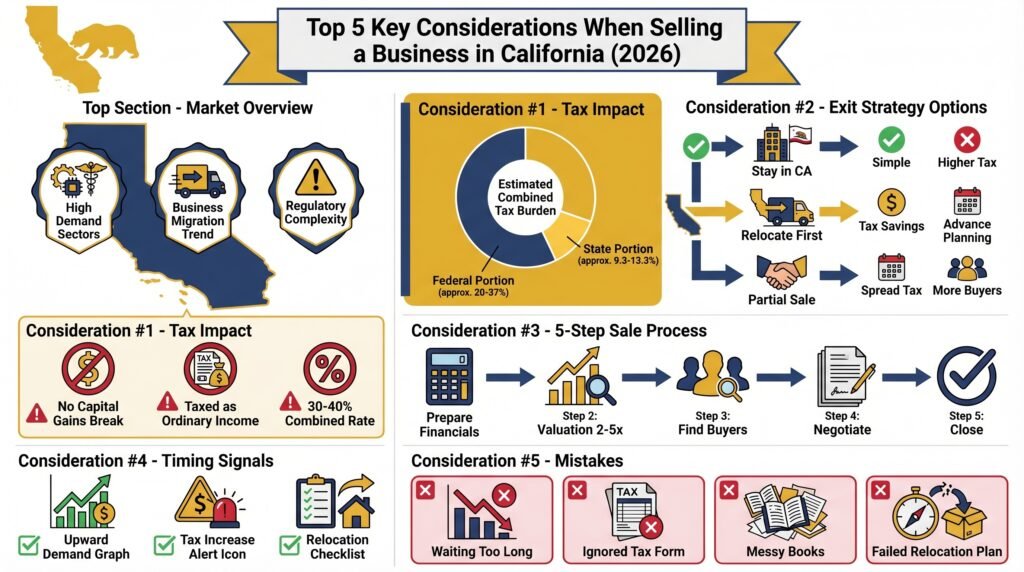

Selling a business in California presents unique challenges that go beyond the typical deal negotiations and paperwork. In 2026, owners face a brutal tax environment with state capital gains rates reaching 13.3%, aggressive Franchise Tax Board audits, and proposed exit taxes targeting high-net-worth people leaving the state.

Add in property reassessment rules, sales tax compliance hurdles, and the ongoing exodus of businesses to states like Texas, Florida, and Nevada, and you’ve got a complex landscape to navigate.

The surge in business migration out of California has created a new playbook for smart exits. Many owners are now timing their business exit strategy around relocation, selling your business before moving to avoid the state’s heavy tax burden.

Whether you’re looking to sell a small business or exit a larger operation, understanding how to sell a business while minimizing your California tax exposure can save you hundreds of thousands or even millions of dollars.

This guide breaks down the five most critical considerations to help you exit business high tax state situations cleanly and keep more of your hard-earned sale proceeds.

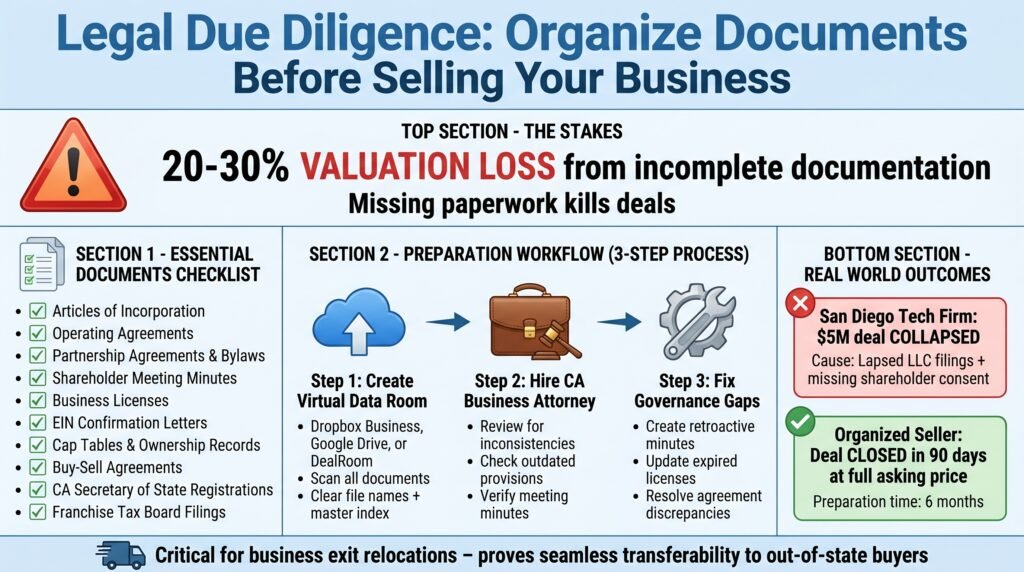

1. Organize Legal Documents and Conduct Early Due Diligence

Getting your legal house in order early is the foundation of any successful business sale. Buyers will scrutinize every document during due diligence, and missing or inconsistent paperwork can kill deals faster than almost anything else.

Industry experts report that incomplete documentation can slash your business valuation by 20-30% or cause buyers to walk away entirely.

Start by gathering your articles of incorporation, operating agreements, partnership agreements, bylaws, shareholder meeting minutes, business licenses, EIN confirmation letters, and detailed ownership records including cap tables.

If you have many owners, make sure buy-sell agreements are current and properly executed. For California-specific requirements, verify that all state registrations with the Secretary of State and Franchise Tax Board are up to date and in good standing.

How to prepare your documents:

Create a virtual data room using platforms like Dropbox Business, Google Drive, or specialized services like DealRoom. Scan and organize every document with clear file names and a master index.

Hire a business attorney experienced in California transactions to review everything for inconsistencies, outdated provisions, or missing items.

This is especially important for meeting minutes, which California courts take seriously even though many small businesses skip them.

Address any governance gaps immediately. If you haven’t held annual meetings or documented major decisions, create retroactive minutes with your attorney’s guidance.

Update any expired licenses or permits, and decide discrepancies between your operating agreement and actual business practices.

A San Diego technology firm owner learned this lesson the hard way when a $5 million acquisition fell apart after buyers discovered lapsed LLC filings and missing shareholder consent for a major contract. Another seller who spent six months organizing documents in advance closed their deal in just 90 days at full asking price.

This preparation becomes even more critical if you’re planning business exit strategy relocation. Clean documentation shows to out-of-state buyers that the business can transfer seamlessly, regardless of where you’re headed next.

When you’re selling your business before moving, buyers need confidence that everything is legitimate and transferable.

California Secretary of State Business Search

2. Clean Up Financials and Address Tax Compliance Head-On

Nothing scares away serious buyers like messy books or unresolved tax issues. California’s Franchise Tax Board has a reputation for aggressive enforcement, and any red flags in your financial records will become major negotiating points or deal-breakers.

You need at least three years of clean profit and loss statements, balance sheets, cash flow reports, and finish payroll tax records.

Your financial statements should be prepared using Generally Accepted Accounting Principles (GAAP) or at least reviewed by a qualified CPA. Ideally, get compiled or audited statements, which carry more credibility with buyers and their lenders.

Make sure depreciation schedules are accurate and up to date, and that you can clearly explain any unusual expenses or income fluctuations.

California-specific tax traps to address:

The state doesn’t conform to federal Qualified Small Business Stock (QSBS) exclusions, so you’ll owe California capital gains even if you qualify federally.

Consider electing the Pass-Through Entity Tax (PTET) if you operate as an S-corp or LLC, which let’s you remove state taxes on your federal return.

Work with your CPA to allocate part of the sale price to personal goodwill rather than business assets, as personal goodwill gets more favorable capital gains treatment when you’re the key relationship driver.

File your final tax returns marked “Final” with the FTB, and formally close any sales tax accounts through the California Department of Tax and Fee Administration (CDTFA). Sales tax allows don’t transfer to buyers, so handle this properly.

Disclose and decide any outstanding tax liabilities, payroll tax arrears, or pandemic-era loans like EIDL that might still be on your books.

Getting compliant step by step:

Engage a CPA who specializes in California business transactions for a finish financial review. Have them reconcile all sales and use taxes, and register properly with CDTFA if you’re selling inventory as part of the deal.

Model out your tax hit in advance.

A $10 million capital gain costs $1.33 million in California state taxes alone at the 13.3% top rate, before you even factor in federal taxes.

One Los Angeles restaurant owner structured an asset sale carefully, used the PTET election to save $200,000 federally, and successfully relocated to Arizona immediately after closing. Poor financial preparation often leads to nasty post-sale surprises from the FTB, potentially destroying your plans to sell a small business and move on cleanly.

CDTFA Sellers Permit Information

3. Review and Fix Contracts, Liabilities, and IP Assets

Your contracts form the operational backbone that buyers are actually purchasing. They’ll examine every agreement for assignment restrictions, unusual terms, or personal guarantees that could prevent transfer.

Customer contracts, vendor agreements, leases, loan documents, and employee arrangements all need thorough review months before listing your business.

Look specifically for “change of control” provisions that could end key relationships upon sale. Many commercial contracts include non-assignment clauses requiring third-party consent before transfer.

Start negotiating these consents early, since vendors or landlords might use your sale as leverage for better terms.

Leases deserve special attention. Short remaining lease terms or unfavorable renewal options can significantly impact valuation, especially for retail or restaurant businesses where location drives revenue.

Resolve outstanding liabilities before they become buyer concerns. Settle or disclose any pending lawsuits, regulatory investigations, vendor disputes, or customer complaints.

In California, employment-related claims pose particular risks.

Make sure you’re fully compliant with state wage and hour laws, meal and rest break requirements, and independent contractor classification rules under AB5.

Intellectual property needs proactive protection:

Register your trademarks with the USPTO if you haven’t already. Secure relevant domain names and social media handles under company ownership.

Review and update all employee and contractor agreements to include proper IP assignment provisions.

California law presumes employees own work they create outside business hours unless you have written agreements stating otherwise. Have your attorney audit IP assignments for any gaps.

Update non-disclosure agreements and employee handbooks to reflect current California employment law. Make sure non-compete agreements follow California’s strict limitations, which generally void them except in narrow circumstances like business sales.

A Bay Area SaaS company spent three months fixing expiring vendor contracts and resolving employment classification issues before going to market. The cleanup increased their final sale price by 15%.

Another seller ignored these issues and faced a lawsuit six months after closing, eating up sale proceeds in legal fees.

Proper contract and liability management supports your strategy to exit business high tax state operations by making the business “plug and play” for out-of-state buyers. When buyers see clean, transferable relationships, they’re willing to pay premium valuations.

For those looking to avoid taxes when selling a business, structure matters tremendously. Asset sales versus stock sales create completely different tax consequences.

Buyers typically prefer asset purchases because they get a stepped-up tax basis, while sellers usually prefer stock sales for better capital gains treatment.

Navigate this negotiation with professional guidance.

4. Structure the Deal for Tax Minimization and Relocation Timing

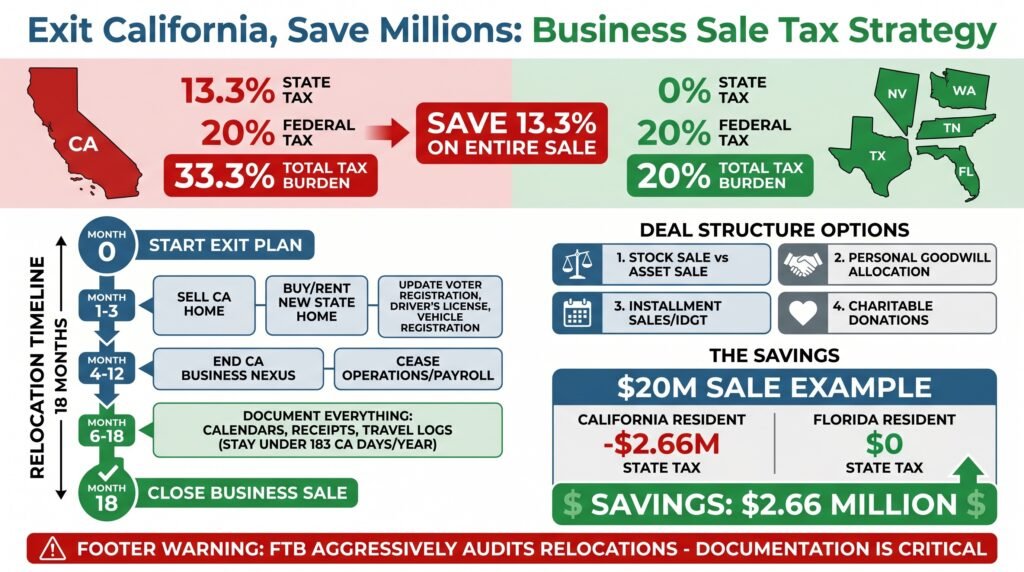

California’s tax environment makes deal structure and timing absolutely critical. At 13.3%, California levies one of the highest state capital gains rates in the country on top of federal rates that can hit 20%.

The state doesn’t conform to federal QSBS exclusions that benefit some startup founders.

Worse, proposed legislation similar to AB 2088 continues surfacing with 10-year lookback provisions targeting wealthy people who leave California and later sell assets.

Your business exit strategy should center on residency status when the sale closes. California taxes residents on all income regardless of source, but non-residents only owe California tax on California-sourced income.

If you can establish residency in a no-income-tax state like Texas, Florida, Nevada, Tennessee, or Washington before closing your sale, you potentially avoid the entire 13.3% California capital gains hit.

Tax minimization strategies to talk about with professionals:

Consider whether an asset sale or stock sale makes more sense for your situation. Stock sales generally provide better tax treatment for sellers since all proceeds receive long-term capital gains rates.

Asset sales create a mix of ordinary income (for inventory, receivables) and capital gains, but buyers love them for the depreciation benefits.

Allocate part of the purchase price to personal goodwill if you’re the key relationship driver. Personal goodwill gets favorable capital gains treatment because it’s your personal asset, not the company’s.

This works when clients buy from the business specifically because of you.

Explore installment sales that spread income over many years, reducing the single-year tax spike. Consider selling to an Intentionally Defective Grantor Trust (IDGT) to defer gains.

Make charitable donations of business interests before the sale to exclude donated portions from taxable income.

Relocation timing for those selling your business before moving:

Move 12-18 months before closing if possible. California aggressively audits former residents claiming they left, so you need overwhelming evidence.

Sell your California home, rent or buy in your new state, update voter registration and driver’s license, forward mail permanently, and register vehicles in the new state.

End all California business nexus by ceasing operations, payroll, and California-focused activities.

Document time spent in each state meticulously. Spend fewer than 183 days per year in California after establishing new residency.

Keep detailed calendars, receipts, and travel records.

California’s Franchise Tax Board has the burden of proof, but only if you can show you truly left.

Compare state tax impacts carefully. Florida residents pay zero state income tax on a $20 million business sale, saving $2.66 million compared to California residents.

That’s real money worth planning around.

One founder I know moved to Texas 18 months before closing his startup sale, saved $2.6 million in state taxes, and documented everything perfectly to survive an FTB audit.

The risk of rushed exits is real. The FTB commonly challenges “overnight” relocations, claiming you maintained California ties through property ownership, business operations, or family relationships.

With many states now proposing exit taxes on accumulated wealth, act sooner rather than later.

FTB Residency Status Guidelines

5. Decide on Asset vs. Entity Sale and Handle Post-Sale Filings

The fundamental choice between selling assets versus selling your entity (stock or membership interests) shapes everything from tax liability to ongoing obligations. Get this decision right early because it affects deal structure, negotiations, and closing processes.

Asset sales let buyers cherry-pick what they want such as inventory, equipment, intellectual property, customer lists, and contracts while leaving behind liabilities, lawsuits, and unknown risks. Buyers love asset purchases because they get a stepped-up tax basis for depreciation.

Sellers typically dislike them because proceeds get split between ordinary income (inventory, receivables) and capital gains (goodwill, IP), potentially creating higher tax bills.

Entity sales transfer the entire company structure, stock certificates or LLC membership interests. The buyer assumes everything including unknown liabilities, which makes them nervous.

Sellers prefer entity sales because all proceeds typically qualify for long-term capital gains treatment, creating lower taxes.

Speed is another advantage since you’re not transferring dozens of individual assets.

California-specific considerations:

Entity sales trigger change-of-ownership property reassessment under Revenue and Taxation Code Section 64 when more than 50% of ownership interests transfer. If your business owns real property in California, reassessment at current market value can create substantial property tax increases for the buyer, making entity sales less attractive.

Asset sales need careful sales tax handling. You’ll need to register the asset transfer with CDTFA and potentially collect sales tax on inventory and equipment.

Entity sales generally avoid sales tax but need proper notification to many state agencies.

Pros and cons summary:

Critical closing and post-closing steps:

Draft a comprehensive purchase agreement listing all assets, purchase price allocation, payment terms, representations and warranties, and non-compete provisions. Have both your attorney and CPA review for accuracy before signing.

After closing, tell CDTFA of the business transfer or closure. File final tax returns with the FTB using Form 100 (corporations) or Form 568 (partnerships/LLCs) clearly marked “Final Return.”

Submit required change-of-ownership statements to the county assessor if real property transferred. Formally dissolve or surrender your business entity with the California Secretary of State once all tax clearances are obtained.

A Fresno manufacturing company executed a clean asset sale, avoided inheriting entity liabilities, and closed successfully within 90 days. The structure let the owner relocate immediately to Nevada without ongoing California filing obligations.

This properly concludes your how to sell a business process and frees you to enjoy life in a lower-tax state.

SBA Guide to Selling Your Business

Business Seller Checklist

Whether you are planning to sell your business solo or utilize the experience and leveraging skills of a broker, pause and review the discussed points, and you have done the basic preparation needed to place your business on the market.

A major contributor to business undervaluations, wasted time, and poor exits is simply a lack of readiness. A broker can only sell what you’ve built.

If your business:

- Depends heavily on you

- Has inconsistent or unclear financials

- Lacks systems or transferable processes

Then even the best broker will struggle to get a premium offer. Brokers don’t create value. They expose it.

Bottom line: If you are not sure what basic preparation is required before considering a business valuation or selecting a business broker, click the link below to take our free business readiness quiz. The score will give you a clear indication of where you are in the process and the next course of action to take to ensure you start the business sale and exit on the right footing.

If you are further along in the process, read our 3-part article for successful business exit planning when selling your California business here.

Conclusion

After reviewing all five considerations, organizing legal documents and conducting early due diligence (Consideration #1) stands out as the most critical starting point. This single step prevents roughly 80% of deal-killers, buys you time for sophisticated tax planning, and signals professionalism to serious buyers.

Clean documentation becomes even more valuable when selling your business in California during the current wave of business migration to low-tax states.

One business owner I encountered turned finish operational chaos into a $15 million exit simply by starting the organization process 18 months before listing. The early preparation let him identify and fix problems that would have torpedoed negotiations, and gave his tax team time to structure an optimal deal that saved over $400,000 in unnecessary taxes.

If you’re ready to sell a small business or develop your business exit strategy relocation, start by consulting with a California business attorney and a CPA who specializes in business transactions. Don’t wait until you’ve found a buyer to begin organizing documents and addressing compliance issues.

The earlier you start, the more options you’ll have for structuring a tax-efficient exit.

For the smartest approach to exit business high tax state situations, prioritize working with advisors experienced in California-to-low-tax-state transitions. Begin with thorough FTB-compliant financial preparation and aim to establish residency in your target state well before closing.

The goal is completing your sale as a non-resident of California to avoid taxes when selling a business that could otherwise consume 13.3% of your gains.

With proper planning and execution, you keep dramatically more of what you’ve built.

Your decades of hard work and risk-taking deserve most protection. Every dollar you save on unnecessary taxes is a dollar you can invest, enjoy in retirement, or use to fund your next venture.

Take action now to position yourself for the best possible outcome when selling your business before moving out of California’s high-tax environment.

Frequently Asked Questions

What is California’s proposed exit tax and does it apply in 2026?

California has not enacted an exit tax as of 2026, but proposed legislation like AB 2088 from prior years targeted high-net-worth people leaving the state with potential 10-year lookback provisions on wealth accumulated while a California resident. While no exit tax is now law, the Franchise Tax Board aggressively audits former residents who claim they left California before realizing large gains.

The FTB looks for ongoing ties like California business operations, maintained property, or significant time spent in state.

To protect yourself, sever all California connections 12-18 months before your business sale and document everything meticulously.

How do I become a non-resident before selling to avoid California taxes?

Establishing non-residency needs moving your domicile completely. Sell your California home or convert it to a rental, purchase or rent a home in your new state, update your driver’s license and vehicle registration, change voter registration, forward mail permanently, and close California bank accounts.

Most importantly, spend fewer than 183 days per year in California after your move.

End all California business operations, payroll, and customer concentration. Your capital gains get sourced to your residency status on the sale date, so finish your move well before closing.

Many Reddit users in tax forums report needing at least two years of documented evidence to successfully defend their non-resident status during FTB audits.

Asset sale or stock sale, which minimizes taxes for California sellers?

Stock or entity sales typically provide better tax treatment for sellers because all proceeds qualify for long-term capital gains rates up to 13.3% California plus 20% federal. Asset sales create a mixture of ordinary income taxed up to 37% federally on items like inventory and receivables, plus capital gains on goodwill and intellectual property.

However, using the Pass-Through Entity Tax (PTET) election for S-corps and partnerships can help by making state taxes federally deductible.

California doesn’t conform to federal QSBS exclusions, so startup founders get no state tax break even if they qualify federally. Always model both scenarios with your CPA before negotiating.

How long does selling a small business in California typically take?

Well-prepared businesses usually sell within 6-12 months from listing to closing. Businesses with messy financials, compliance issues, or unclear documentation often take 18 months or longer.

Due diligence alone can consume 60-90 days for complex businesses.

Family transitions or sales to existing employees tend to move fastest, sometimes closing in 3 months, while third-party sales to unknown buyers take longest because of extensive due diligence and financing requirements. Starting your preparation 18-24 months before you want to close gives you time to clean up issues without pressure.

What about property tax reassessment when selling my business?

California Revenue and Taxation Code Section 64 triggers property reassessment when more than 50% of a business entity’s ownership interests change hands. If your business owns real estate, reassessment at current market values can dramatically increase property taxes for the buyer.

This makes entity sales less attractive for businesses holding appreciated property.

Asset sales often avoid reassessment if the real estate stays with the original entity or transfers separately. Some sellers handle this by separating real estate into a different entity before the sale and leasing it to the business long-term.

Consult with a tax professional about your specific situation.

Can I use trusts or installment sales to defer capital gains taxes?

Yes, several strategies can spread or defer your tax hit. Installment sales let you receive payments over many years, recognizing gain as you receive cash rather than all upfront.

This keeps you out of the highest tax brackets and may span years when you’re a California resident and a non-resident.

Intentionally Defective Grantor Trusts (IDGTs) involve selling your business to a trust before the actual sale, potentially deferring gains significantly. Charitable donations of business interests before selling exclude the donated portion from taxable income.

California generally follows federal tax treatment for these strategies, but timing and structure matter enormously.

Work with an estate planning attorney and CPA experienced in California business exits to apply these properly.

Do I need a business broker when selling my business?

Hiring a broker isn’t legally required, but professional intermediaries handle approximately 70% of small to mid-sized business sales and often net sellers 10-20% higher prices through their networks and negotiation experience. Brokers charge commissions typically ranging from 5-10% of the sale price, sometimes on a sliding scale for larger deals.

For businesses valued under $500,000, you might successfully handle the sale yourself using marketplaces like BizBuySell.

For anything larger or more complex, broker expertise in valuation, marketing, buyer qualification, and deal structuring usually pays for itself. Make sure any broker you hire has specific experience with California business transactions and understands the tax implications of different deal structures.

References:

[1] California Secretary of State Business Search: https://bizfileonline.sos.ca.gov/search/business

[2] California Department of Tax and Fee Administration: https://www.cdtfa.ca.gov/services/sellers-permit.htm

[3] United States Patent and Trademark Office: https://www.uspto.gov/trademarks/search

[4] California Franchise Tax Board Residency Guidelines: https://www.ftb.ca.gov/file/personal/residency-status/index.html

[5] U.S. Small Business Administration: https://www.sba.gov/business-guide/manage-your-business/close-or-sell-your-business

[6] JMiller Law Group: Selling a Business in California

[7] BrightTax: California Exit Tax Guide

[8] Grimbleby-Coleman CPAs: Tax Implications for Business Sales

[9] BNY Wealth: Reducing Tax Impact on Business Sales

[10] JD Supra: Capital Gains Strategies for Business Owners

References

[1] Nongrantor trust strategies and California sourcing rules

[2] Charitable Remainder Trust and ESOP tax treatment

[5] Installment sales and QSBS provisions under IRC

[6] California residency audit practices and wealth migration patterns

[9] Entity restructuring timelines and planning requirements

[13] Section 1202 QSBS qualification rules

[15] ESOP establishment and deferral mechanics

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice.

*Disclaimer: This article is written for educational purposes and should not be interpreted as financial advice. We may receive compensation for referrals made through this article.